Inflation Shock Is Back, But US And India May Not Raise Rates Together

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Inflation is rising in both economies, but the US and India may still follow different interest rate paths due to different price pressures.

Key Takeaways

- US inflation rose faster in April 2026, with CPI and PCE both at 3.8%, raising pressure on the Federal Reserve.

- India’s April CPI was lower at 3.48%, while earlier updates flagged oil, rupee and food risks as the next triggers.

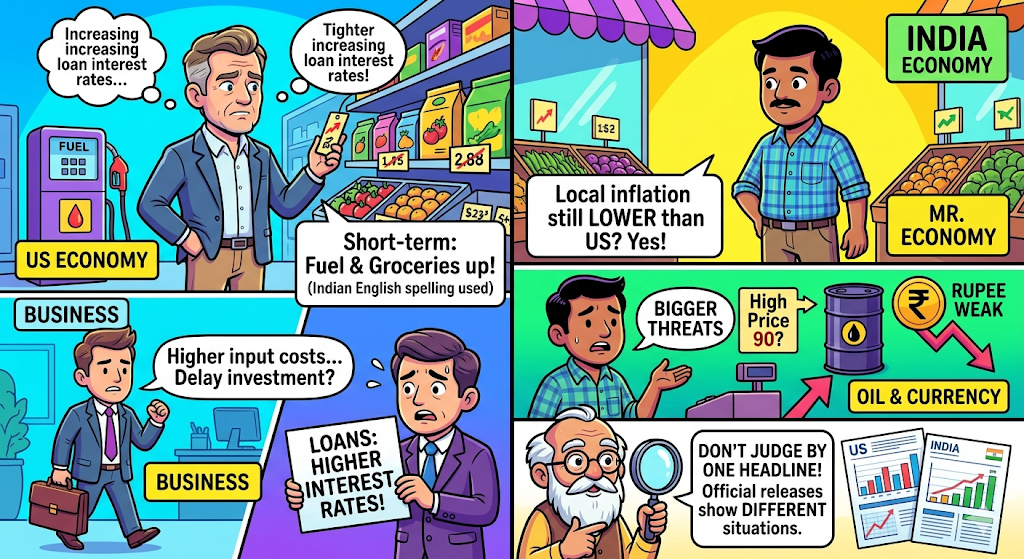

Inflation Is Rising Again, But Not In The Same Way

Prices are moving up again in the US and India. For families, the short-term pain may come through fuel, groceries and loan costs. For businesses, higher inflation can raise input costs and delay investment decisions.

In the long term, the risk is bigger for borrowers if central banks choose tighter rates. But India’s case looks different from the US because local inflation is still lower, while external pressure from oil and currency movements remains the bigger threat.

The latest official releases show why both economies cannot be judged by one inflation headline.

This gap is important. The US is facing inflation above its 2% target. India’s inflation is below the 4% target, though food prices, crude oil and rupee weakness can change the picture quickly.

Why Indian Borrowers And Consumers Should Watch This Closely?

For Indian households, the biggest pain point may not be only EMI. A weak rupee can make imported crude costlier, which then flows into petrol, diesel, transport and food prices. That can hit monthly budgets even without a rate hike.

There is also a positive side. If Indian rate-setters avoid an immediate hike, home loan and personal loan borrowers may get more time before EMIs rise. LoansJagat reported on 14 May 2026 that the repo rate was expected to stay at 5.25%, while oil and rupee pressure remained the risk.

The market view also shows a split between inflation fear and growth protection.

A rate hike can support the rupee, but it cannot produce cheaper crude oil or better food supply. That is why India may prefer targeted currency steps and liquidity action before raising rates sharply.

What Experts Say And What Can Be Done Next?

The Federal Reserve’s 18 March 2026 projections showed 2026 PCE inflation at 2.7% and core PCE at 2.7%. Its projected federal funds rate for end-2026 was 3.4%, showing a cautious path.

Experts quoted by Reuters said India may hold rates because inflation is still below target. The better solution may be to protect the rupee through market tools, monitor food supply and use rate hikes only if inflation becomes lasting.

Conclusion

The US may stay tougher on rates because inflation is broader and above target.

India may wait longer, unless oil, food prices and rupee pressure turn into a bigger price shock.

FAQs

Will a repo rate cut to 5.25% reduce loan EMIs in India?

It can, but borrowers may not see the benefit on the same day. If a home loan or personal loan is linked to an external benchmark, banks usually revise rates faster. Still, each bank follows its own reset date. So, some EMIs may fall after a few weeks or months.

Fixed-rate loan borrowers may not gain from this cut. FD investors should also watch this, because banks may reduce deposit rates later. For the economy, cheaper loans can help buyers, small businesses and real estate. But if inflation rises again, banks may become slow in passing the full benefit.

Can high US inflation increase costs for people in India?

Yes, it can affect India, though not directly every time. When prices rise in the US, the Federal Reserve may keep rates high for longer. That often supports the dollar. For India, a stronger dollar can push the rupee lower. Then crude oil, electronics, fertilisers and other imports become costlier. Fuel prices can slowly affect transport and daily goods too. Foreign investors may also pull some money from Indian markets if US returns look better. So, Indian families may feel it through petrol, imported items, market volatility and slower loan rate cuts.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article