Can RBI Profit From Minimising Digital Frauds?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

India’s digital payments network is expanding fast, and fraud is rising with it. If scams decline, RBI may not gain directly, but the wider system could.

India’s digital payments surge has created a parallel rise in fraud exposure. The Ministry of Finance said on 10 January 2026 that digital payment transaction volume rose to 22,831 crore in FY2024-25 from 2,071 crore in FY2017-18, while transaction value increased to ₹3,509 lakh crore from ₹1,962 lakh crore.

At the same time, Reuters reported on 6 February 2026 that 65% of reported frauds involved losses below ₹50,000. This has triggered a larger policy question: if digital fraud reduces, can RBI benefit through lower system costs, stronger trust and reduced pressure across the payments ecosystem?

Will Lower Fraud Improve RBI’s Financial Position?

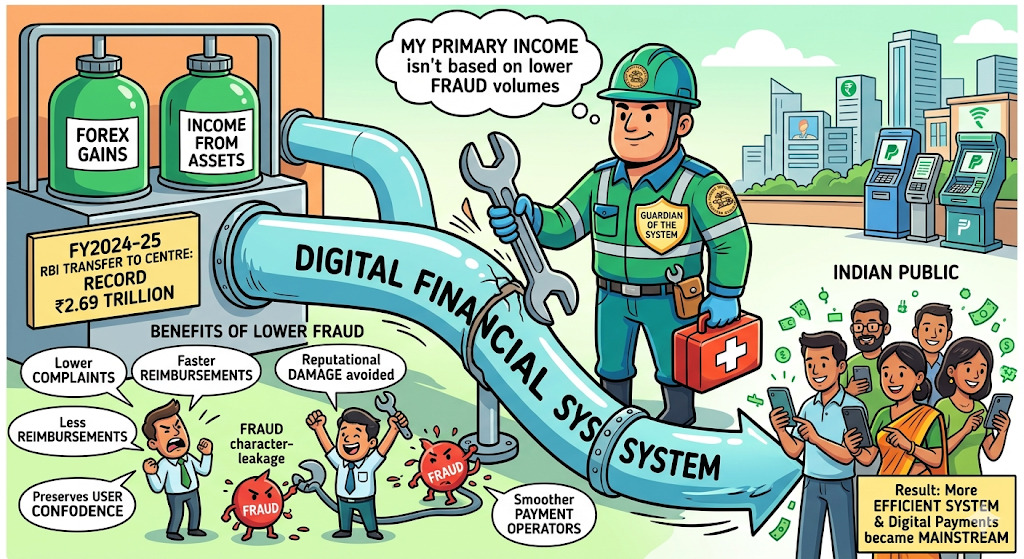

RBI will not profit from fewer frauds in a direct commercial way. Its earnings do not come from digital scam volumes. But lower fraud can improve the efficiency of the system it regulates.

Read More -RBI’s ₹50,000 Cap on Digital Fraud Claims

Reuters reported on 23 May 2025 that RBI transferred a record ₹2.69 trillion surplus to the Centre for FY2024-25, largely due to foreign exchange gains and income from financial assets.

That means fraud reduction does not create revenue by itself. Still, it can lower complaints, reimbursements, disruption and reputational damage across banks and payment operators. A safer digital network also helps preserve user confidence at a time when digital payments have become mainstream.

There is also a cost angle. Business Standard reported on 29 May 2025 that security printing expenditure rose 25% to ₹6,372.8 crore in FY25.

If safer digital payments push even a small shift away from cash over time, that can ease some pressure attached to currency logistics. It is not a direct gain, but it supports a more cost-efficient financial environment.

What Has Led To This Point?

The anti-fraud push has been gathering pace. Reuters reported on 6 March 2026 that draft guidelines proposed compensation of up to 85% of the net loss or ₹25,000, whichever is lower, for eligible small-value fraud victims. Customers would have to report such incidents within 5 days to remain eligible. The objective is to reduce customer distress and speed up resolution.

Alongside this, fraud prevention is moving upstream. LoansJagat, in a report published on 9 July 2025, said banks were being urged to integrate the Department of Telecommunications’ Financial Fraud Risk Indicator system for real-time alerts on risky mobile numbers.

Also Read - RBI Kill Switch That Could Save Bank Account

PIB had also reported on 2 July 2025 that this integration was being positioned as a landmark step in cyber fraud prevention. The shift shows that the focus is no longer only on compensation after a fraud, but on stopping risky transactions earlier.

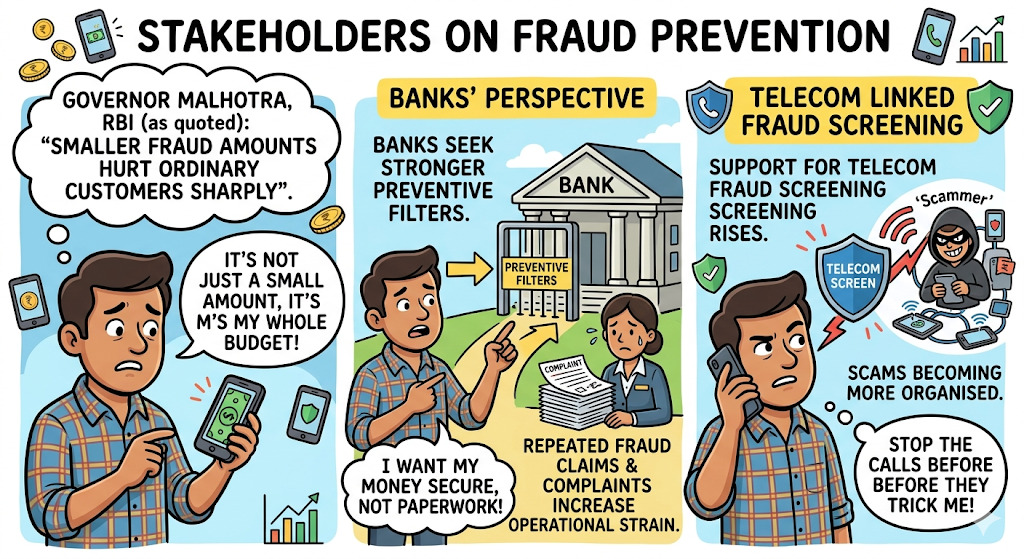

What Stakeholders Are Saying?

Governor Sanjay Malhotra, as quoted by Reuters on 6 February 2026, said smaller fraud amounts may look limited in value but can hurt ordinary customers sharply.

Banks are expected to back stronger preventive filters, because repeated fraud claims and complaint handling increase operational strain. Telecom-linked fraud screening has also gained support as scams become more organised.

Conclusion

RBI may not earn directly from lower digital fraud. But if fraud falls, the financial system becomes more trusted, less costly and easier to run.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article