Are Home Loan and Personal Loan Borrowers Ready for 2026 Hikes?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

SBI Chairman C. S. Setty has backed a rate pause, saying India’s long growth run depends on credit, jobs, digital payments and infrastructure.

Key Takeaways

- SBI Chairman C S Setty said a rate pause can help India protect growth and avoid sudden loan-cost pressure.

- Earlier, rates were held at 5.25%, and LoansJagat noted, that home loan EMIs stayed stable.

India’s largest bank chief has supported a pause in interest rates just before the June policy decision. C S Setty said a pause would help growth move without sudden pressure on borrowers, banks and companies, as reported by The Economic Times.

In the short term, borrowers may avoid fresh EMI pressure. In the long term, the bigger point is that the situation is different. Setty said India’s growth story cannot be read only through Sensex moves, as Business Standard reported.

India’s Growth Story In Numbers

Setty pointed to digital payments, banking access and long-term investment needs. These are not daily stock market signals. They show how money now moves through ordinary homes, kirana shops, small firms and government benefit systems.

That is why his “beyond Sensex” remark lands well. A farmer receiving DBT, a student paying through UPI, or a small trader getting formal credit is also part of the growth story.

What This Means For India’s Borrowers And Families

For home loan borrowers, a pause usually means no fresh shock in floating EMIs. It may not bring instant relief, but it gives people room to plan monthly budgets. Small firms also get a better grip on working capital costs.

There is a downside too. If rates stay unchanged for too long, borrowers waiting for cheaper loans may have to wait more. Savers may also watch deposit rates closely, especially retired people who depend on interest income.

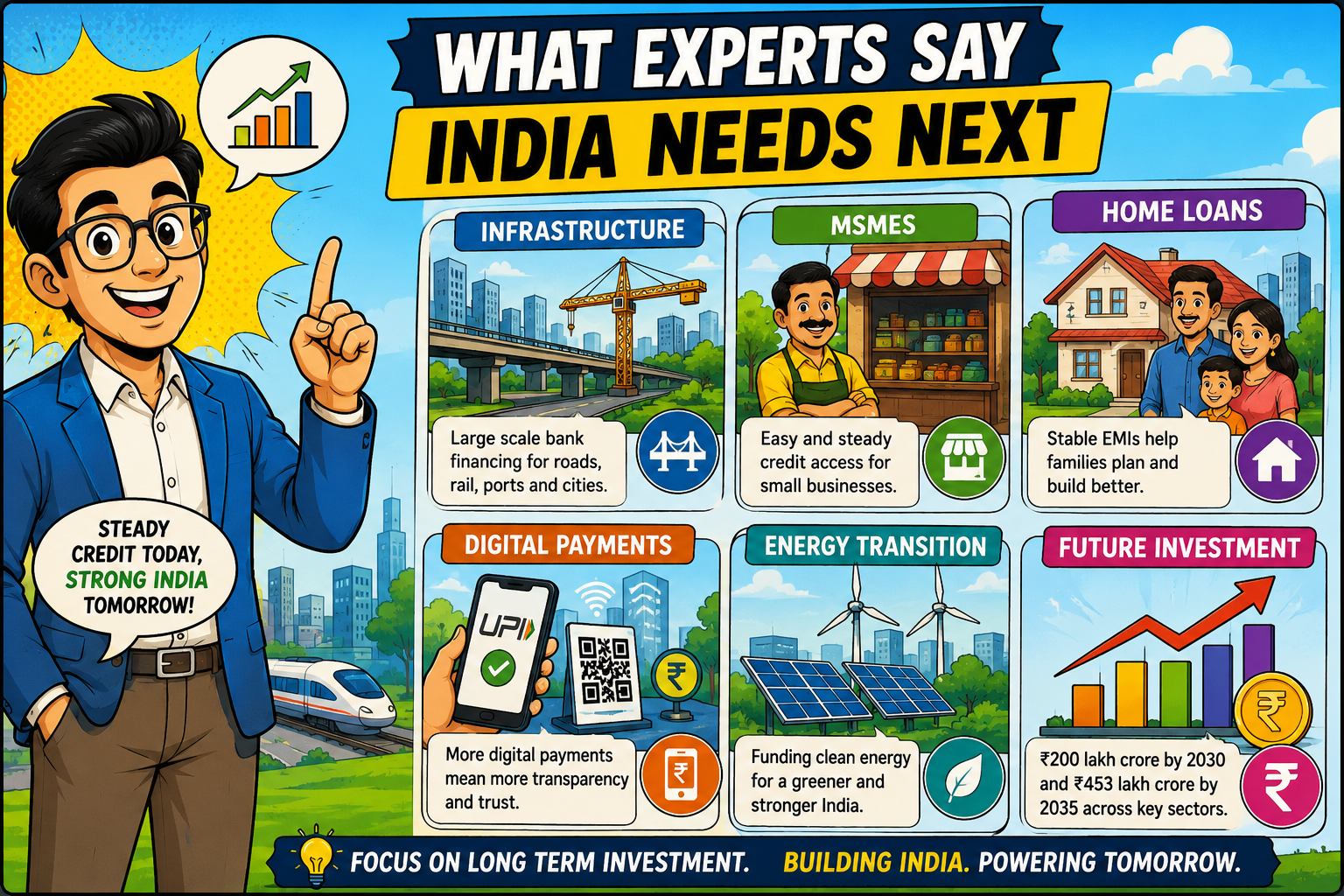

What Experts Say India Needs Next

Setty said India may need nearly ₹200 trillion in fresh investment by 2030 and another ₹453 trillion by 2035 across infrastructure, manufacturing, energy transition, urban development, MSMEs and innovation, according to The Economic Times.

The solution, in his view, is not only cheaper money. Banks need to finance productive sectors, widen market access, support entrepreneurs and use technology better. That is where India’s banking system will be tested.

Conclusion

Setty’s message was simple: the stock market is only one window into India’s economy. Rates, credit, digital payments and bank-led investment may decide how widely growth reaches Indian households.

FAQs

Successive increase in home loan interest rates: EMI hike vs. tenure hike?

When home loan interest rates rise repeatedly, lenders usually adjust repayments in one of two ways: increasing the EMI or extending the loan tenure. An EMI hike means borrowers pay more every month but can finish the loan within the original schedule. A tenure hike keeps the EMI largely unchanged but increases the repayment period, leading to higher total interest costs over time. Most banks initially prefer extending tenure to reduce the immediate burden on borrowers. However, if rates continue rising and the tenure reaches its limit, EMIs may also increase. Borrowers should review loan terms regularly and consider prepayments when possible.

Should I buy a house now or wait, given home loan interest rates in India in May 2026?

Whether you should buy a house now or wait depends more on your finances than on predicting interest rates. As of May 2026, borrowing costs have eased from recent highs, but future rate movements remain uncertain. If you have a stable income, a sufficient down payment, and plan to stay in the property for several years, buying now may make sense, especially if you find a home that fits your budget. Waiting could help if rates fall further, but property prices may also rise. Instead of trying to time the market perfectly, focus on affordability, EMI comfort, and long-term financial goals.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article