By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

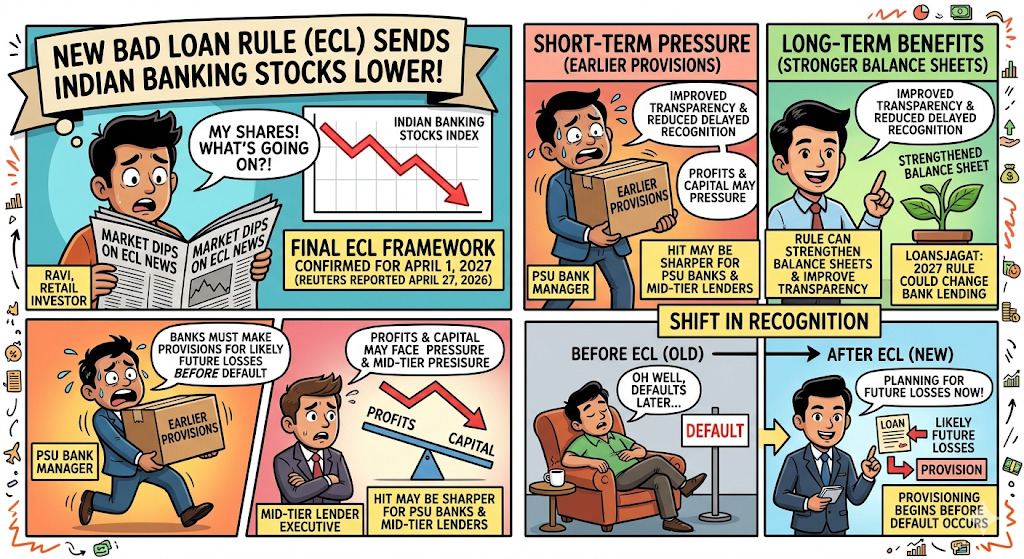

Bank shares fell after the new ECL provisioning rule raised fears of higher credit costs, lower profits and sharper pressure on PSU lenders.

Indian banking stocks slipped after the final Expected Credit Loss, or ECL, framework confirmed that banks will shift from recognising losses after default to providing for likely future losses. The framework will start from April 1, 2027, Reuters reported on April 27, 2026.

In the short term, banks may face pressure on profits and capital because provisions will have to be made earlier. The hit may be sharper for PSU banks and mid-tier lenders. In the long term, the rule can strengthen balance sheets, improve transparency and reduce delayed recognition of bad loans. LoansJagat also noted that the 2027 rule could change bank lending by forcing earlier recognition of weak loans.

Before the table, the market reaction showed a clear split. PSU banks saw heavier selling than private banks as investors focused on provisioning gaps and capital buffers.

After the table, the trend was simple. Investors sold lenders where the cost of early provisioning could eat into future earnings faster.

For Indian borrowers, the first visible change may come in loan approval filters. Banks may become more careful while lending in unsecured loans, vehicle loans, microfinance and other higher-risk segments, since future credit losses will now be counted earlier.

The positive side is for depositors and the financial system. If banks recognise stress earlier, weak loans are less likely to stay hidden for long. Fortune India reported that the new approach moves banks from an incurred-loss model to a forward-looking model based on a 3-stage, probability-weighted framework.

Before the second table, expert estimates show why bank stocks reacted quickly. The concern was not only about 1 year of provisioning, but also about recurring pressure on earnings.

After the table, the broad market view is that private banks with extra buffers may handle the shift better. PSU banks could need tighter capital planning before 2027.

Former SBI Chairman Dinesh Kumar Khara told Economic Times that Indian banks are ready for ECL norms. He said the industry’s capital adequacy is around 16-17%, while FY25 banking profit may be near Rs 4 trillion and FY26 profit may reach Rs 4.5-5 trillion.

The solution, according to market experts, is early capital planning, stronger buffers and cleaner loan monitoring before April 1, 2027. Punit Bahlani said the bigger issue may be the recurring hit to profitability, not just the one-time capital adjustment.

The ECL rule has hit bank stocks because investors expect higher provisions before 2027.

For the banking system, early loss recognition can reduce future bad-loan shocks, but PSU lenders may face a tougher adjustment.

Will RBI’s New Bad Loan Rule Make Indian Banks Safer Or Hurt Their Profits?

RBI’s new Expected Credit Loss rule will change how Indian banks handle bad loans. Instead of waiting for a loan to become overdue for 90 days, banks will have to estimate possible future losses and keep money aside earlier.

This may hurt bank profits in the short term, especially for PSU banks, because provisions could rise. Some banks may also become stricter while approving risky loans. But in the long term, this can make the banking system stronger, safer for depositors and more transparent for investors. It also brings India closer to global banking practices.

Why Do PSU Banks Struggle To Recover Large Bad Loans In India?

PSU banks often face slower recovery of huge loans because many large defaults involve long legal cases, stressed businesses, political pressure, weak collateral value and delays under recovery channels like IBC, DRT and SARFAESI. Earlier, some banks also gave big loans based on optimistic project reports without strong monitoring.

Once a company turns sick, recovering the full amount becomes difficult because assets lose value over time. However, the situation has improved after stricter RBI rules, better loan tracking, IBC cases and higher provisioning. PSU banks are now more careful, but legacy bad loans still affect recovery speed.

Related Finance News | |||

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

RBI Expands Agri Startup Financing Through Cooperative Banks |

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article