By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

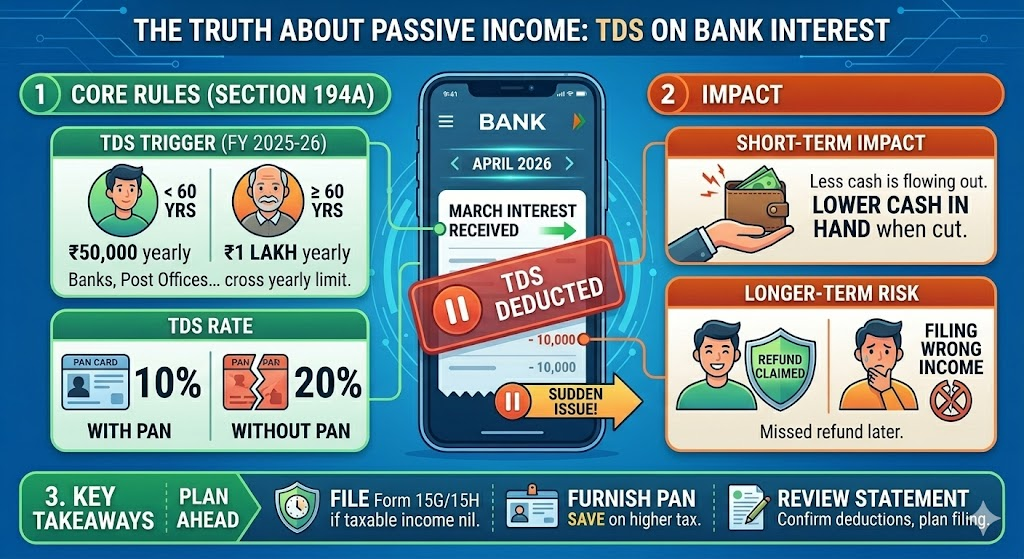

Banks can deduct TDS on deposit interest once annual limits are crossed. For savers, the bigger issue is tracking thresholds, PAN status, and return-time mismatches.

For many depositors, bank interest still looks like easy passive income until TDS suddenly shows up in the account statement. That has become a sharper issue after Budget 2025 changes on interest thresholds, especially for senior citizens. The short-term impact is lower cash in hand when TDS is cut. The longer-term risk is filing the wrong income or missing a refund later.

The core rule remains under Section 194A. Banks, post offices and co-operative banks deduct TDS on eligible interest once the yearly limit is crossed. The standard rate listed by the Income Tax Department is 10%. If PAN is not furnished or is inoperative, the deduction can go higher under the tax rules.

The latest official and news-backed position is straightforward. For FY 2025-26, the TDS trigger on deposit interest is shown at ₹50,000 for regular depositors and ₹1,00,000 for senior citizens. News coverage around Budget 2025 also reported that the senior citizen threshold was doubled from ₹50,000 to ₹1 lakh.

Before looking at the numbers, one point is worth keeping in mind. TDS is not the final tax. Interest can still be taxable even where no TDS is deducted because the threshold was not crossed.

That is where the impact spreads wider than fixed deposit investors alone. Pensioners, small savers and households depending on interest income need to watch cumulative yearly interest, not just one deposit receipt or one branch statement.

The previous threshold for senior citizens was ₹50,000, and Budget 2025 announced the jump to ₹1 lakh to reduce smaller TDS transactions. Business Standard and The New Indian Express both reported the change on 1 February 2025, in line with the official Budget release.

Tax professionals and banking explainers are also repeating another warning. Depositors should verify TDS entries in Form 26AS and AIS, because Form 26AS now largely shows TDS/TCS data while AIS carries broader reported information. A practical explainer on Section 194A is also available on LoansJagat.

For most depositors, the practical fix is simple. Track interest bank-wise, keep PAN details updated, and reconcile TDS before filing returns. That reduces refund delays and surprise tax notices later.

Bank TDS on interest is not new, but the threshold changes have made it more relevant in 2026. For depositors, early checks are better than fixing a mismatch at ITR time.

Related Financial News | |||