Can Home Loan Money Be Used For Something Else In India?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

In India, regular home loans stay tied to housing use. Extra cash usually comes through top-up loans or loan against property, with lender rules and tax limits.

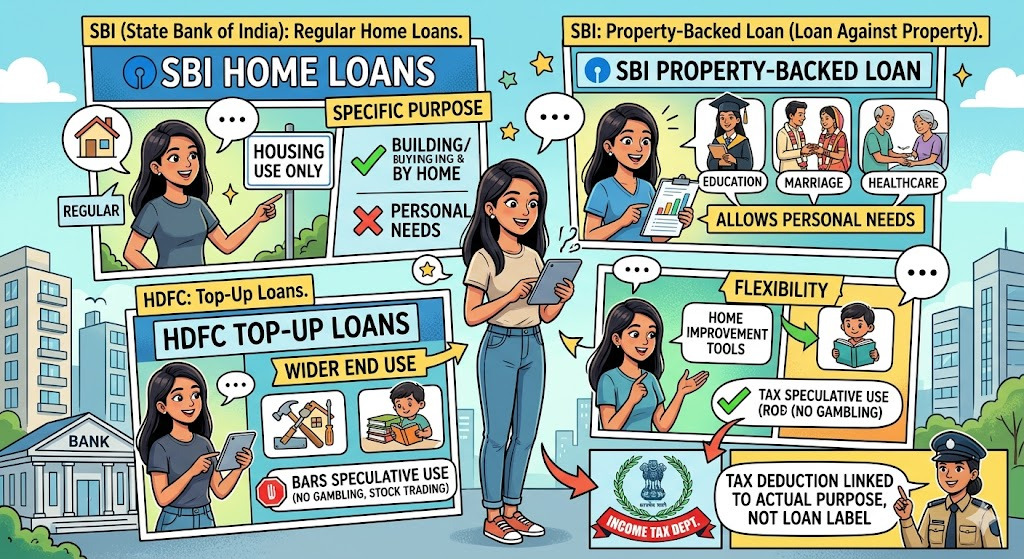

Indian borrowers often assume a home loan works like a cash-out mortgage in the US. It does not. SBI’s regular home loan page says the product is for purchase, construction, plot plus construction, extension and repair or renovation, and notes it has already served over 31 lakh families.

HDFC’s top-up loan page, meanwhile, separately positions extra borrowing for personal or professional needs other than speculative purposes. The split is simple: the original home loan is for the house, while extra liquidity usually comes from a top-up loan or loan against property.

What Homeowners Can Actually Use It For?

8 India-relevant reasons to tap home equity should be:

- Home Renovation And Repairs

Regular home loans in India can be used for repair and renovation, and SBI explicitly lists repair/renovation among approved uses.

- Home Extension Or Improvement

SBI also lists extension of house as an eligible purpose under its home loan products.

- Child’s Education

SBI’s loan against property page and HDFC’s top-up loan page both mention education as a valid use case.

- Marriage Expenses

Both SBI and HDFC list marriage-related expenses as an accepted end use for property-backed borrowing or top-up loans.

- Medical Or Healthcare Costs

SBI’s loan against property page specifically mentions healthcare expenditure.

- Debt Consolidation

HDFC says top-up loans can be used for debt consolidation, which makes this one of the clearest non-housing use cases in India.

- Business Expansion Or Professional Needs

HDFC allows top-up loans for personal and professional needs, including business expansion, though SBI’s LAP page says its LAP is not permitted for business purposes. So this one is lender-specific.

- Emergency Liquidity Or Large Planned Spending

Loans against property are positioned by SBI as an “all purpose loan” for major life expenses, while LoansJagat also frames property-backed borrowing as a way to unlock funds using owned property.

That also explains why borrowers use these products for planned expenses and not just emergencies.

Tax treatment stays narrower than borrowing flexibility. The Income Tax Department page updated on 11 December 2025 says Section 24(b) allows up to ₹2,00,000 on self-occupied property for purchase or construction, but only ₹30,000 for repairs.

How This Shift Built Up In India?

Over time, the market separated housing finance from property-backed liquidity. SBI’s product pages draw that line clearly. A regular home loan is attached to the property transaction itself, while a loan against property sits under personal-purpose borrowing.

LoansJagat’s explainer published on 16 September 2025 also notes that home equity in India is generally accessed by borrowing against the value built in the property, not by freely repurposing the original home loan. Mint, in its 24 September 2025 report, reminded borrowers that pledging a home for credit carries repayment risk because the home remains collateral.

This difference shapes how lenders assess use, how tax deduction works, and how much flexibility a borrower really has.

Borrowers looking for education, medical or marriage funding are usually entering the home-equity route, not the plain home-loan route.

What Banks And Tax Authorities Are Saying?

SBI is clear that regular home loans are for housing use, while its property-backed loan allows personal needs such as education, marriage and healthcare.

HDFC allows wider end use through top-up loans but bars speculative use. The Income Tax Department links deduction to actual purpose, not just the loan label.

Conclusion

In India, home-loan money is not open-ended cash. Borrowers usually need a top-up loan or loan against property for other expenses, and the tax benefit stays tied to actual end use.

Related Financial News | |||

|

|

| |

| |||

|

| ||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article