Entrepreneur Went From ₹10 Lakh Monthly Income to Seeking ₹6 Lakh Loan, Big Lesson for Founders

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

A founder’s cash crunch has put one hard lesson in focus for entrepreneurs: never take a loan before checking whether the real problem is weak cash flow.

Singapore-based entrepreneur Yashank Jhamb has triggered debate after saying he went from earning ₹10 lakh a month to borrowing ₹6 lakh from friends to pay salaries. In posts cited by multiple reports, he blamed early founder mistakes and what he called “toxic Indian customers” for the slide.

The sharper takeaway for business owners is not the outrage around clients. It is this: borrowing works only when the business can collect on time, protect margins, and handle repayment without depending on hope.

The must-know thing before taking a loan

Jhamb’s account points to a basic problem many small founders ignore. Revenue on paper is not the same as cash in hand. He said survival mode pushed founders to accept weak terms, unclear scope and delayed payments. That becomes dangerous when salaries, vendor dues and EMIs start lining up together.

Before borrowing, an entrepreneur has to ask one blunt question: is the loan funding growth, or just covering unpaid invoices and bad client behaviour? If it is the second one, debt can deepen the problem, not solve it. LoansJagat also notes that business loans are useful for cash-flow management only when repayment capacity and financial records are already in place.

Read More -CEOs Who Took Huge Loans & Built Billion

Key reports and source links

The backlash around “Indian vs international clients” may grab attention, but the loan lesson sits elsewhere. Even a business earning ₹10 lakh a month can run into trouble if collections are late, contracts are loose, and founder decisions stay reactive. That gap between income and actual liquidity is where many repayment problems begin.

What entrepreneurs should check before borrowing?

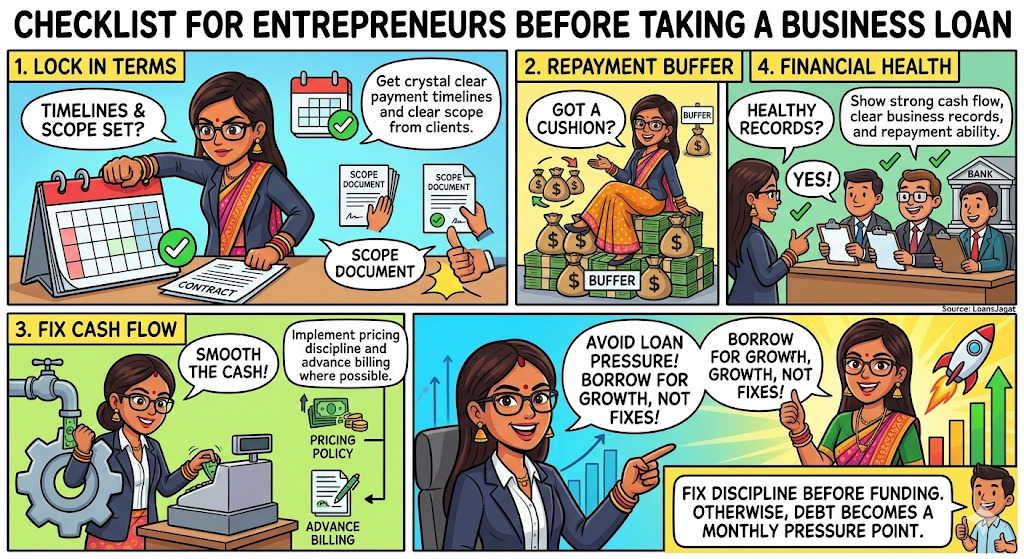

A founder planning to take a loan should first lock three things: payment timelines, scope clarity, and a repayment buffer. LoansJagat says lenders look closely at cash flow, business records and repayment ability before approval. That is also a practical checklist for founders themselves.

A loan should come after the founder fixes pricing discipline, advance billing where possible, and a cushion for at least 2 to 3 bad payment cycles. Otherwise, debt turns into a monthly pressure point.

Conclusion

The must-know thing for entrepreneurs planning to borrow a loan is simple: do not use debt to hide a broken cash-flow system.

Borrow when collections are stable, contracts are tighter, and repayment is visible. Jhamb’s story is a warning that monthly revenue can look healthy while the business is already under strain.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article