Budget 2026: Will Housing Credit Passport Speed Up Home Loan Approvals?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

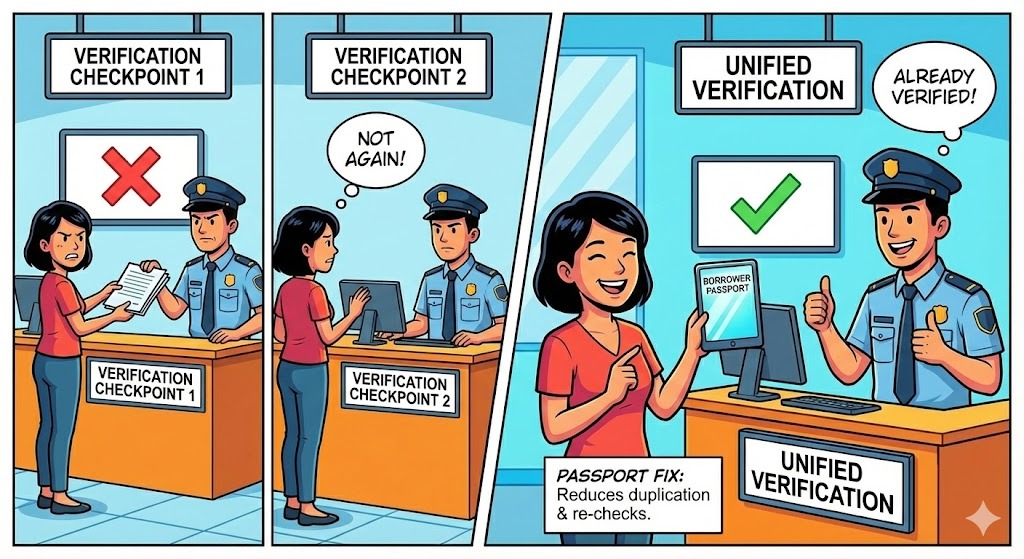

A proposed “housing credit passport” could bundle borrower data with consent, reducing repeat paperwork and trimming home loan processing from today’s 15–25 day cycle.

India’s housing finance pitch to Budget 2026 is getting sharper. Real estate and lending experts want a “housing credit passport” so borrowers do not submit the same documents to multiple teams and multiple lenders. The idea is simple: a standardised, consent-based digital snapshot of income signals, credit history and existing loans, shared at the start of the application.

Most underwriting inputs are already digital or semi-digital, but approvals still drag because verification is repeated. The proposal is being framed as a speed and predictability reform for middle-income homebuyers, without changing lenders’ final credit decision rights.

What’s Slowing Home Loans Right Now?

Loan delays are not always about risk appetite. Industry commentary flagged that the real friction sits in documentation loops, not credit availability. Over 80–85% of data points used in home-loan underwriting are already digital or semi-digital, yet processing can stretch to 15–25 days due to repeated verification steps.

Lenders still collect salary slips, bank statements, tax returns and employment details, plus run bureau checks. Some physical checks continue for address or property verification, especially when a file is tagged higher risk. For first-time buyers, the back and forth often starts after the property is shortlisted, which tightens timelines with sellers.

Here's a quick view of the current workflow and what the passport is trying to change.

The promise is faster early-stage decisions. Property and legal checks still remain outside the passport’s scope.

How The Housing Credit Passport Is Expected To Work?

The “passport” is being described as a consent-based digital snapshot of a borrower’s financial profile, covering income, credit history and existing loans, which lenders can access during the home loan application. Adhil Shetty, CEO of BankBazaar, backed the concept in these terms, positioning it as a repeat-use profile rather than a one-lender document dump.

The Budget 2026 expectation is not about replacing underwriting. It is about cutting the avoidable work inside underwriting. Vishal Valecha, COO of Easy Home Finance, said the passport is increasingly feasible because a large share of borrower data, including credit history, banking patterns and income indicators, is already available in structured formats across the industry.

On impact, experts in Hindustan Times, January 21, 2026 report estimated that a pre-verified profile could reduce manual document checks by 30–40% and cut turnaround time by 40–50%, especially for salaried and formally employed households.

