Most FD Investors Get This Wrong: One ₹5 Lakh FD or Five ₹1 Lakh FDs?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- 5 FDs of ₹1 lakh each deliver comparable returns compared to one FD, with the former providing better liquidity.

- As far as the security of your investment is concerned, DICGC insurance provides cover to the extent of ₹5 lakh per bank. So investing in five FDs in different banks will lower the risks for investors.

One FD Or Five: What Should Your ₹5 Lakh Do In Five Years

A ₹5 lakh fixed deposit might appear quite straightforward. However, the way you structure your FD can affect more than just returns, especially when you need quick access to your money during an emergency.

In the case of a five-year investment tenure, the choice of splitting FDs versus a lump sum FD depends on many factors.

On the bright side, your returns remain almost the same regardless of the FD structure. At an annual interest rate of 7% and quarterly compounding, your FD will generate ₹7,07,389 after five years if you park your lump sum of ₹5 lakh in it.

Your earnings will come out to ₹7,07,390 by splitting this money equally into five FDs of ₹1 lakh each. As you can see, the difference is insignificant.

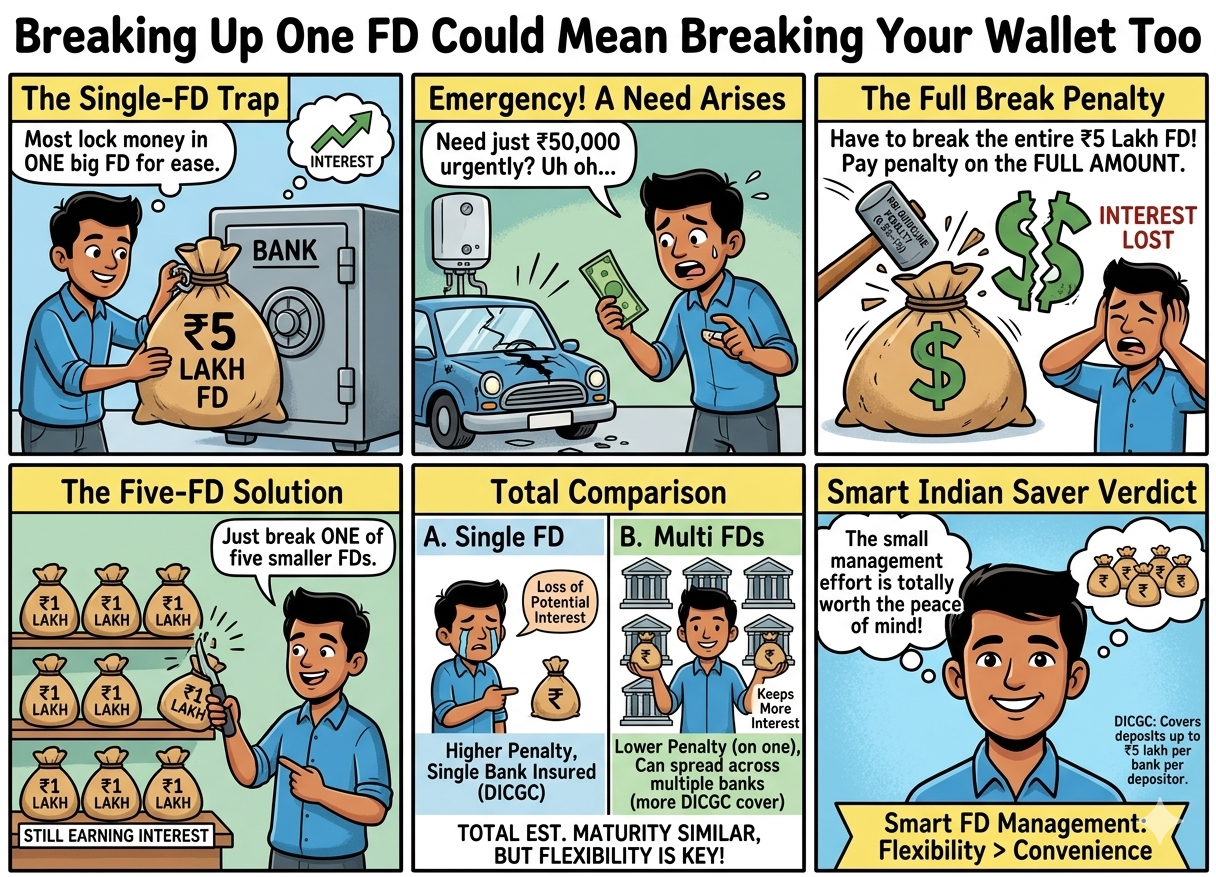

Breaking Up One FD Could Mean Breaking Your Wallet Too

Here is where most investors get it wrong. If you lock ₹5 lakh in a single FD and face an emergency, you may have to break the entire deposit. Most banks charge a premature withdrawal penalty of 0.50% to 1%, as per RBI guidelines. That means losing interest on the full amount, not just what you need.

With five separate FDs, you break only one and keep the rest earning interest. This table shows how the two options compare:

Additionally, DICGC insures deposits up to ₹5 lakh per depositor per bank. The spreading of FDs across different banks adds a layer of safety.

What Financial Experts Recommend for Smarter FD Planning?

Adhil Shetty, CEO of BankBazaar, has noted that FD laddering reduces the risk of reinvesting the entire corpus at lower interest rates and offers a balance between short-term and long-term rates.

He also points out that public sector banks generally impose lower premature withdrawal penalties than private sector banks, which makes them a safer choice if liquidity is a concern.

One FD still works well for investors who prefer simplicity. It is easier to track a single maturity date and manage one renewal. It suits retirees or those who do not need frequent liquidity.

Conclusion

The returns from one FD and five FDs are almost identical over five years. But five smaller FDs give you more control, better emergency access, and lower penalty risk. As you are investing ₹5 Lakh for 5 years, breaking it down into various parts makes a more practical investment for many investors. Pick a structure according to your liquidity requirements, not just the rate of interest.

FAQs

Should I spread my 5 lakhs across five FDs instead of having it in a single one?

If you think there is a possibility of needing money in between, then keeping five FDs might be a good idea. There is little difference in returns, and in case of an emergency, you will only need to break one FD instead of withdrawing the entire amount and paying a penalty for all five.

Are there any disadvantages of having multiple FDs with multiple banks?

The primary drawback is having to remember the various maturity dates, interest payouts, and renewal due dates. Nonetheless, keeping FDs in separate banks will provide better security of deposits and will allow you to meet your various objectives, like emergencies and retirement goals.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article