Finance Bill 2026: Sitharaman Pushes Trust-Based Tax Administration

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Finance Bill 2026 signals a softer compliance route for honest taxpayers, but keeps enforcement tools intact through selective retrospective fixes, tighter procedures and targeted tax changes.

Finance Bill 2026 has moved beyond a routine Budget measure and become a wider tax administration story. In the Lok Sabha on 25 March 2026, Finance Minister Nirmala Sitharaman said a trust-based tax administration sits at the core of the Bill and is intended to reduce hardship for honest taxpayers.

The Finance Bill, 2026, listed on the India Budget portal and the Income Tax Department’s Finance Bills page, was uploaded on 2 February 2026. The Lok Sabha later cleared it by voice vote with 32 government amendments, pushing the debate from tax rates to how taxpayers are dealt with.

What The Bill Actually Changes For Taxpayers?

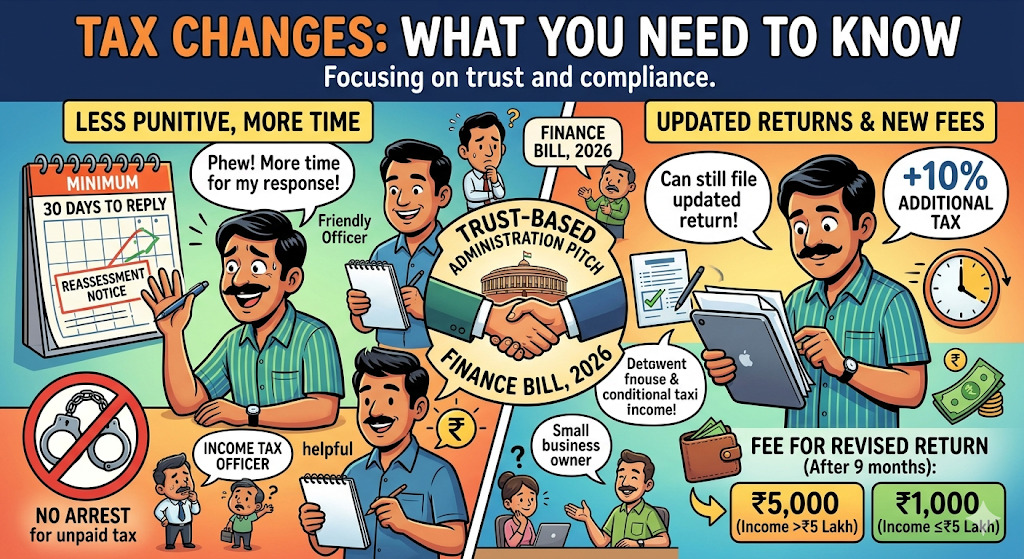

The government’s pitch is simple: fewer disputes, more compliance, quicker closure. The Bill gives taxpayers a minimum 30-day window to respond to reassessment notices and removes the Income Tax Recovery Officer’s power to arrest assessees for unpaid tax demand, while retaining recovery through attachment and sale of assets.

The Memorandum to the Bill, dated 2 February 2026, also says updated returns can be filed even after a reassessment notice, but with an extra 10% additional tax in such cases. It further proposes Section 234-I, with a fee of ₹5,000 where total income exceeds ₹5 lakh and ₹1,000 where it does not, if a revised return is filed after 9 months.

Read More : 80 IAC Tax Exemption

These changes make compliance less punitive on paper, but not lighter in every area.

How The Story Reached This Stage?

The earlier Budget documents had already shown that the Centre wanted a smoother transition to the new tax framework from 1 April 2026. The passed Bill then added politically and commercially relevant changes.

According to ET reports published on 26 March 2026, the surcharge on buyback-related capital gains has been capped at 12%, and the turnover threshold for startup tax holiday eligibility has been raised to ₹300 crore from ₹100 crore. At the same time, the Bill allows retrospective reopening of some proceedings struck down on technical grounds and validates certain past orders, showing that the government is easing process but protecting revenue action too.

LoansJagat’s report on new income-tax forms, published on 24 March 2026, also flagged that taxpayers will start seeing the compliance shift from 1 April 2026.

That is why the Bill is being read as both reform and control.

Also Read : India Doubles Tax Holiday

Who Said What On The Amendments?

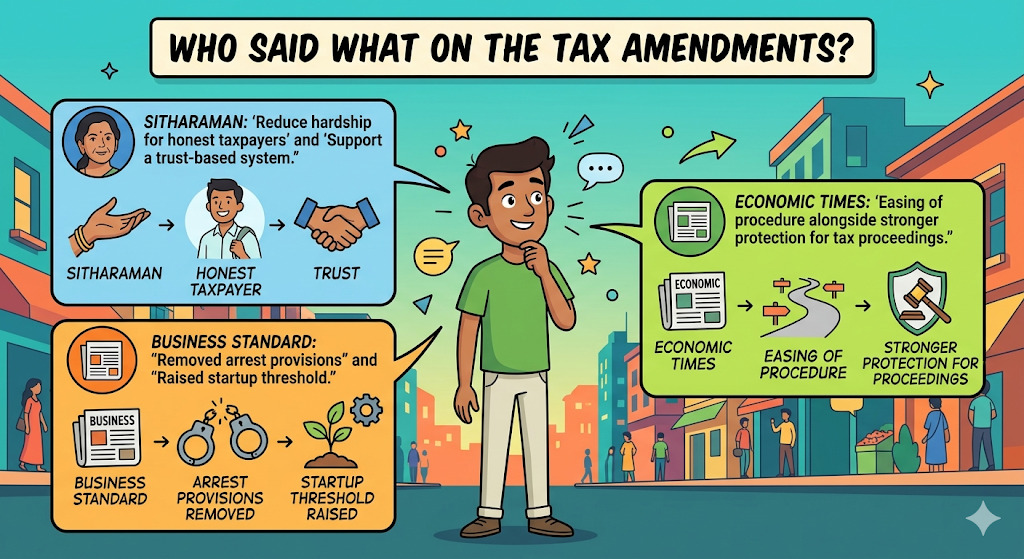

Sitharaman said the Bill is meant to reduce unnecessary hardship for honest taxpayers and support a trust-based system.

Business Standard reported that the changes also removed arrest provisions and raised the startup threshold. Economic Times noted that the easing of procedure came alongside stronger protection for tax proceedings.

Conclusion

Finance Bill 2026 is not just a tax proposal. It is a clear reset in how compliance, reassessment and recovery are being framed.

It offers relief in procedure, but the enforcement backbone stays firmly in place.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article