By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

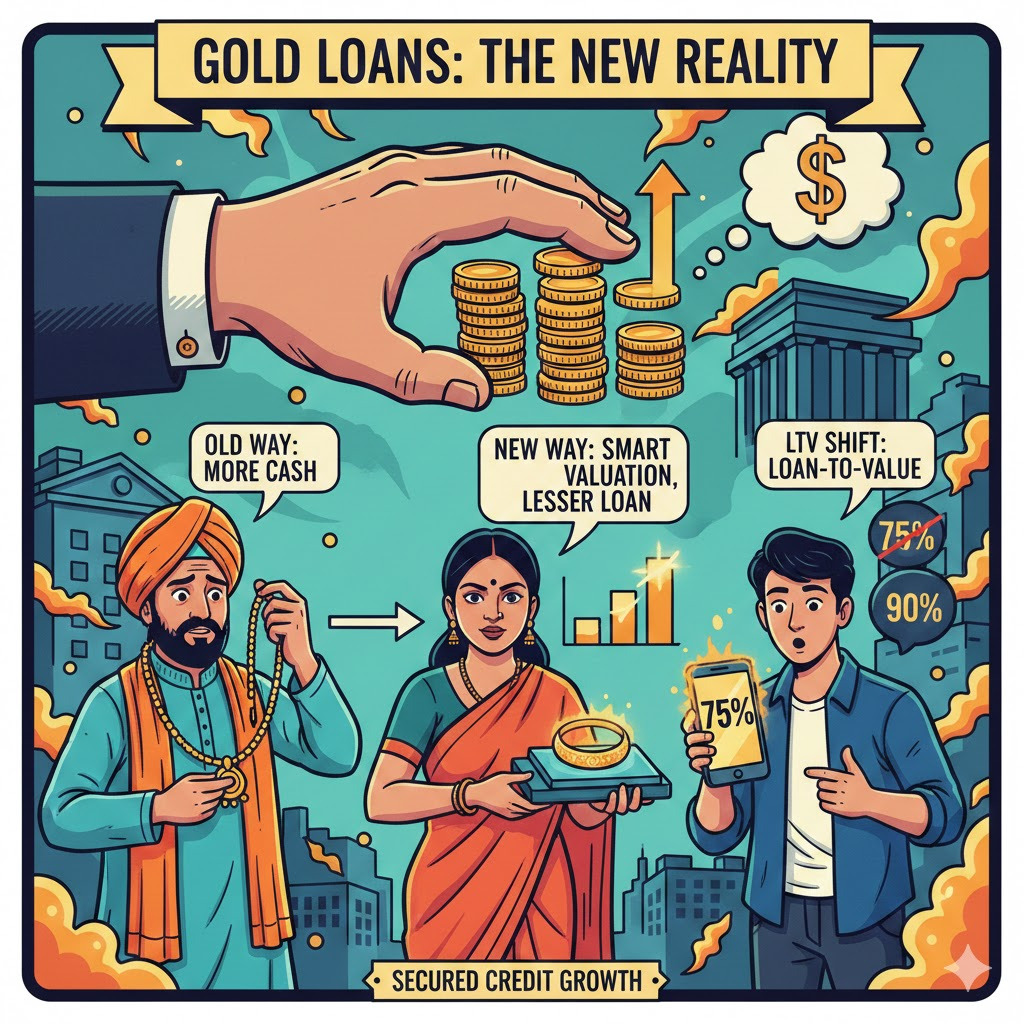

Gold loans are surging again as banks chase secured credit growth. Newer valuation and LTV practices are changing how much borrowers can actually raise.

Gold loans have become a high-velocity retail product in India, driven by rising bullion prices and tighter appetite for unsecured lending. Bank credit data tracking gold-backed borrowing shows a sharp jump in outstanding balances, and lenders are competing hard on speed and pricing.

At the same time, borrower protection and collateral handling have moved up the agenda, with new-age rules and stricter processes being discussed and rolled out. For customers, the key question is simple: how is the loan amount calculated, who qualifies quickly, and what happens during settlement or default, especially when households are also comparing options like a personal loan for urgent cash needs.

The immediate trigger is demand for secured cash, especially among small borrowers and traders, along with lenders pushing gold loans as a lower-risk retail asset.

Read More : IIFL Suvarna Dhara Gold Loan Launched

Outstanding loans against gold jewellery rose 128.5% YoY to ₹3.38 lakh crore in Oct 2025 and increased 63.6% since March 2025, as per data cited in a Times of India report dated Nov 29, 2025.

Before getting into calculations, here is how the lender environment is shifting:

This fast growth is now reshaping how lenders price, process, and cap loans for different ticket sizes. It is also changing borrower behaviour, with some customers weighing gold loans against an instant personal loan when speed is the priority.

