Retail Loan Write-Offs Spike In India: Should Depositors Be Worried?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

India’s banks are writing off more retail loans than before. That does not put deposits at immediate risk, but it shows stress in unsecured lending.

Indian banks wrote off ₹1.72 lakh crore of loans in FY2024-25, and for the first time retail loans topped all segments at ₹45,404 crore, according to Finance Ministry data reported by The Indian Express on 16 March 2026.

Services accounted for ₹38,438 crore, industry ₹37,716 crore, MSMEs ₹28,587 crore and agriculture ₹21,882 crore. The key question for depositors is simple: if a bank writes off many loans, is their money at risk? Not straightaway. A write-off is an accounting move to clean up bad assets from books. It is not the same as a loan waiver, and recovery efforts usually continue.

Why Retail Write-Offs Are The Real Story?

Read More - Retail Banking

The deposit angle needs context. A high write-off number does not mean depositors should panic, because banks make provisions and absorb these losses over time. The sharper issue is where the stress is building.

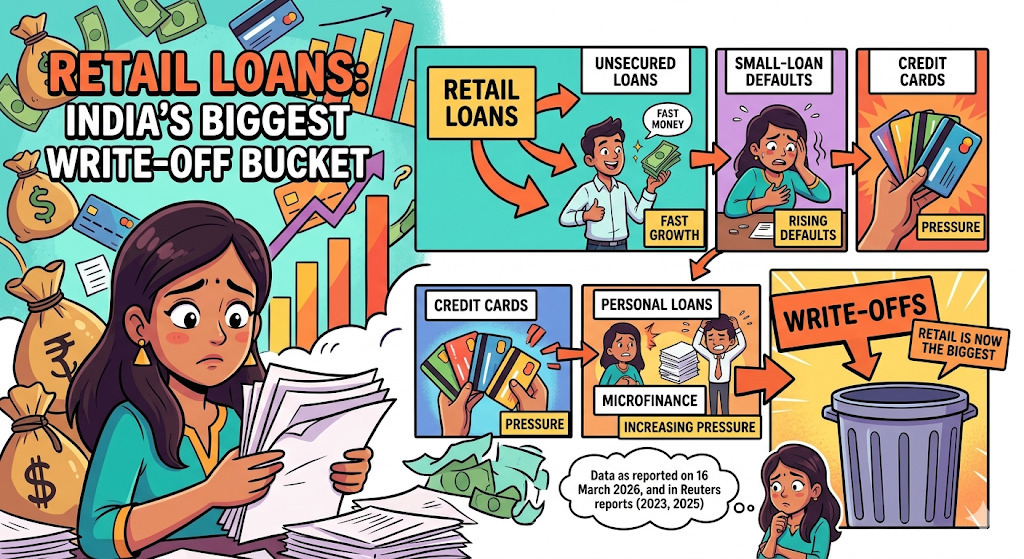

Recent pressure has shifted from large corporate loans to small-ticket unsecured retail credit, especially personal loans, credit cards and microfinance. That is why retail now leads write-offs.

The pattern suggests that banks expanded consumer credit fast, including among weaker borrower segments, and some of that lending is now going bad. A Reuters report published on 30 June 2025 said delinquencies had risen in these retail pockets and that non-housing retail loans formed 54.9% of total household debt.

How This Built Up Over Time?

In the run-up to this trend, unsecured retail credit had been growing at a sharp clip. Reuters on 16 November 2023reported that unsecured personal loans were up 23% year-on-year as of 22 September 2023, while outstanding credit card balances had risen nearly 30%. That pace of growth pointed to aggressive lending.

By 9 February 2025, Reuters reported that private banks were seeing higher defaults in micro loans, personal loans and credit cards, pushing lenders to slow fresh disbursals in those categories.

A background note from LoansJagat, published on 28 October 2025 also flagged unsecured, no-collateral lending as a growing problem for Indian banks because recovery is harder when borrowers default.

What Stakeholders Are Saying?

Also Read - PSU Banks Boost Retail Loans

The Finance Ministry’s data, as reported by The Indian Express on 16 March 2026, shows retail has become the biggest write-off bucket.

Reuters reports from 2023, 2025 and 2025 point to the same trend: fast growth in unsecured loans, rising small-loan defaults, and pressure in cards, personal loans and microfinance.

Conclusion

Deposits are not automatically in danger because a bank writes off loans. But rising retail write-offs show that easy unsecured lending is now feeding visible credit stress.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article