RBI MPC April : Why Home Loan EMIs May Stay Flat For Now

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

With the April 8 policy verdict nearing, borrowers are looking for EMI relief. But a repo pause, slow loan resets and market stress could keep instalments unchanged.

Home loan borrowers are heading into the RBI Monetary Policy Committee meeting with limited hope of an immediate EMI cut.

A Reuters poll published on April 6 said 69 of 71 economists expect the repo rate to stay at 5.25%. That view has strengthened as crude oil, bond yields and the rupee have all turned volatile. In plain terms, lenders are unlikely to rush into passing on any benefit when the policy rate itself is expected to remain unchanged and market conditions are still tight.

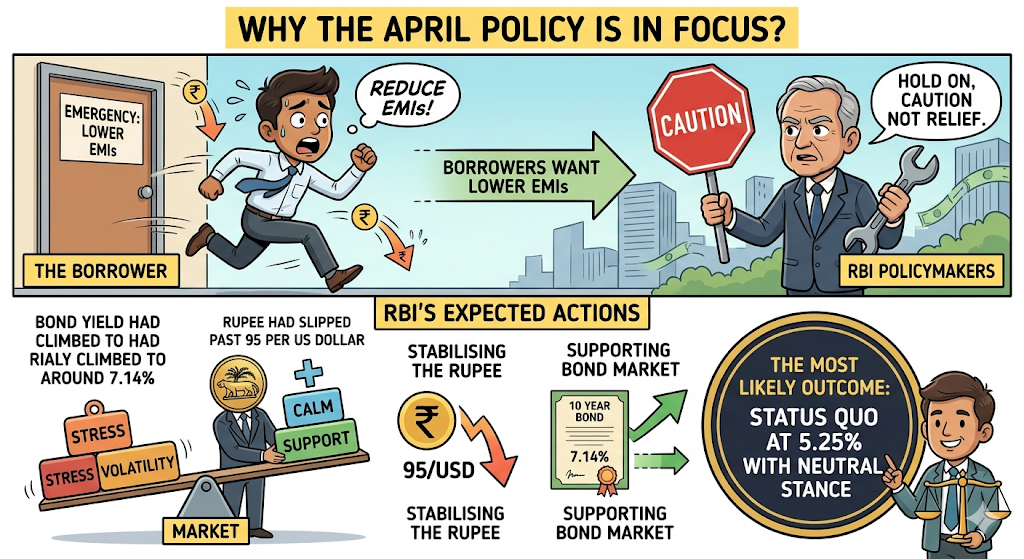

Why The April Policy Is In Focus?

The issue is simple. Borrowers want lower EMIs, but this policy may deliver caution, not relief. Reuters reported on April 6 that the RBI is expected to focus on calming financial markets, supporting liquidity and preventing further stress in the rupee and bond market.

The same report said the 10-year bond yield had climbed to around 7.14%, while the rupee had slipped past 95 per US dollar. Moneycontrol, in its April 3 preview, also said the most likely outcome was status quo at 5.25% with a neutral stance.

For borrowers, that usually means floating-rate home loans do not see any fresh downward revision right away. Banks first wait for the policy signal, then follow their reset cycle. If there is no cut, EMI movement usually stays stuck where it is.

Why EMIs May Not Move Right Away?

The bigger story is transmission. ETBFSI reported on January 29 that 46% of public sector banks’ outstanding floating-rate loans were still linked to MCLR, against 10% for private banks. MCLR-linked loans adjust slower than external benchmark-linked loans. So even when rates fall, many borrowers do not see the benefit quickly.

LoansJagat said on March 7 that on a ₹50 lakh home loan for 20 years, the EMI is about ₹44,986 at 9% and about ₹43,391 at 8.5%. That shows the saving can be visible, but only when the revised rate is actually passed on.

This is why many borrowers have not felt full relief even after earlier easing. Business Standard reported on April 5 that the RBI had already cut rates by 1.25% from last February, but kept them unchanged in August, October and February 2026.

What Economists And Banks Are Saying?

Reuters quoted HSBC’s Pranjul Bhandari saying that if the energy shock lingers, growth could take a hit bigger than the price shock. Barclays’ Aastha Gudwani told Reuters the RBI may keep injecting liquidity.

ET on April 6 said policymakers are likely to watch the rupee and bond yields closely rather than move rates quickly.

Conclusion

For now, the April MPC looks more like a pause-for-assessment than an EMI relief event. Home loan borrowers may have to wait for both a policy shift and faster bank transmission.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article