By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

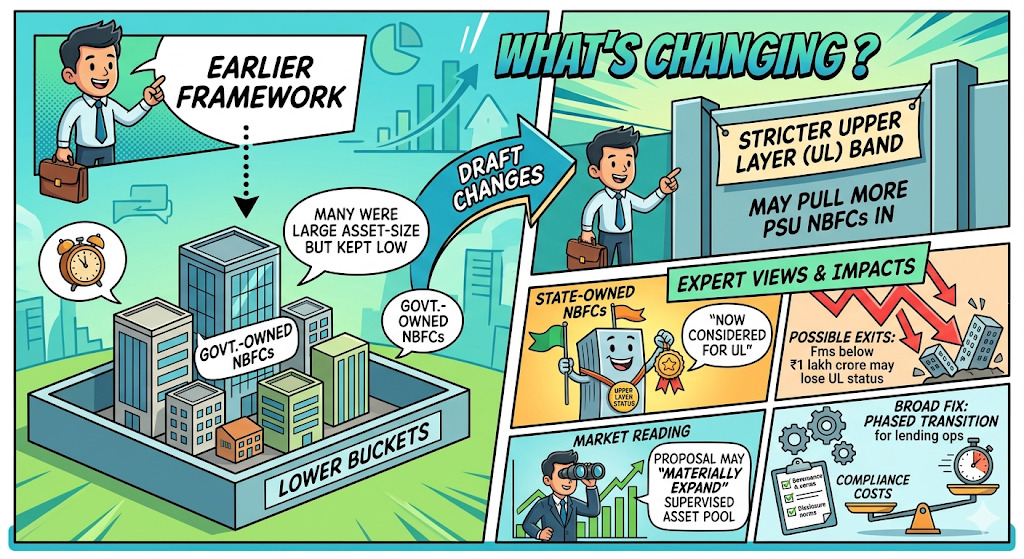

A draft change in NBFC classification could sharply widen stricter oversight, with CareEdge estimating Upper Layer coverage may rise to 70% of sector assets.

India’s large non-bank lenders could be headed for tighter rules if the proposed Upper Layer filter is finalised. The draft shifts the trigger to an asset-based threshold of ₹1 lakh crore+, replacing the older scoring-led method. CareEdge said this could more than double asset coverage under the tougher bucket to around 70% as of September 2025.

In the near term, this can raise compliance, governance and disclosure costs for affected firms, including some state-owned NBFCs that were earlier outside this bracket. Over time, it may tighten supervision across a larger part of the shadow banking space, though firms facing reclassification may have to adjust capital planning and reporting.

The shift is simple on paper but wide in impact. Under the proposal, any NBFC crossing ₹1 lakh crore in total assets may move into the Upper Layer. That is a major break from the present selection framework, where only 15 Upper Layer NBFCs accounted for 30.2% of total sector assets at end-March 2025.

For borrowers, the impact may not show up overnight in loan pricing, but stricter oversight of large NBFCs can improve balance-sheet discipline and disclosure.

That is relevant because NBFCs remain a major credit channel for retail borrowers, MSMEs and vehicle finance users across India. For a quick explainer on how NBFCs work, this LoansJagat guide is useful.

The earlier framework kept most government-owned NBFCs in lower buckets, even though many were large by asset size. The draft changes that and may pull more PSU-linked players into the stricter band. Some reports also flagged that firms below the new threshold could move out over time, while larger entrants may come in.

CareEdge’s Sanjay Agarwal said the proposed changes may “materially expand” asset coverage under the Upper Layer. Industry coverage in ETBFSI said likely entrants may already meet capital norms, but governance and disclosure requirements would tighten. The broad fix experts point to is a phased transition so that compliance costs do not spill too quickly into lending operations.

If finalised, the rejig could widen stricter supervision across India’s largest NBFCs much faster than earlier expected. The next focus will be on who moves in, who moves out, and how firms absorb the added compliance load.

Related Financial News | |||