LIC Housing Finance Q4 Surprise: Profit Climbs, But Loan Growth Still Drags The Story

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

LIC Housing Finance posted a stronger Q4 FY26 profit, but slow loan-book growth kept the result from becoming a full recovery story.

Key Takeaways

- LIC Housing Finance’s Q4 FY26 PAT rose 9% to ₹1,497.41 crore, helped by lower provisions, better margins and higher disbursements.

- The previous update was management’s FY26 expectation of double-digit growth, but the outstanding loan portfolio grew only 4%.

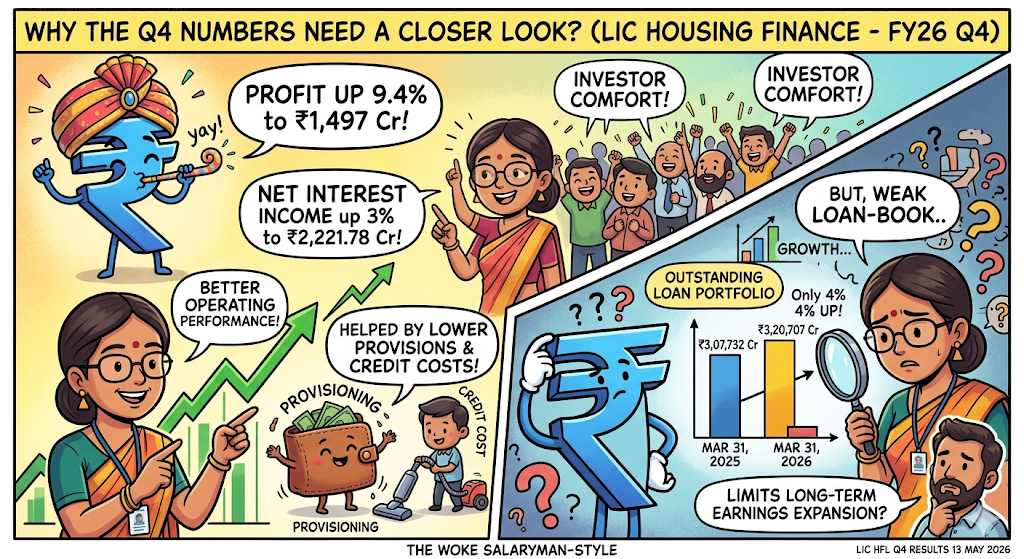

Why The Q4 Numbers Need A Closer Look?

LIC Housing Finance announced its standalone audited Q4 FY26 results on May 13, 2026, after its board meeting in Mumbai. Profit after tax rose to ₹1,497.41 crore from ₹1,367.96 crore a year ago, while net interest income rose 3% to ₹2,221.78 crore.

In the short term, the result gives investors comfort on profitability and asset quality. In the long term, the weak loan-book growth can limit earnings expansion. The company’s outstanding loan portfolio was ₹3,20,707 crore as of March 31, 2026, up only 4% from ₹3,07,732 crore a year earlier.

The company’s revenue from operations slipped 1%, but profit improved due to better operating performance and lower credit cost. Economic Times reported on May 14, 2026 that LIC Housing Finance’s Q4 net profit rose 9.4% to ₹1,497 crore, helped by lower provisions even as earnings dipped.

The dividend proposal of ₹10 per share gave shareholders a direct payout, but Business Standard reported on May 14, 2026 that the stock still fell after the result, showing investor concern over growth quality.

Loan Growth Weakness Could Hit Borrowers And Housing Demand

For homebuyers, the positive part is that LIC Housing Finance disbursed more loans in Q4. Total disbursements rose 10% to ₹21,019 crore from ₹19,156 crore. Individual home loan disbursements rose 8% to ₹16,672 crore, while non-housing individual loans jumped 25% to ₹3,348 crore.

Borrowers tracking affordability can use the LoansJagat LIC Home Loan EMI Calculator, which helps calculate monthly EMI, total interest payable and total loan cost. The tool page was crawled on May 13, 2026 and published 2 months ago.

