Banking And PSU Debt Funds Back In Spotlight In May 2026

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Banking and PSU debt funds are drawing attention again as investors search for lower-volatility debt options in a changing rate and tax environment.

Key Takeaways

- ETMutualFunds, on May 21, 2026, listed 5 Banking and PSU debt funds for investors to track in May 2026.

- The earlier push came after debt fund downgrades and defaults made investors prefer bank and PSU-backed papers.

Debt Investors Get A Fresh May 2026 Watchlist

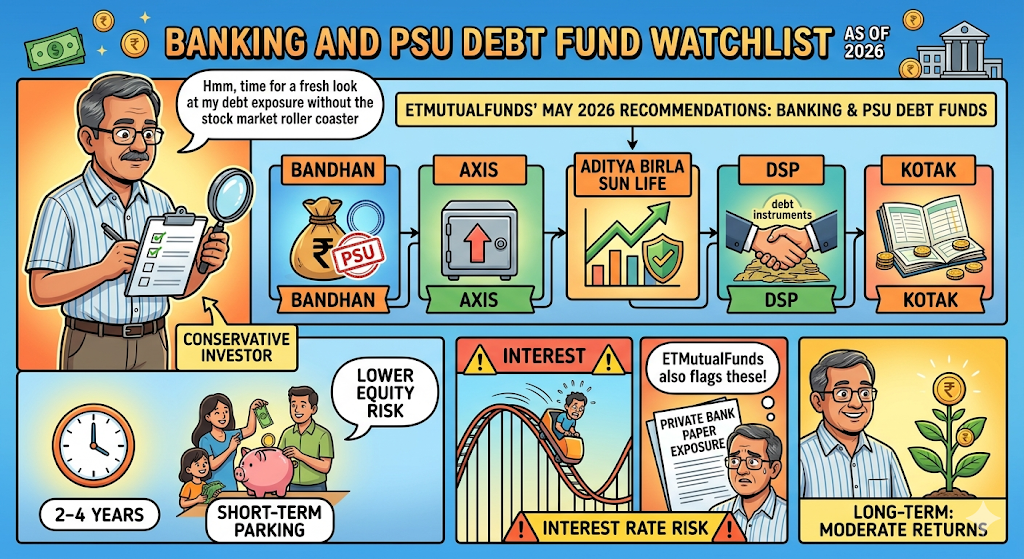

Banking and PSU debt funds are again being watched by conservative investors who want debt exposure without taking equity-like risk. ETMutualFunds’ article published on May 21, 2026 named Bandhan, Axis, Aditya Birla Sun Life, DSP and Kotak Banking & PSU Debt Funds in its May 2026 recommendation list.

In the short term, these schemes can help investors park money for 2 to 4 years. In the long term, returns may stay moderate because these funds invest in debt securities, not stocks. The negative side is interest-rate risk and private bank paper exposure, which ETMutualFunds also flagged in its May 21 report.

5 Banking And PSU Debt Funds In Focus

The table below uses ETMutualFunds’ May 21, 2026 list and Groww’s latest category data available in search results this week.

The biggest takeaway from the numbers is simple. Returns are in a narrow band, so investors should not chase only the highest return. AUM size, portfolio quality, expense ratio and consistency need checking before investing.

Why Small Savers And Salaried Investors Are Watching This Category?

For Indian households, these funds can work as a middle path between fixed deposits and higher-risk debt schemes. INDmoney, in its 2026 Banking and PSU fund page, says these funds invest at least 80% of assets in debt instruments of banks, PSUs and public financial institutions.

The positive part is that these schemes usually hold better-rated papers than many aggressive debt categories. But investors still face taxation changes. ClearTax, in its debt fund taxation page crawled last month, states that gains on debt funds bought after April 1, 2023 are taxed at the investor’s slab rate, without indexation benefit.

What Experts And Market Watchers Are Saying?

