By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Insights

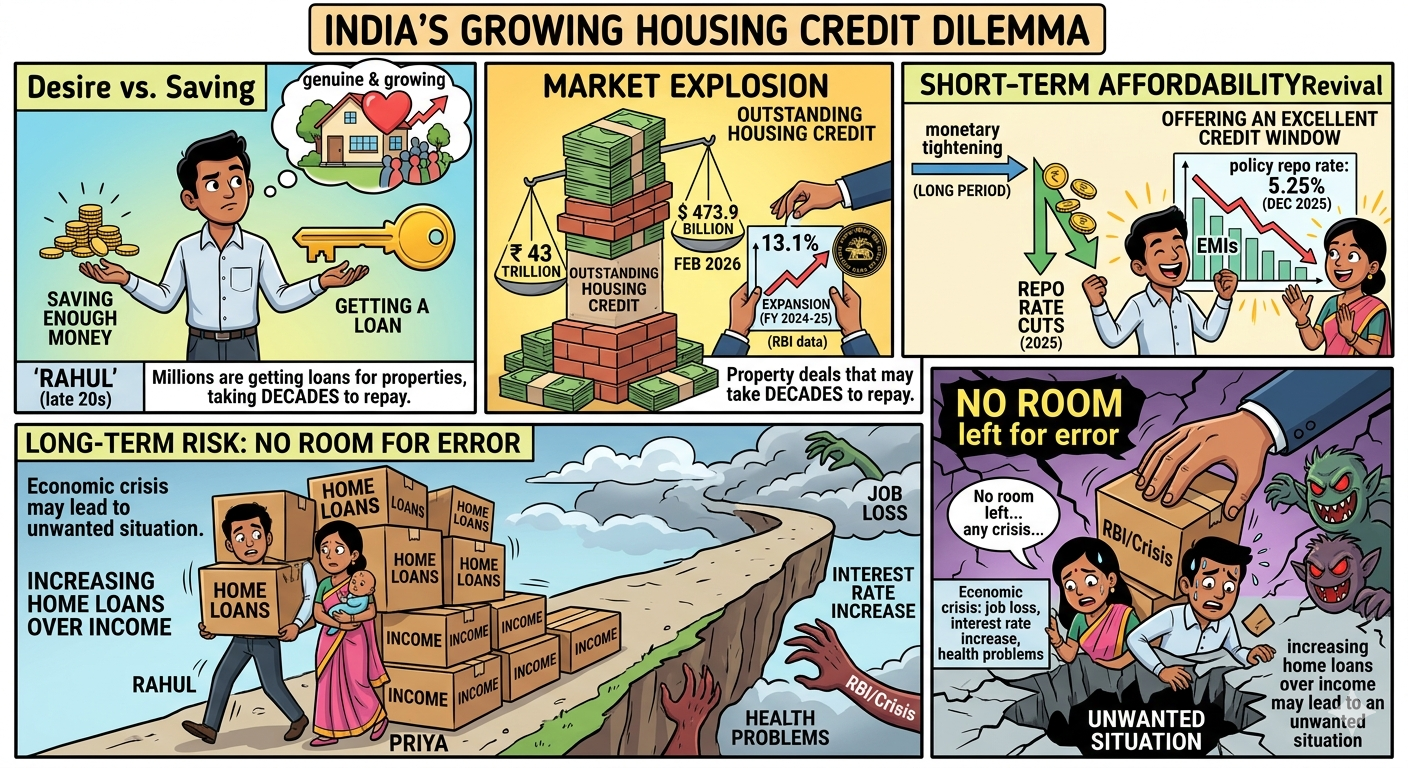

Borrowing is Becoming More Common to Buy Properties in India

Millions of Indians are getting loans for property deals that may take them many decades to repay.

Outstanding housing credit stood at Rs 43 trillion ($473.9 billion) in February 2026, having expanded by 13.1% during FY 2024-25, per RBI data.

There's no denying that the desire to own a house is genuine and growing.

But it's also becoming increasingly common as a means of securing a loan rather than saving enough money. business-standard

Affordability has increased in the short term due to falling interest rates.

Interest rate cuts during 2025 helped revive EMIs' affordability because the policy repo rate came down to 5.25% by December 2025.

Offering an excellent credit window after a long period of monetary tightening, as reported by the Reserve Bank of India.

But the long-term outlook is less favourable.

There is no room left for any error, as any economic crisis, be it job loss, interest rate increase, or health problems, may lead to an unwanted situation with increasing home loans over income.

Understanding the scale of India's housing credit surge requires a close look at the data below.

India's aggregate per capita debt for individual borrowers rose significantly, from ₹3.9 lakh in March 2023 to ₹4.8 lakh by March 2025, marking 10.8% year-on-year growth, according to HDFC TRU research.

That is a fast accumulation. For many households, a growing portion of monthly income now goes directly toward loan repayment rather than savings.

To India's middle class, a house means much more than mere assets; it represents identity, security, and aspirations.

Mumbai's EMI-to-income ratio fell below 50%, signifying sustainable home affordability, backed by the reduction of the policy repo rate by 125 basis points since February 2025, as per housing market experts.

This is indeed good news for all those who were unable to afford homes for several years. business-standard

There has been a trend of borrower accounts where Loan-to-Value ratios are above 70%, which suggests that homebuyers have been making smaller down payments on properties, implying that their loans are much larger compared to the property value.

Rate cuts have provided a small window of opportunity to first-time buyers in Pune, Hyderabad, and Bengaluru, among others.

But this is predicated on the assumption that their incomes remain stable. business-standard

The RBI is not oblivious to the household debt accumulation that the country is witnessing.

India's household debt boom, led by loans for consumption purposes to gratify immediate desires and not investments in productive assets, requires close monitoring, especially among low-rated households, according to HDFC TRU research analysts.

*T&C Apply

While the latter is considered relatively safer, the trend is what counts. business-standard

The home loan market was dominated by public sector banks at 47.33% in 2025, owing to quick rate transmission, while non-banking financial companies have grown faster by providing loans for self-employed individuals whose incomes tend to be volatile, according to HDFC's research.

Maintaining discipline in underwriting loans will prove crucial going ahead. Providing loans to households with limited ability to repay leads to vulnerability once unfavourable conditions strike.

There is no doubt that India's housing credit boom reflects the reality of consumer demand and affordability. However, the danger lies in consumers borrowing beyond their capability, which could end up leaving them heavily indebted.

Is the “Indian Dream” of owning a house still worth it?

Whether the “Indian Dream” of owning a home is still worth it depends heavily on your financial and life goals. Financially, renting and investing the difference in the stock market often yields higher net wealth.

Is buying a home with a bank loan a good decision or bad?

Buying a home with a bank loan is a highly subjective decision. It is generally good for building a physical asset and securing tax benefits, but can be bad if you overextend your finances or end up paying excessive long-term interest.

Related Financial News | |||