Home Loan Balance Transfer Explained: Savings After Recent Rate Cuts

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

With a repo rate at 5.25%, borrowers are checking if lenders passed on cuts. A home loan switch can trim EMIs or tenure, saving lakhs.

Floating-rate borrowers are scanning their loan statements after a sharp easing cycle. A Reuters poll dated January 29, 2026 said the policy rate has been cut by 125 bps since February 2025, and most economists expect it to stay around 5.25% through 2026.

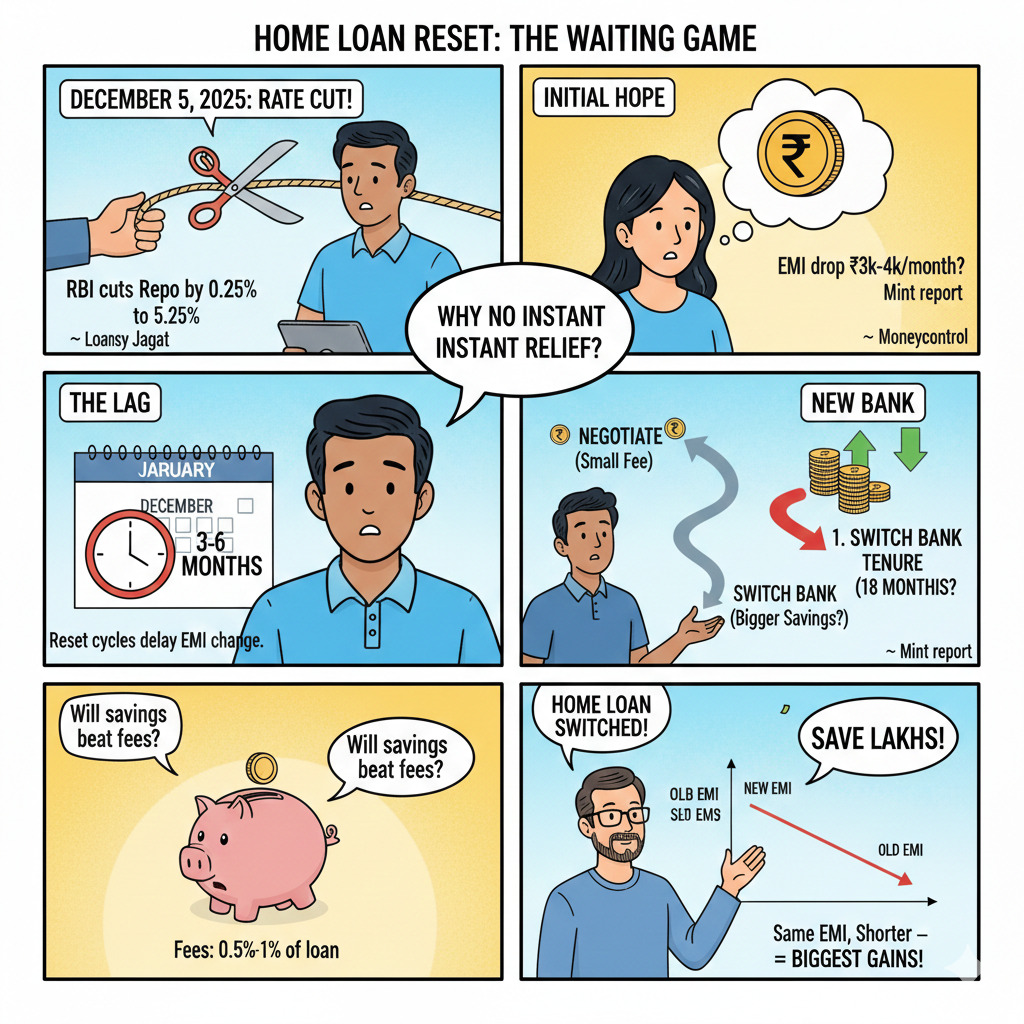

Separately, cleartax, updated on December 24, 2025, notes the repo was cut by 25 bps to 5.25% on December 5, 2025.

Yet, many borrowers are not seeing an instant dip in EMI. The gap between rate cuts and actual relief is pushing a fresh question into living rooms and loan desks. Should the borrower negotiate with the current lender or switch the loan to another bank or HFC.

How A Refinance Can Save ₹5 Lakh To ₹9.55 Lakh?

Read More - How to Transfer a Personal Loan to Another Bank

Savings depend on 3 things: outstanding principal, remaining tenure, and the interest-rate gap offered by the new lender. A small gap looks minor monthly, but over years it builds up.

Before looking at fees, here is a clean illustration using a common case: ₹50 lakh outstanding, 15 years remaining, rate moving from 9.00% to 8.00%.

The second approach is where the bigger gains sit. Same EMI, faster principal reduction.

Now, borrowers still need a practical reality check. Fees can eat into savings. Paisabazaar says processing fees on home loan transfers typically range 0.5% to 1% of the loan amount.

What Happened Earlier: Rate Cuts, EMI Expectations, And The Reset Lag?

This switch conversation picked up pace after the December policy move. A Reuters report dated December 5, 2025 said the repo was cut by 25 bps to 5.25% and the central bank announced liquidity steps including ₹1 trillion in bond purchases and $5 billion in FX swaps.

Moneycontrol report published December 5, 2025 (23:16 IST) said EMIs and interest rates are set to fall after the cut, estimating an EMI drop of about ₹3,000 to ₹4,000 for a ₹50 lakh loan.

On the broader cycle, Moneycontrol (published December 18, 2025, 16:00 IST) wrote that the repo fell to 5.25% from 6.5% after 4 cuts in 2025.

Still, borrower relief can come late. Loans Jagat, in a piece published January 11, 2026, said even repo-linked loans usually reset on predefined dates, often every 3 or 6 months, so the EMI may not change on the day of a policy cut.

A separate mint report dated December 10, 2025 also flags the same waiting window, quoting an advisor who suggests giving it 3 to 6 months before escalating the issue or taking action.

Also Read - Home Loan Balance Transfer Gains Momentum

Borrowers, then, are increasingly comparing two paths: pay a small repricing fee and negotiate, or do a full balance transfer if the spread gap is wider.

Before deciding, a timeline snapshot helps.

After this wave of reporting, the consumer decision has narrowed to a simple test: will savings beat the costs.

Stakeholders Weigh In: What Lenders And Advisers Are Signalling?

In the December 5, 2025 coverage, Reuters quoted RBI Governor Sanjay Malhotra describing the economy as being in a “rare goldilocks phase” while announcing liquidity measures alongside the rate cut.

On the borrower side, mint December 10, 2025 report quoted investment advisor Shankar K advising borrowers to wait 3 to 6 months for transmission, and then consider next steps if the lender has not reduced rates or tenure. Loans Jagat January 11, 2026 explainer also nudges borrowers to track reset dates before assuming the cut is not reflected.

Conclusion

With repo at 5.25%, a switch can save lakhs when the rate gap is real and tenure left is long. The biggest wins often come from holding EMI steady and cutting tenure.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article