There is also a caution note. Nearly 35–40% of India’s home-loan borrowers are self-employed or semi-formal earners, and their income profiles do not fit clean templates. Over-standardisation could lead to stricter terms or delayed approvals if the passport becomes overly score-driven.

What Has Built Up To This Moment?

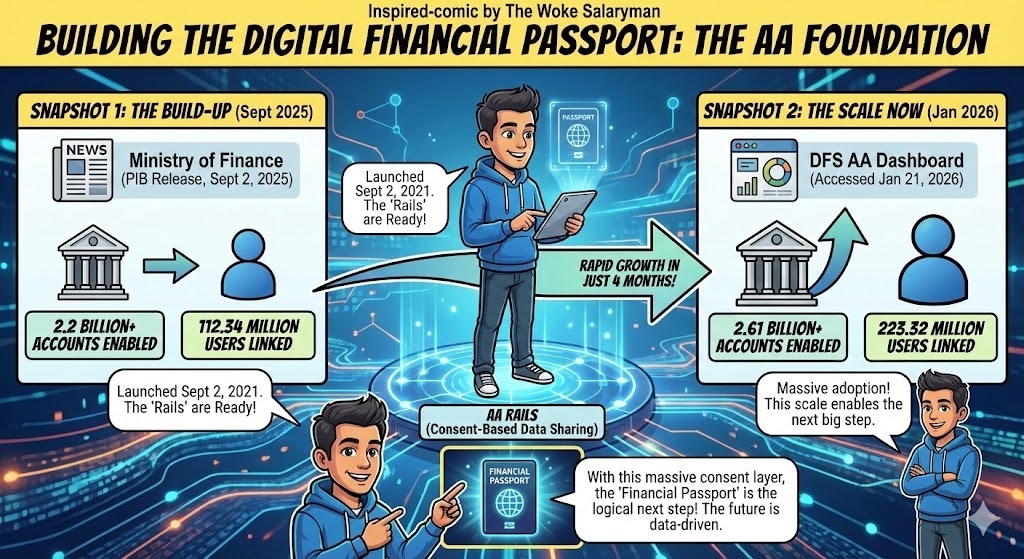

A major reason the passport idea is being pushed now is that India already has consent-based rails for sharing financial data. The Account Aggregator (AA) framework is the most visible base layer.

The Ministry of Finance through a PIB release dated September 2, 2025 (9:14 AM) said the AA framework was launched on September 2, 2021, and reported 2.2 billion+ accounts enabled for consent-based data sharing and 112.34 million users linked, alongside participation figures such as 112 institutions live as both FIP and FIU, 56 as FIP-only and 410 as FIU. The same day, coverage in ET BFSI also cited the 2.2 billion+ enabled accounts data point.

On the government’s Department of Financial Services AA page, the scale is shown higher, with 2.61 billion+ enabled financial accounts and 223.32 million users linked. This page does not show a publication date on the visible header, so it is best read as the latest dashboard view accessed on January 21, 2026.

Here is how the official snapshots compare.

Market ecosystem voices have also tracked growth. Sahamati’s press release dated September 2, 2025 said 780+financial institutions were onboard and 269+ million customer consents had been processed.

On the borrower side, platforms keep pushing pre-approvals to cut purchase friction. A LoansJagat blog dated February 24, 2025 advised buyers to seek a sanction letter that is typically valid for 3–6 months, calling pre-approved loans a speed lever during property selection.

Stakeholder Voices And Concerns

Shetty’s view is that a consent-based borrower snapshot can reduce stress and repeat checks. Valecha’s view supports faster processing but warns on data freshness, consent management and flexibility for self-employed borrowers.

Broader Budget 2026 coverage also shows a wider real estate wishlist around affordability and policy support, so the credit passport is landing in a larger demand cycle.

Conclusion

Budget 2026’s housing credit passport pitch is a speed reform, not a subsidy. If it stays consent-led and flexible, it could cut the 15–25 day approval drag significantly.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article