By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

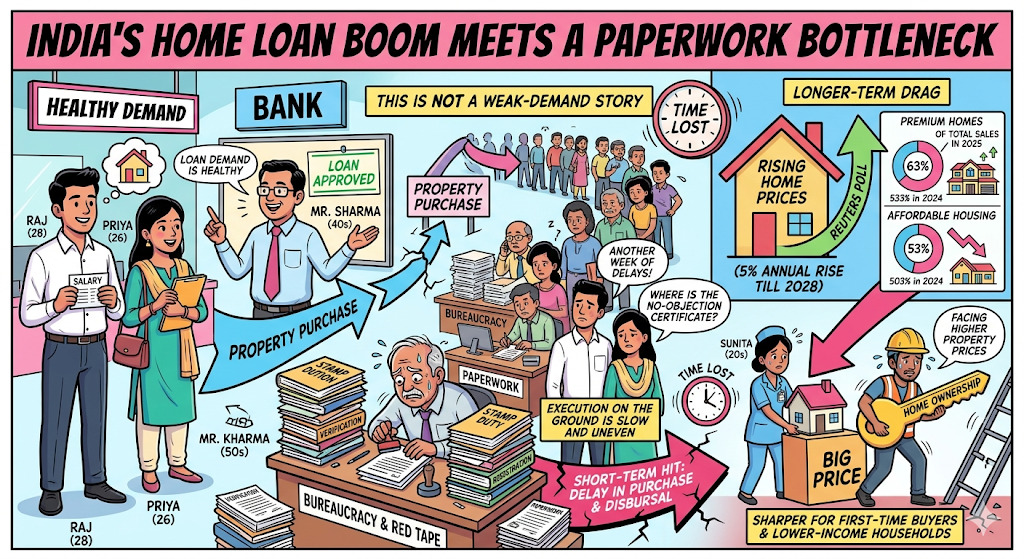

India’s home-loan market is expanding fast, but buyers are running into document-heavy processes, slow approvals and patchy lender practices just when housing costs are rising.

The short-term hit is delay in purchase and disbursal. The longer-term drag is sharper for first-time buyers and lower-income households already facing higher property prices. A Reuters poll published on 12 March 2026 said Indian home prices are expected to rise 5% annually through 2028, with premium homes making up 63% of total sales in 2025, up from 53% in 2024.

Before the numbers, one point stands out. This is not a weak-demand story. Loan demand is healthy, but execution on the ground is slow and uneven.

Those figures show where borrowers are getting stuck. Salaried applicants are usually asked for salary slips, Form 16 and bank statements. Self-employed applicants often need 3 years of ITRs and extra financial records, with property-title checks adding another layer.

For households in India, the problem is simple. Approvals take longer, document demands keep changing and closing a purchase becomes harder when prices are already moving up. That hurts buyers who need timing certainty and cannot keep stretching budgets.

There is still one positive angle. If lenders move to cleaner digital verification, the same market could become faster and cheaper for borrowers. LoansJagat reported on 22 January 2026 that a proposed housing credit passport could cut approval timelines from around 15 to 25 days.

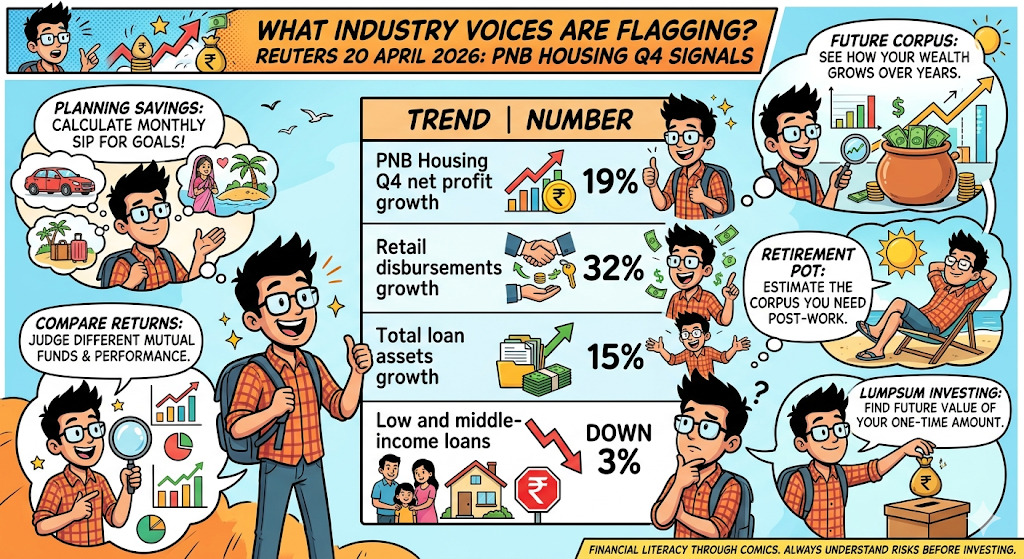

The bigger market signals are strong. Reuters reported on 20 April 2026 that PNB Housing Finance posted a 19% rise in Q4 net profit to ₹6.56 billion, with retail disbursements up 32% to ₹90.20 billion and total loan assets up 15.3% to ₹873.47 billion. But loans to low and middle-income households fell 3%.

Mint quoted BASIC Home Loan co-founder Atul Monga saying unclear requirements and repeated submissions remain common hurdles. BankBazaar’s Adhil Shetty told Mint lenders focus on identity, income and clean legal title. The likely fix is standardised checklists and consent-based digital data sharing.

India’s home-loan story is still growing, but the paperwork load is slowing buyers at the wrong time. Faster digital checks and standard document rules could ease the pressure.

What Papers Should A Buyer Keep Ready Before Applying For A Home Loan In India?

For a home loan in India, banks usually ask for KYC documents, income proof and property papers. A buyer should keep PAN, Aadhaar, passport-size photos, salary slips, Form 16 and 6 months’ bank statements ready. Self-employed applicants may also need ITRs, profit and loss statements and business proof.

*T&C Apply

On the property side, lenders usually check the sale agreement, title deed, allotment letter, tax receipts and approved building plan. Requirements can change from bank to bank, so it is smart to compare lenders first. Keeping both personal and property documents ready early can speed up approval.

How Can You Get a Home Loan With Minimal Documents in India?

A home loan without any paperwork is usually not possible in India. Lenders still need basic KYC, income proof and property papers before approval. What borrowers can do is reduce physical paperwork by using digital KYC, Aadhaar-based verification, DigiLocker documents and consent-based financial data sharing where available.

DigiLocker is designed to support paperless document access and verification, while some lenders already offer digital home-loan journeys. Experts have also proposed a housing credit passport to cut repeated document checks and speed up approvals. So, the practical answer is not zero paperwork, but less paperwork and faster processing.

Related Financial News | |||