By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

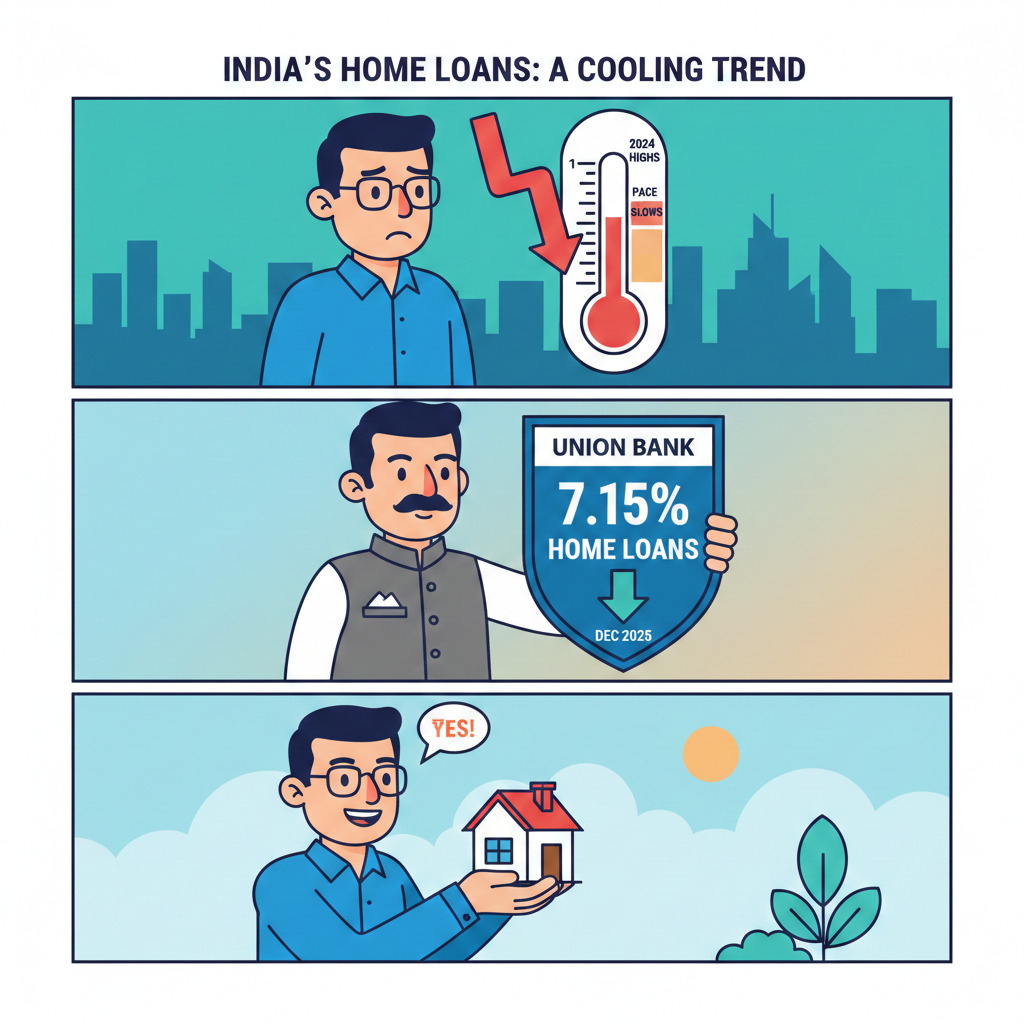

US mortgage rates have slipped below 6% again, but Indian home-loan rates are still mostly above 7%. Any further drop hinges on policy signals and bank pricing.

In India, borrowers are watching if the easing cycle of 2025 can still translate into lower home-loan offers in 2026. Aggregated lender listings show home loans starting at 7.10% p.a. as of 04 February 2026, with actual rates varying by credit score, LTV and lender policy.

In practice, loan eligibility in PSU banks and private lenders also shapes the final offer, since income type, bureau score and property documents can change rate bands.

Indian home loans have cooled from 2024 highs, but the pace has slowed. Several lenders trimmed repo-linked benchmarks after the final cut of 2025, and competition has kept “starting rates” near the low-7% band for top profiles. For instance, Union Bank of India reduced home-loan rates by 30 bps to 7.15%, effective 18 December 2025, as reported on 24 December 2025.

A key indicator is credit demand. Outstanding commercial credit crossed ₹300 lakh crore by end-January 2026, up 14.7% year-on-year, pointing to strong borrowing appetite even after rate cuts. Strong demand can keep banks selective with aggressive cuts, especially for average-risk borrowers.

Here is a clear snapshot of what borrowers are comparing.

The key point is simple. Global rates can set sentiment, but Indian pricing will move mainly with domestic liquidity, competition, and banks’ internal spreads.

India’s easing cycle in 2025 was meaningful, but transmission has not been uniform across borrowers. Reports tracking the policy path noted cumulative cuts of 125 bps from February 2025 to December 2025, taking the headline rate from 6.50% to 5.25%.