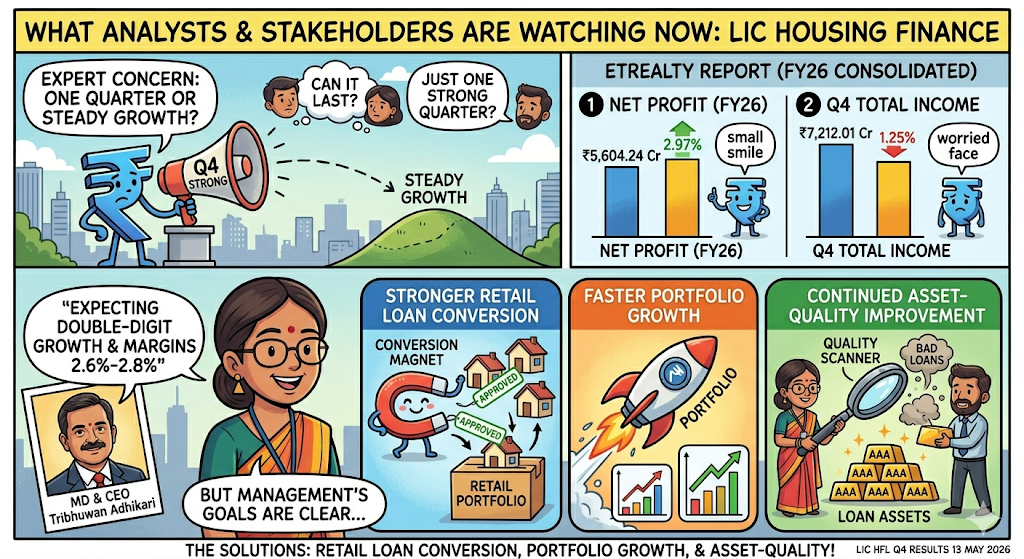

What Analysts And Stakeholders Are Watching Now?

The biggest expert concern is whether one strong quarter can become steady growth. ETRealty reported on May 13, 2026 that LIC Housing Finance’s FY26 consolidated net profit rose 2.97% to ₹5,604.24 crore, while Q4 consolidated total income declined 1.25% to ₹7,212.01 crore. (ETRealty.com)

Earlier, MD and CEO Tribhuwan Adhikari told ETMarkets on October 31, 2025 that the company expected double-digit growth ahead, with margins stabilising around 2.6% to 2.8%. The solution now is stronger retail loan conversion, faster portfolio growth and continued asset-quality improvement.

Conclusion

LIC Housing Finance delivered a profitable Q4 with stronger disbursements and better asset quality. But unless loan growth rises above 4%, the recovery story will remain incomplete.

FAQs

Should Someone Choose LIC Housing Finance For A Home Loan Over Banks?

LIC Housing Finance can work for a borrower if the interest rate is lower and all loan terms are checked properly. In the Reddit post, the person mentioned a ₹35 lakh loan offer at 7.10% for 5 years. Many replies asked the borrower to compare it with banks before deciding.

One reason is that housing finance companies may not reduce rates as fast as banks when repo rates fall. Before choosing LIC HFL, check processing fee, prepayment rules, foreclosure charges, rate reset terms and branch support. A lower rate helps, but only if the loan stays flexible.

How Much Interest Does LIC Housing Finance Charge On A Home Loan?

LIC Housing Finance gives home loans at different interest rates based on the borrower’s CIBIL score, loan amount, income and repayment profile. As per recent reports, LIC HFL cut its starting home loan rate to 7.15% for borrowers having a CIBIL score of 825 or above and loans up to ₹5 crore.

Many borrowers may still get a higher rate if their credit score is lower or if the loan risk is higher. So, before applying, one should compare LIC HFL rates with banks, check processing charges and calculate EMI through the LoansJagat LIC Home Loan EMI Calculator.

Related Finance News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article