By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

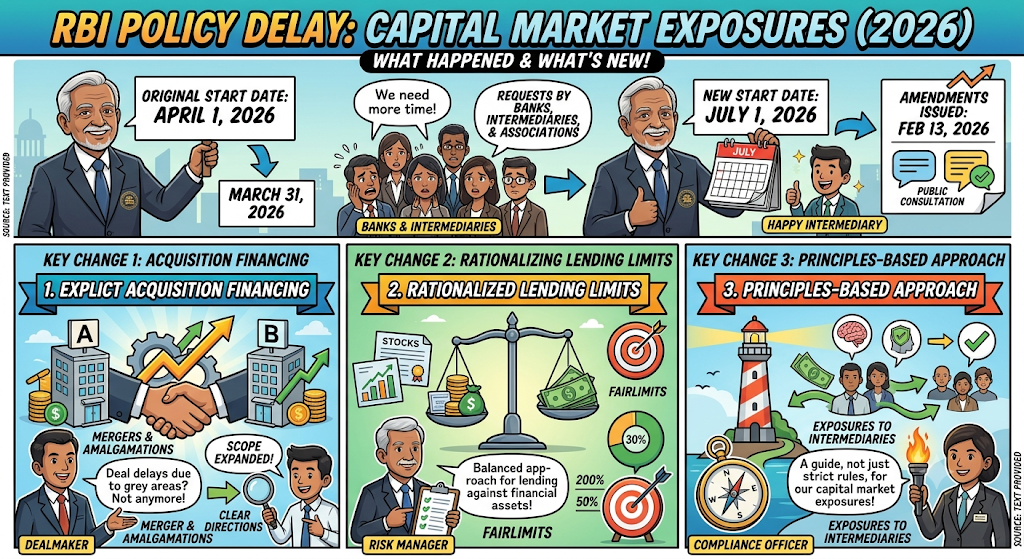

The RBI pushed back the start date of its new capital market exposure policy from April 1 to July 1, 2026 in March 31, 2026. The RBI explained that the decision was made because of the requests made by the banks, capital market intermediaries, and other industry associations. The amendment directions were originally issued on February 13, 2026, following a public consultation exercise.

The framework itself introduces 3 key changes, it facilitates acquisition financing more explicitly, rationalises lending limits against financial assets, and introduces a more principles-based approach for exposures to capital market intermediaries. The scope of acquisition finance has been expanded to now explicitly cover mergers and amalgamations, removing a grey area that had been causing deal delays.

The new rules expand access to bank-funded acquisition finance but impose clear restrictions for companies planning mergers. Such financing is only permitted when acquiring control of a non-financial company. Banks can refinance acquisition loans only after the transaction is completed and control is established. Where acquisition finance is extended through a subsidiary or SPV, a corporate guarantee from the acquiring company is now mandatory.

For Indian high-net-worth investors and firms using loans against shares, the new rules are also relevant. LoansJagat notes that as of Q1 2024, outstanding securities-backed loans globally are estimated at $138 billion, with Indian HNIs “closely monitoring this approach” as a way to access liquidity without selling shares. The RBI's revised framework, by rationalising lending limits against financial assets, aims to ensure these loans are structured with proper collateral and risk controls from July 1, 2026 onwards.

For capital market intermediaries like brokers, the RBI provided specific operational relief. Banks can now fund proprietary trading against 100% cash or cash-equivalent collateral. The RBI has also removed restrictions on financing market makers against the same securities used for market-making activities, a step that should improve market liquidity.

Whalesbook analysts noted the 3-month deferral fits a broader RBI trend of strengthening financial sector resilience, particularly after banking stocks faced pressure from the RBI's limits on net open forex positions on March 30, 2026. They added the RBI is ensuring “more involvement in capital markets and acquisition finance is backed by strong risk management and sufficient capital.”

Conclusion

The RBI's 3-month deferral to July 1, 2026, gives banks and intermediaries the runway they need to align systems without disrupting deal activity. The final framework arriving on July 1 will set clearer rules for India's M&A and capital markets lending for years, with acquisition finance now covering mergers and stricter refinancing conditions in place.

FAQs

So far as of July 2, 2026, no notification regarding the postponement of the exam from the side of RBI has come out yet. As per schedule, the RBI Grade B Mains exam for the General Stream would be conducted on July 25, 2026, while for DEPR & DSIM Streams would be held on July 26, 2026.

To qualify, the company's total bank and NBFC exposure must not exceed ₹25 crore. The account must be classified as a Standard Asset, not an NPA, and the business must hold a valid GST registration. Fraud-linked accounts are completely ineligible, and banks conduct a viability assessment before approving any restructuring request.

Epfo Services Resume Aadhaar Email Updates Turn Free Passport Fees Rise From July 1 2026

India Inflation Outlook Improves As Cpi Holds At 3 93 Following Drop In Commodity Prices

Fintech Small Ticket Personal Loan Defaults Rose To 6 4 Percent By March 2026 Rbi Fsr Warns

2 Us Judges Block Trumps Student Loan Forgiveness Limits Before July 1 Deadline

Gold Loans Jump 105 To 5 1 Lakh Crore By May 2026

Mirae Asset Banking Fund Leads Sector With 5 9 Monthly Return

Top Performer Bank Of India Small Cap Fund Gives 29 9 In 3 Month Returns In Small Cap Mutual Funds

Nippon India Floater Fund Tops Floating Rate Mutual Funds With 2 3 Three Month Return