RBI Mis-Selling Rules: How New Draft Curbs Could Make Banks Pay For Wrong Sales

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

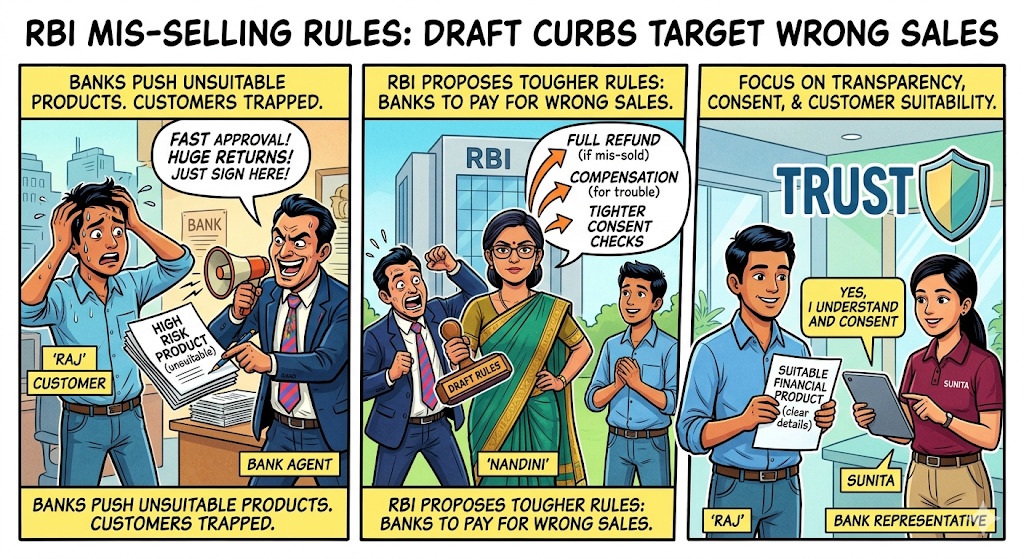

India’s banking sales model is under pressure after draft rules proposed full refunds, compensation and tighter consent checks when customers are pushed unsuitable financial products.

Mis-selling has returned to the spotlight after banks were accused of pushing insurance, investment and add-on products to customers seeking basic loans or deposits. The trigger was a fresh draft framework released on 11 February 2026, followed by Finance Minister Nirmala Sitharaman’s warning on 23 February 2026 that banks should stop mis-selling and focus on core business.

Reports in Mint, Reuters and The Economic Times say the proposed rules could start from 1 July 2026, with public comments invited till 4 March 2026.

Before the tougher provisions are explained, the immediate takeaway is simple. The draft shifts accountability to banks, not just to customer signatures or fine print.

How Customers Stand To Gain?

The main change is sharper customer protection. If mis-selling is established, banks may have to refund 100% of the amount paid, cancel the sale where needed, and compensate for losses.

The draft also targets forced bundling, dark patterns on apps and websites, and sales of products that do not match a customer’s age, income, education or risk profile, even when consent was taken.

That means a signed form may no longer be enough defence for a bad sale. India Today reported this full-refund clause on 12 February 2026, while LoansJagat and The Economic Times highlighted the same safeguard on 16 February 2026 and 28 February 2026 coverage.

Another important shift is the consent design. Reports say banks would need separate and explicit customer approval for each product, making it harder to slip in insurance, cards or paid add-ons through bundled sales.

What Happened Before This Crackdown?

The build-up began at the MPC outcome on 6 February 2026, when the central bank flagged draft measures on mis-selling and loan recovery practices. Within days, the draft sales-practice rules were published. By 16 February 2026, explainers across The Economic Times and LoansJagat had started unpacking the likely impact on bank branches, DSAs and digital channels.

The issue gained wider public traction after Sitharaman’s remarks on 23 February 2026. The Economic Times and Times of India reported that she described mis-selling as an offence and asked lenders to stop selling products that customers do not need.

Around the same time, Forbes India reported on 24 February 2026 that over half of online users said they had faced hidden charges, forced add-ons or deceptive design on banking websites. That gave the debate a digital angle beyond branch sales.

These developments show why the draft is being seen as a bigger consumer-rights shift, not just another compliance update.

What Stakeholders Are Saying?

Sitharaman’s stand has been blunt: banks should return to deposit-taking and lending, not push products customers did not ask for.

Industry commentary in Reuters, ET and TOI suggests the draft could force banks to rethink incentive-driven selling and digital nudges.

Conclusion

If finalised in the present shape, the rules could make mis-selling expensive for banks and easier to challenge for customers. The big shift is clear: wrong sales may now come with a direct refund bill.

Related Financial News | |||

|

|

| |

| |||

|

| ||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article