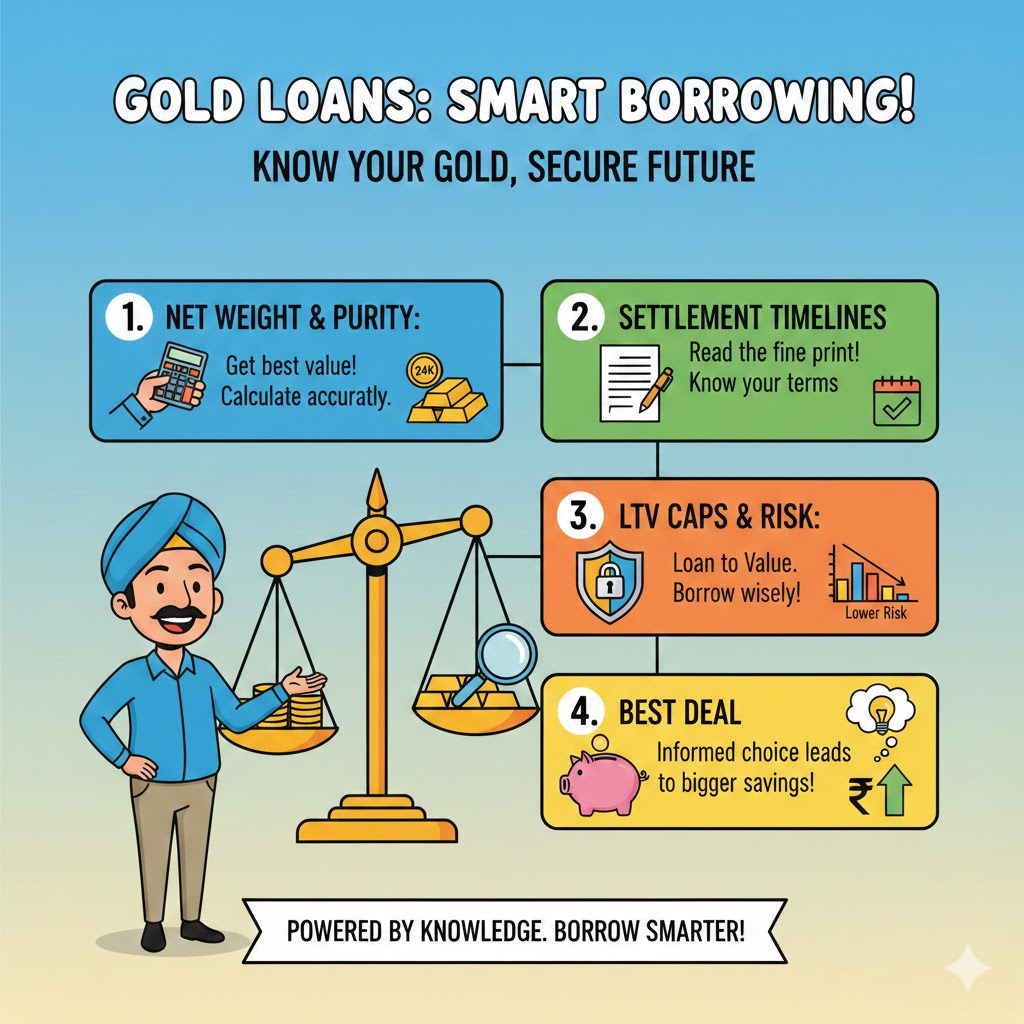

Gold loan underwriting is quick, but not random. Lenders begin with net weight (stones and non-gold parts deducted) and then test purity. The value is linked to a daily reference gold price, after which lenders apply a Loan-to-Value (LTV) cap to decide the final sanction.

For borrowers, the practical formula looks like this:

Eligible loan = (Net gold weight × Purity-adjusted rate) × Permitted LTV

Loan ticket size has become a key lever. Several market explainers highlight a tiered approach where smaller loans can fetch higher LTV, while larger loans are tighter. LoansJagat’s report notes higher LTV for small-ticket borrowers and a clear timeline for collateral return.

In parallel, lenders are also tightening checks across retail credit, including personal loan eligibility criteria, as they manage risk across secured and unsecured products.

At the same time, growth is visible in lender books. Muthoot Finance reported gold-loan AUM rose 47% to ₹1.32 trillion for the July–September 2025 quarter, while profit jumped 87.5% to ₹23.45 billion, Reuters reported on Nov 13, 2025.

For anyone comparing repayment outgo across products, LoansJagat’s personal loan emi calculator helps estimate monthly EMI, total interest payable, and total repayment before applying.

The story built up through 2025, when regulators and the government flagged sharper oversight for gold-backed lending as volumes accelerated. Reuters reported on Apr 9, 2025 that the central bank proposed stricter processes, including better collateral checks and end-use monitoring, after a rapid rise in gold-loan demand.

By mid-2025, there was also a policy push to keep small borrowers comfortable while tightening risk controls for larger tickets. The Economic Times reported on May 30, 2025 that the Finance Ministry sought relief for small gold loans in the draft framework.

Also Read : India's Gold Loan Rules Have Changed

A key upcoming date is Apr 1, 2026, when the revised gold-loan norms are expected to take effect, as reported by Times of India on Jun 7, 2025.

Below is a quick snapshot of lender growth signals that shaped the conversation:

The competitive heat is also visible in public markets coverage. Economic Times reported on Feb 24, 2026 that smaller private and PSU banks with large gold-loan books are seeing balance sheet gains during the bullion rally.

CRISIL linked the surge to elevated gold prices and a shift towards secured credit, projecting strong AUM growth through March 2027. Muthoot pointed to strong demand and raised FY26 gold-loan growth guidance to 30% to 35%, Reuters reported.

Gold loans are growing fast, and lenders are using tighter valuation discipline and ticket-based LTV caps to control risk. For borrowers, the best deal starts with net weight, purity, and knowing how settlement timelines work in writing, while also benchmarking alternatives such as a personal loan, checking personal loan eligibility, and using a personal loan EMI estimate to compare monthly outgo before committing.

Related Financial News | |||