By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key takeaways

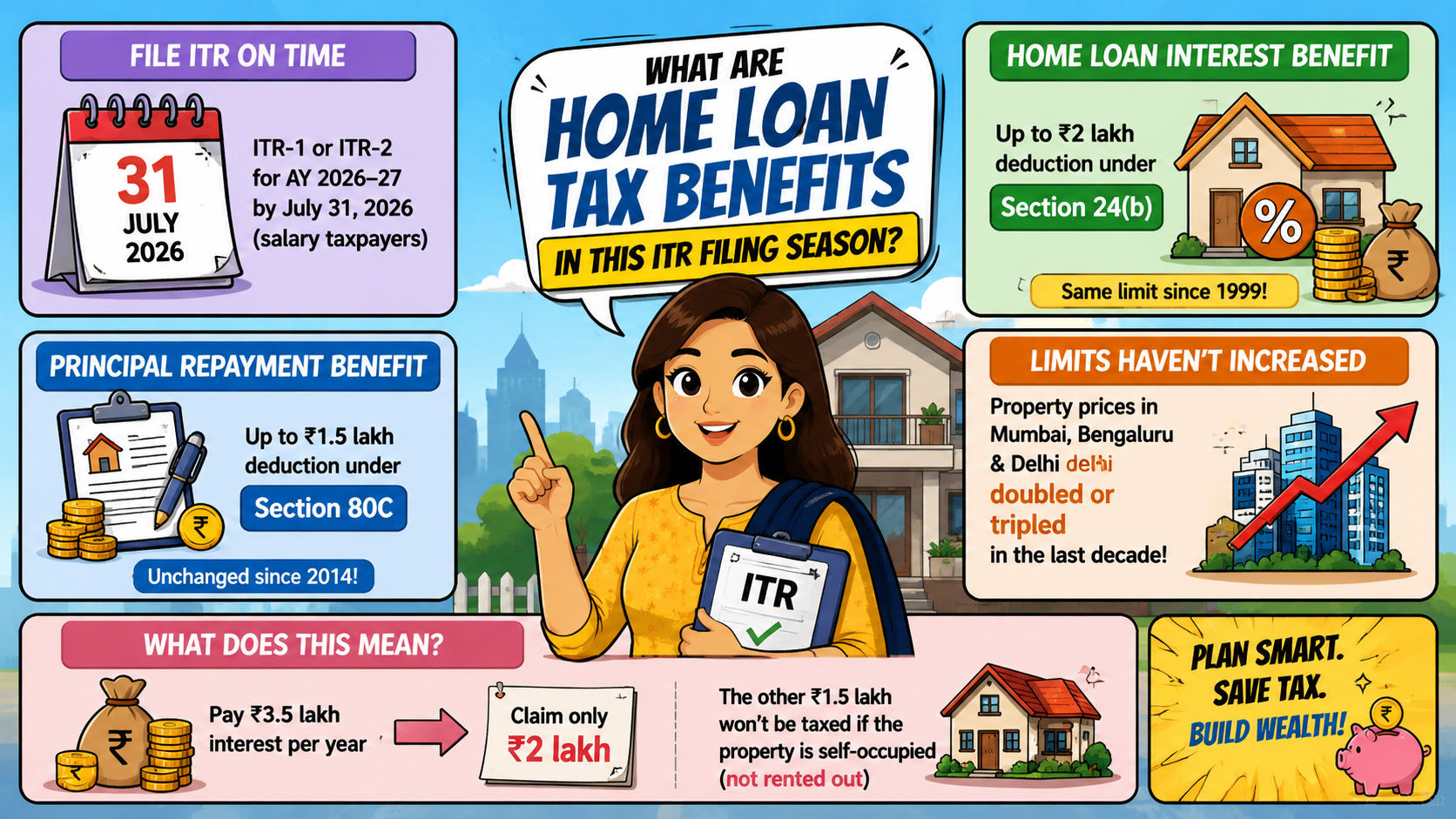

CBDT released all ITR forms for AY 2026-27 on March 30, 2026. Individuals whose tax is deducted through salary need to file ITR-1 or ITR-2 by July 31, 2026. As per Section 24(b), the home loan interest tax benefit of ₹2 lakh has remained the same since it was introduced by the Income Tax Act in 1999. Section 80C provides another benefit of ₹1.5 lakh on home loan principal repayment, unchanged from 2014.

This implies that the limit has not increased with EMI costs for most individuals. As per analysis of Canara HSBC Life in its Budget 2026 report, the prices of properties in Mumbai, Bengaluru and Delhi have doubled or even tripled in the last decade. An individual who pays ₹3.5 lakh per year on interest can claim only a deduction of ₹2 lakh. The other ₹1.5 lakh will not be taxed in case the property is not rented out.

This question is academic now for 72% of taxpayers who switched to the new tax regime in AY 2024-25, as per data by Bajaj Finserv.

The new regime blocks Section 24(b) entirely for self-occupied homes. Only interest on rented properties can be set off, and only against actual rental income, not salary.

Out of 1 lakh housing-related queries on LoansJagat.com, borrowers repeatedly ask why their EMI outgo does not match their tax savings. Housing loans account for 52% of total household debt in India, per the RBI’s Household Finance Committee Report dated September 26, 2017. That share explains why any freeze in deduction limits directly hits a large section of middle-class households, especially first-time buyers in metro cities.

According to The Economic Times of December 6, 2024, tax advisors have recommended comparing the two regimes annually prior to making returns. According to the April 2026 report of Bajaj Finserv, “It is advisable for borrowers to switch to the old regime only when their deductions, including 80C, 24(b), and 80D, exceed ₹4.5 lakh.” Below that threshold, the new regime's ₹75,000 standard deduction often works out better.

The solution experts recommend is simple. Salaried non-business taxpayers can switch regimes directly in the ITR every year before the July 31, 2026 deadline. The Income Tax Department’s e-filing portal offers a built-in regime comparison tool. Homebuyers with loans above ₹40 lakh should run both calculations before submitting Form 16 data.

The ₹2 lakh home loan interest cap under Section 24(b) has not moved since 1999, even as EMIs and property prices climbed sharply across Indian cities. Given the July 31, 2026 ITR filing deadline, the taxpayer should make a comparison of regimes rather than presume that their old-regime deductions will continue to yield the same benefit that they used to yield.

FAQs

No. As per Budget 2026, there is no increase in the interest deduction of Section 24(b) for AY 2026-27 under the old regime.

Log in to incometax.gov.in and check your intimation under Section 143(1). If the ₹2 lakh interest was missed, submit a rectification request within the return's assessment year, attaching your lender's interest certificate as proof.

Read Also