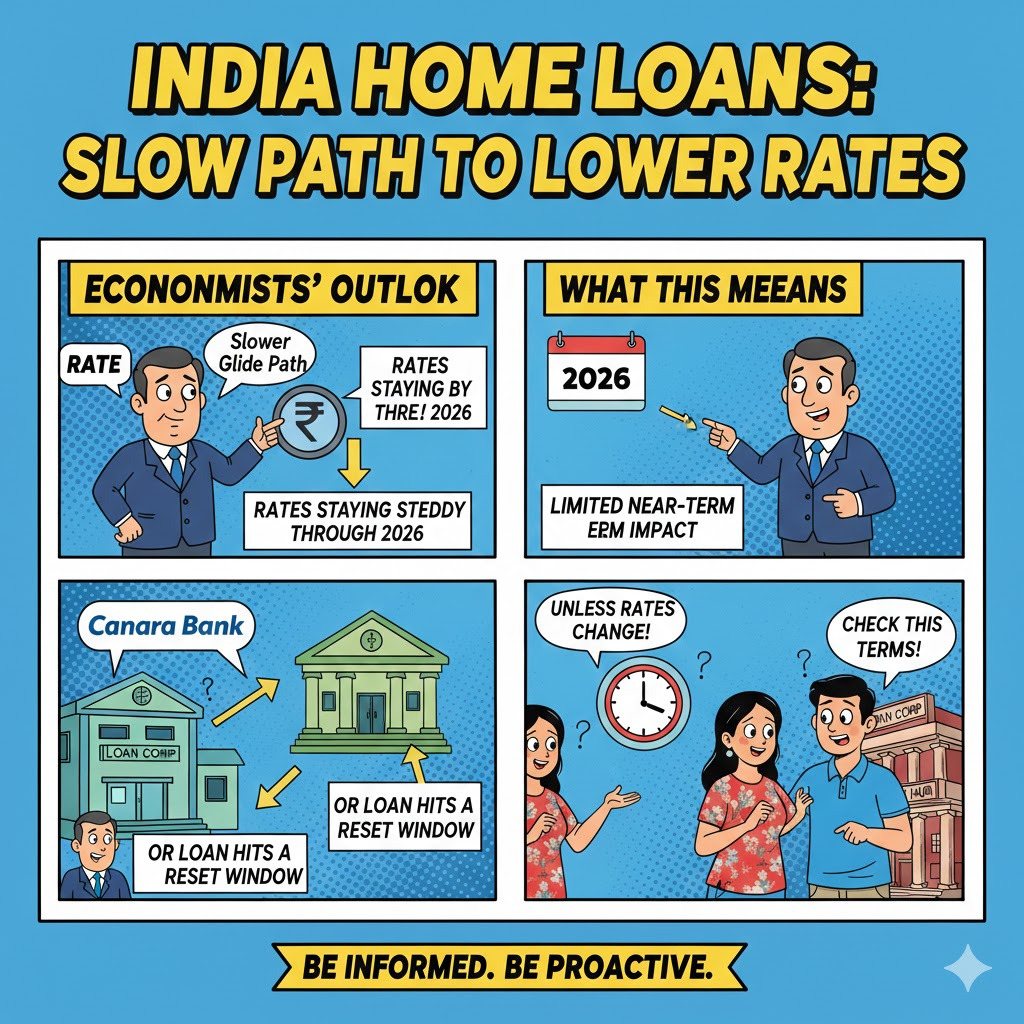

Banks responded in pockets. A December 2025 report highlighted that Canara Bank cut its repo-linked benchmark by 25 bps to 8.00%, effective 12 December 2025, with implications for EMI resets on linked loans.

Meanwhile, external factors overseas have pulled US mortgage rates down too. Freddie Mac’s series shows the US 30-year average at 6.01% on 19 February 2026, versus 6.85% a year earlier.

Even then, what moves EMIs in India is often administrative timing, many borrowers see changes only when reset windows arrive, or when the loan application process online is completed and the lender locks pricing based on profile and property checks.

Here are the recent triggers that decide whether Indian borrowers see more relief.

It is also worth noting that borrowers on reset dates feel changes first. Others may see no EMI change until the next repricing.

Economists surveyed by Reuters broadly expected rates to stay steady through 2026, signalling a slower glide path for lending rates. Borrower-facing explainers have echoed that near-term impact is limited unless the bank revises spreads or the loan hits a reset window.

In the US, Freddie Mac described the latest move as a continuation of gradual affordability improvement, even with rates still around 6%.

LoansJagat’s February 2026 coverage said the RBI’s status quo at 5.25% typically means no sudden move in floating EMIs unless a bank resets rates or changes the spread.

Borrowers looking to reduce their EMI can explore a home loan balance transfer on LoansJagat and compare options across lenders based on their current rate, outstanding amount and reset cycle.

Indian home-loan rates are easing, but the next cuts are likely to be small and targeted. Borrowers will gain more by shopping for spreads and resets than by tracking overseas headlines.

Related Financial News | |||