Widow Gets Relief As Supreme Court Limits Bank Recovery Using Article 142

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Relief came, but with conditions. The Supreme Court used Article 142 to cap a widow’s bank settlement after a COVID-19 bereavement pushed her account into default.

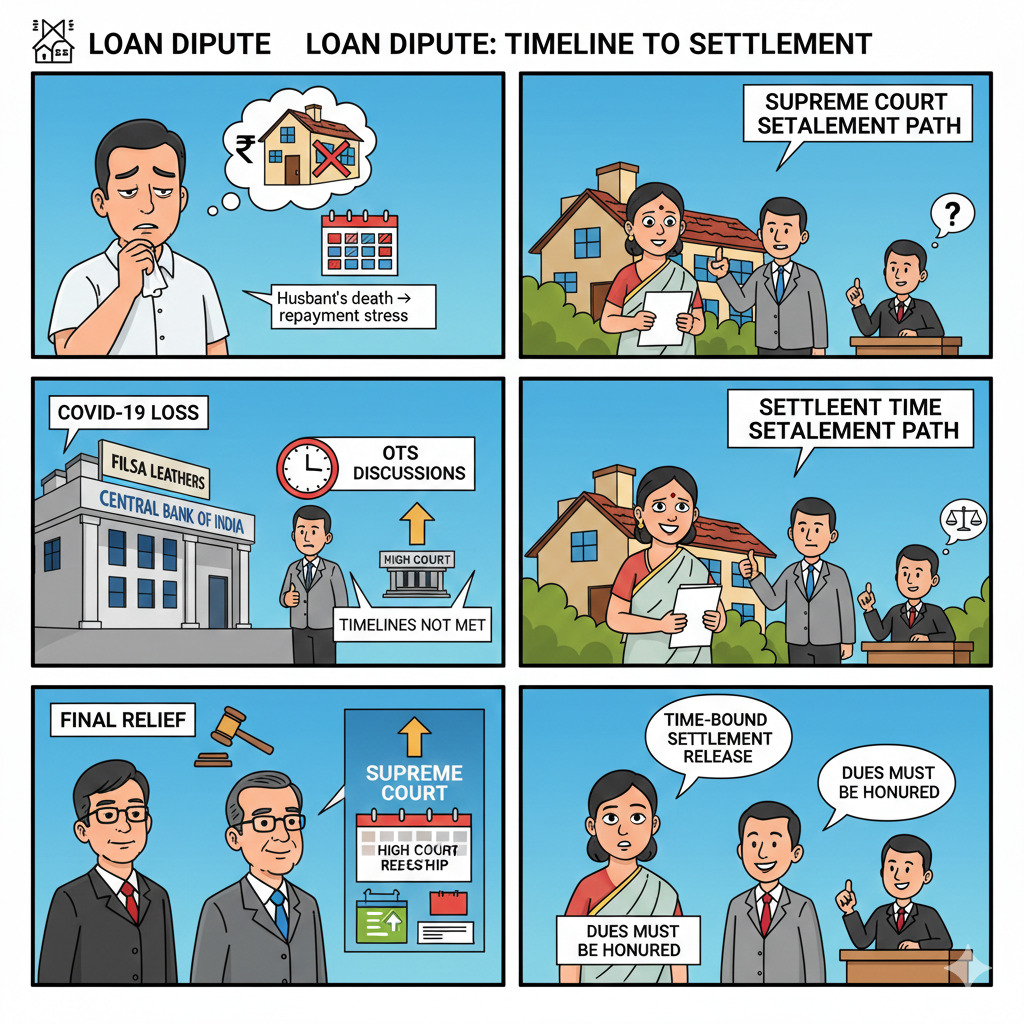

A widow from Tamil Nadu got limited relief after the Supreme Court stepped in to soften the outcome of a bank recovery process. Her husband ran a small leather business and died during the second COVID-19 wave, after which repayments slipped and enforcement steps began.

The Court said the bank’s claim could stand in law, yet a rigid approach would hurt the family disproportionately. Using Article 142, it fixed a one-time payment route that, if complied with on time, would close the account and secure release of property papers.

What Triggered The Dispute?

The conflict began with a housing-backed business loan and a failed settlement window.

The borrower’s husband, proprietor of FILSA Leathers, had taken credit facilities from the Central Bank of India and mortgaged the family home as security. After his death in 2021, repayments became difficult and the bank moved ahead with recovery steps.

The family tried to resolve it through a one-time settlement, but the payment schedule did not work out. The High Court did not grant relief, pushing the case to the Supreme Court, where the bench looked at hardship and fairness, not just strict timelines.

Read More - Section 144 Of The Income Tax Act – Best Judgment Assessment Explained

Before getting into the ruling, here are the headline figures that shaped the outcome.

These numbers are essential because the Court’s order effectively converts a contested recovery into a single, time-bound closure option.

How The Supreme Court Used Article 142?

The Supreme Court held that the Central Bank of India’s recovery stand could be valid, but it also noted the borrower’s situation was unusual and harsh. It invoked Article 142, which allows the Court to pass orders for “complete justice”, and framed a practical settlement route.

The direction was simple: deposit the fixed amount within the time granted, and the bank must close the dues and return the property documents. If the borrower misses the deadline, normal recovery steps can continue. The Court also signalled this relief is fact-specific, not a template for future defaulters.

What Happened Earlier: From OTS Talks To Court Battles?

The timeline shows a familiar pattern in stressed retail and MSME-linked accounts: settlement talks, deadline lapses, then enforcement notices. According to The New Indian Express reported on 27th January 2026,

The borrower first approached the Madras High Court after the OTS did not translate into closure and the bank proceeded with statutory recovery.

When the High Court did not grant the relief sought, the appeal reached the Supreme Court. Over time, the Court issued interim protection and also explored whether the earlier settlement framework could be revived, before finally settling on an Article 142 solution.

Also Read - Income Tax Act: Tax Provisions, Sections, Deductions & Complete Guide

To keep it clear for readers, the key milestones are set out below.

For readers who want background on how loan accounts turn into NPAs and how recovery typically proceeds after defaults, LoansJagat has a detailed overview of the standard stages from financial stress to enforcement and recovery.

Who Said What?

The bench, led by CJI Surya Kant with Justice Joymalya Bagchi, framed the relief as an exceptional response to hardship, while not questioning the bank’s legal position.

The bank’s stance, as reflected in reporting, remained that dues and timelines must be honoured, especially after an OTS expires. The borrower’s side focused on the post-bereavement financial stress and the risk of losing the family home.

Conclusion

The ruling offers a narrow exit route, not a blanket borrower relief. It also underlines how Article 142 is used sparingly, when facts are extreme and time is running out.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article