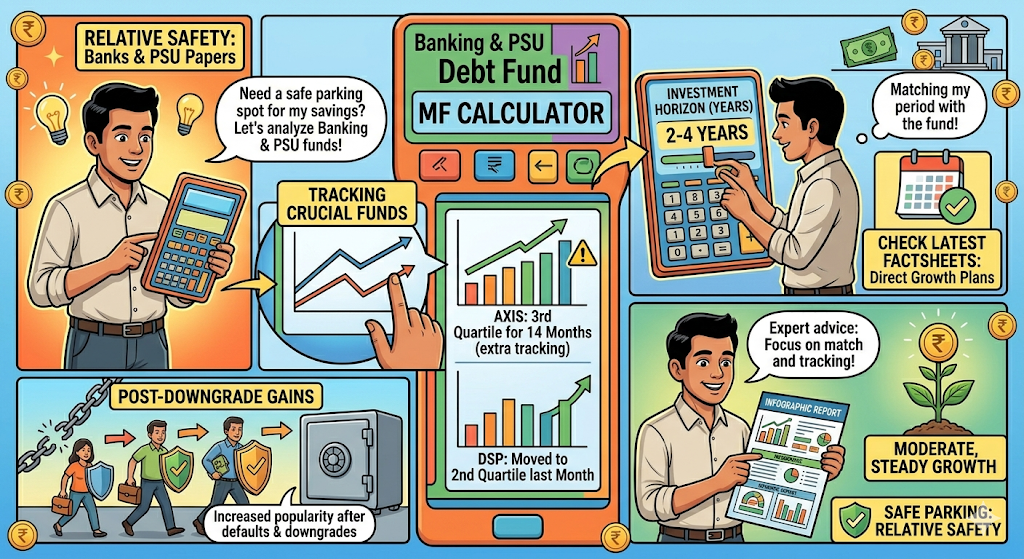

ETMutualFunds said advisors view Banking and PSU debt schemes as “relatively” safe because they invest in papers of banks and public sector companies. It also noted that the category gained popularity after debt-market downgrades and defaults.

The better approach is to match the fund with the holding period. Investors with a 2 to 4 year horizon may consider direct growth plans after checking latest factsheets. Axis needs extra tracking because ETMutualFunds said it stayed in the 3rd quartile for 14 months, while DSP moved to the 2nd quartile last month.

Previous Banking Updates Investors Should Track

Banking stocks and fund portfolios remain linked through sentiment, bond yields and institutional exposure. LoansJagat reported that HDFC Bank received approval dated May 6, 2026 for group entities to hold up to 9.95% in ICICI Bank and Kotak Mahindra Bank.

These updates do not make Banking and PSU funds risk-free. They only show why bank-linked debt portfolios are again getting attention from savers, fund advisors and market watchers.

Conclusion

Banking and PSU debt funds may suit conservative investors with a 2 to 4 year horizon. Returns, tax impact, credit quality and latest portfolio data should be checked before investing.

FAQs

Can Banking and PSU debt funds work for someone looking for lower-risk debt investment?

Banking and PSU debt funds may suit investors who want a lower-risk debt option but do not want to lock money fully in FDs. These funds mainly invest in debt papers issued by banks, PSUs and public financial institutions. So, the credit risk is usually lower than many other debt fund categories. Still, returns are not fixed. They can move with interest rates. In the Reddit discussion, users also pointed out that exit timing should depend on the investor’s goal. For many investors, a 2 to 4 year holding period may be more suitable.

Can banking and PSU debt funds be a safer choice for investors right now?

Banking and PSU debt funds may suit people who want lower risk than equity funds and can stay invested for 2 to 4 years. These funds mainly put money in debt papers issued by banks, PSUs and public financial institutions.

That gives some comfort on credit quality, but it does not remove risk. Returns can fall when interest rates move up. Investors also need to check the fund’s portfolio, expense ratio and past consistency. Since debt fund taxation changed from April 1, 2023, post-tax returns should be compared with fixed deposits before putting money in.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article