By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

India’s private credit market reached $25 billion, expanding corporate funding while higher borrowing costs, opaque valuations and liquidity risks demand closer scrutiny from lenders nationwide.

India’s private credit market doubled in 5 years to around $25 billion in assets under management by the end of 2025, according to a Moody’s Ratings sector assessment covered by Moneycontrol on July 2, 2026. Annual transaction value crossed $11 billion in 2025.

Private funds are financing Indian companies that need large, long-term, or specially structured loans. This could help infrastructure, property and manufacturing projects secure capital. Yet expensive debt, layered financing and difficult-to-price loans may create repayment pressure later.

The figures below capture the size, pace and sector concentration reported by Moody’s.

The doubling implies annualised growth of about 14.9%. Moody’s said real estate remained the largest borrower segment, followed by infrastructure and utilities. Promoter financing also covered refinancing, liability management and stake purchases.

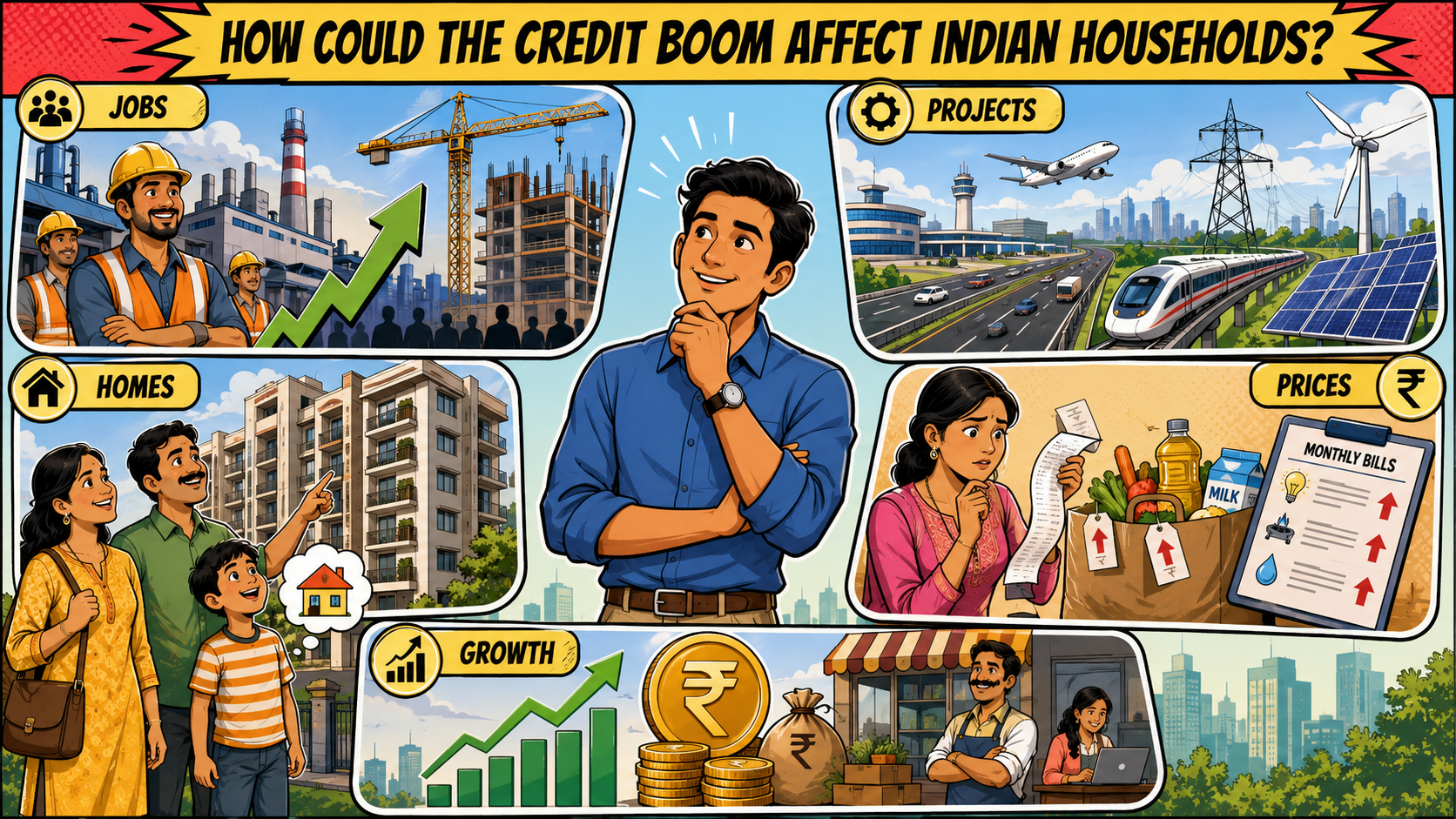

Private credit funds do not usually lend to households. Their effect reaches people through companies and projects. More funding for airports, power, renewable energy, housing and factories can support jobs, supplier payments and construction activity.

The cost can travel too. A company paying a high private-credit yield may pass part of that expense through property prices, service charges or product costs. Borrowers seeking smaller conventional loans can review bank and NBFC options through LoansJagat.

Several large 2025 transactions show where the money went.

These transactions confirm that private credit has moved beyond distressed borrowers. Established groups now use it for refinancing, expansion and complex capital requirements.

Moody’s said the Insolvency and Bankruptcy Code introduced in 2016 strengthened creditor rights. Category II Alternative Investment Fund rules also restricted fund-level leverage and improved market credibility.

The agency still flagged rising borrower leverage, opaque structures, valuation difficulty and liquidity mismatches. Its proposed direction is straightforward: lenders need tighter covenants, realistic valuations and repayment schedules linked to actual cash flow.

According to LoansJagat, private credit can restart projects that banks cannot finance, but a loan used only to delay an existing repayment may shift the problem forward. Borrowers need a defined repayment source before accepting costly capital.

India’s private credit expansion gives companies another funding route, particularly for large and complicated transactions. Its next phase will depend on loan quality, transparent pricing and borrowers generating enough cash to repay.

Moody’s placed private credit AUM at about $25 billion at the end of 2025.

Moody’s said current risks were not systemic because the Indian market remained relatively small.

Yes. Liquidity pressure may rise if investors seek early withdrawals while private loans remain locked for several years. Funds with weak cash buffers could then struggle to meet redemption requests.

To some extent, yes. Private credit can shift borrowing away from banks, making total corporate debt harder to track. Risk grows when companies borrow through multiple funds, holding firms, or layered structures.

Read Also:

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article