By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Why Thousands of Young Indians Are Choosing Rent Over a Home Loan and Getting Richer Faster?

Key Takeaways

Buying a home feels like an important life goal for many young professionals. But Nitin Kaushik recently shared a reality check on X (formerly Twitter). He said that a ₹40,000 EMI for 20 years does not just cost money, it also reduces your freedom.

Social pressure and higher lifestyle goals push many people to buy a home early. But taking a big loan at the start of your career can limit your choices. If you lose your job or need to move to another city, that home can quickly become a financial burden.

India’s urban middle class feels this dilemma the most. A ₹40,00,000 loan over 20 years means paying nearly ₹80,00,000 in total with average home loan interest rates at 8.5% to 9% annually. That is double the original amount.

Here is a simple comparison of what both paths look like:

This shows that the numbers favour investing, at least in the early years of a career.

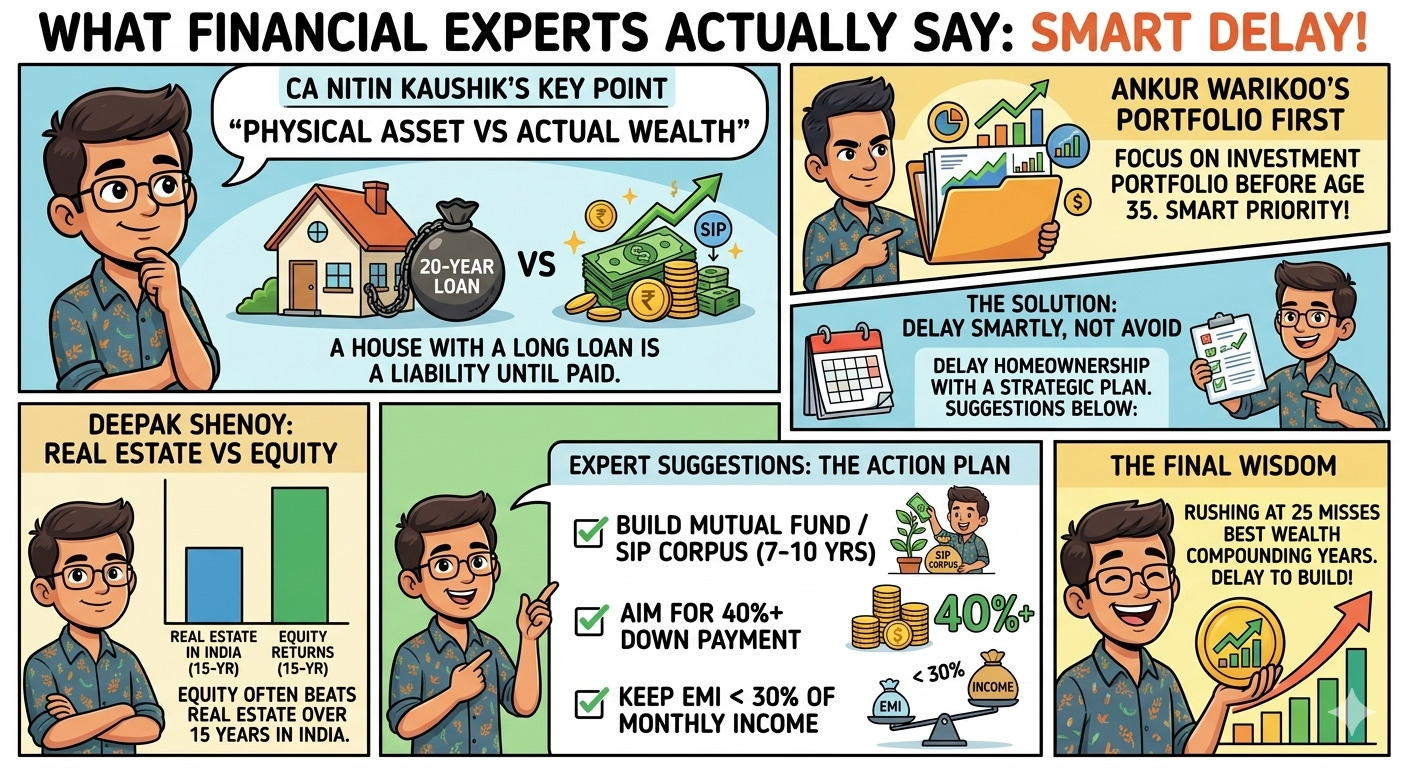

CA Nitin Kaushik put it simply, “You own the house, but it owns your cash flow.” He stressed that young professionals must not confuse a physical asset with actual wealth. A house tied to a 20-year loan is a liability until it is fully paid.

Personal finance expert Ankur Warikoo has also said in multiple public posts that buying a home before 35 is not always wise. He advises building a strong investment portfolio first.

SEBI-registered advisor Deepak Shenoy has similarly noted that real estate in India rarely beats equity returns over a 15-year horizon.

The solution is not to avoid homeownership forever. The advice is to delay it smartly. Experts suggest:

Rushing into a home loan at 25 may feel safe. But it often means missing the best years of wealth compounding.

The choice between a home EMI and investing is deeply personal. But the math speaks clearly. In early career years, staying liquid and investing consistently can help you buy a better home later, without financial stress. Let your money grow first. The house can wait.

1. Should I rent and invest in SIPs, or buy a home with a 20-year loan?

If you are early in your career, renting and investing are usually better. SIPs can grow your money, while EMIs lock your income. Buy a home only when your income is stable, and the EMI is easily manageable.

2. How do people decide between renting and taking a home loan?

People compare EMI vs rent, job stability, and plans. They also use EMI and SIP calculators to check costs and returns. If they want flexibility, they rent. If they want stability and can afford it, they buy.

Related Financial News | |||