Gold, Stocks Or Debt? Top Multi-Asset Funds Split Their 2026 Bets

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Multi-asset funds are drawing fresh investor money, but fund managers are now divided between equity-heavy portfolios, gold trimming and debt cushions.

Key Takeaways

- Multi-asset fund assets rose to ₹1.87 lakh crore from ₹1.13 lakh crore in 1 year, while 1-year returns ranged from 3.3% to 24.6%.

- Earlier, gold and silver rallies helped the category, but latest updates show some funds cutting precious metal exposure.

What Is Pushing Investors Towards Multi-Asset Funds?

Multi-asset allocation funds are gaining attention as investors look for one scheme that can invest across equity, debt, gold, silver, REITs and InvITs. As per The Economic Times report published in May 2026, the category’s assets climbed to ₹1.87 lakh crore from ₹1.13 lakh crore in 1 year.

The short-term benefit is lower dependence on one asset class. The long-term risk is that a wrong call by the fund manager can reduce returns. The same ET report said 1-year returns across multi-asset funds ranged from 3.3% to 24.6%, showing a wide gap between winners and laggards.

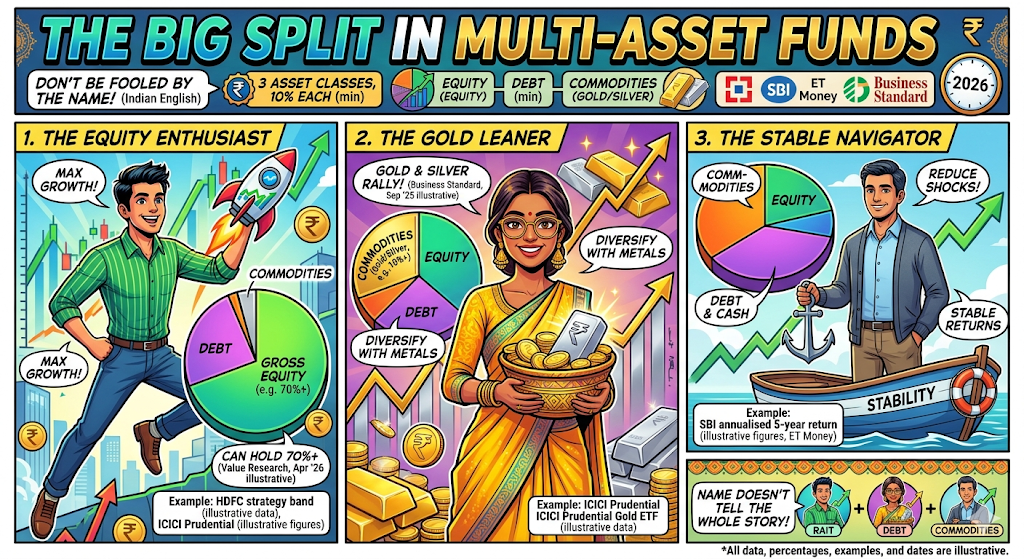

The Big Split In Multi-Asset Fund Portfolios

Multi-asset funds need at least 10% allocation in 3 asset classes. Value Research, in an article dated 20 April 2026, said these funds can still hold from 10% to over 70% in gross equity, depending on the scheme.

This shows why investors cannot judge these schemes only by category name. One fund may run like an equity-heavy hybrid fund, another may lean towards gold, while a third may use debt and cash to reduce portfolio shocks.

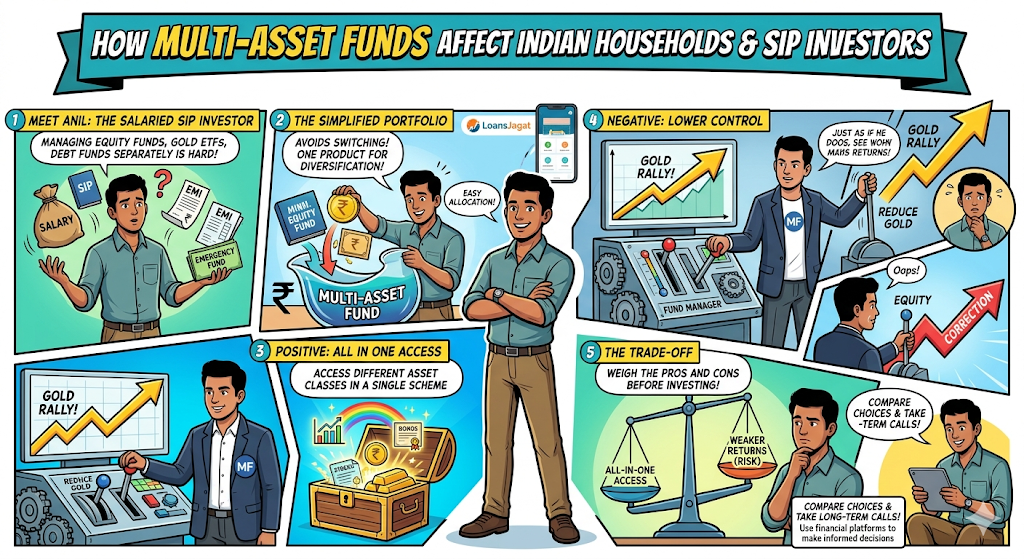

How This Hits Indian Households And SIP Investors?

For Indian households, this trend changes how portfolio building is done. A salaried investor with SIPs, EMIs and emergency savings may use multi-asset funds to avoid switching between gold ETFs, equity funds and debt funds separately. Personal finance platforms such as LoansJagat also focus on helping borrowers and investors compare financial choices before taking long-term calls.

The positive side is access to different assets in one product. The negative side is lower control. If a fund manager reduces gold just before another rally, or raises equity before a correction, investors may face weaker returns despite owning a diversified scheme.

What Experts Are Saying, And What Investors Can Do?

Ihab Dalwai of ICICI Prudential AMC said in The Economic Times interview dated May 2026 that investors should not depend on one static asset class when markets are expensive. He favoured flexible allocation across equity, debt and commodities.

Aparna Karnik of DSP Mutual Fund said in The Economic Times interview published in February 2026 that the fund keeps equity closer to 50% when valuations are stretched and can move it towards 70% when risk-reward improves.

The solution for investors is to check the latest portfolio before investing. They should compare equity level, gold and silver exposure, debt quality, expense ratio and past drawdowns, not only 1-year return.

Conclusion

Gold, equity and debt are all being used differently by top fund managers in 2026. The real test for investors is choosing a fund whose asset mix matches their risk profile.

FAQs

Is adding gold to an equity and debt portfolio a good idea for Indian investors?

Gold can be added, but don’t put too much money into it. For many investors, around 5% to 10% is enough. It can help when equity markets fall or when there is global uncertainty. Gold ETFs are easier to buy and sell, so they suit people who want quick access.

Sovereign Gold Bonds can be better for long holding periods because of tax benefits, but selling early may not be easy. Debt and equity should still do the main job in the portfolio. Gold should be used only as a small safety layer, not as the biggest investment.

What is the best gold option for someone planning to invest?

If the purpose is investment, gold jewellery is usually not the first choice. Making charges and wastage reduce the resale value. Gold ETFs work well for people who already have a demat account. Gold mutual funds are simpler for beginners because they can be bought like any other mutual fund.

Sovereign Gold Bonds are useful for long-term investors, as they give gold price returns along with fixed interest. Coins and bars are fine only when purity, bill and safe storage are checked. For most people, paper gold is easier to buy, track and sell later.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article