What Happens To Unpaid Credit Card Debt If You Move Abroad?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

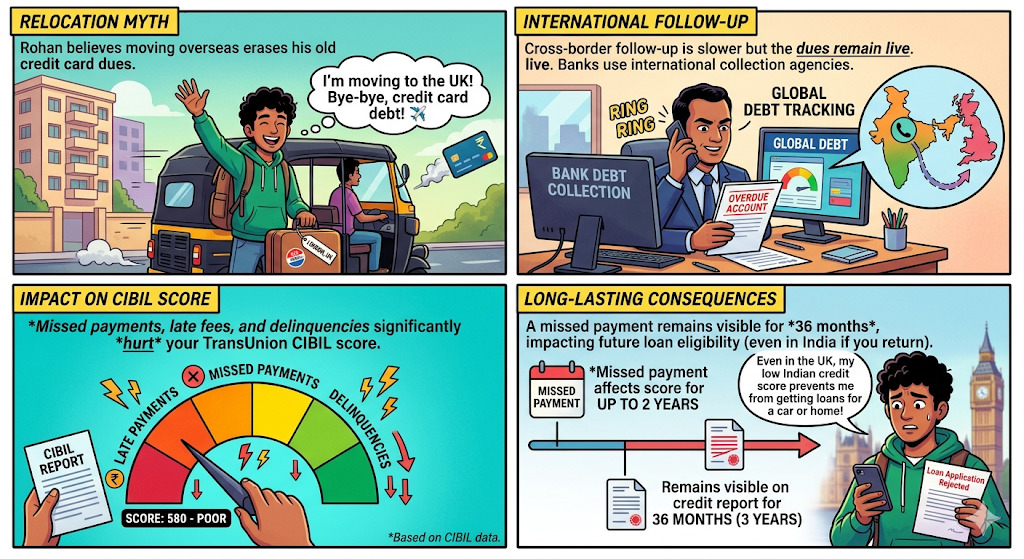

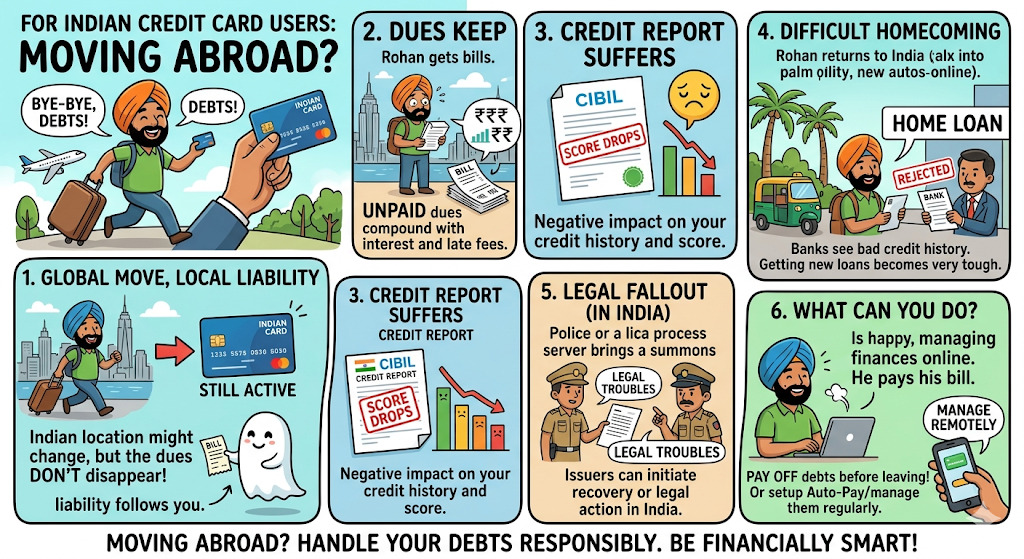

For Indian credit card users, shifting abroad does not close unpaid dues. The bill can rise, the CIBIL score can fall, and lenders can still chase recovery.

An unpaid Indian credit card bill does not disappear when the cardholder leaves the country. Banks can continue charging interest and late fees as per the card agreement, while the default can stay visible in India’s credit ecosystem.

That creates a longer tail for borrowers who later want a home loan, personal loan, car loan or even a fresh credit card in India. For NRIs and emigrants, the real issue is not only recovery calls. It is also future borrowing power, linked bank relationships and the cost of leaving a small unpaid balance unattended.

Why Moving Overseas Does Not Close The Credit Card Bill?

Indian cardholders often assume recovery becomes weak once they relocate. That is only partly true. Cross-border follow-up can be slower, but the dues remain live. TransUnion CIBIL says late payments, missed payments and delinquencies may hurt the score. In its article Does A Failed Credit Card Payment Pull Down Your Score?, CIBIL says a missed payment can affect the score for up to 2 years and remain visible on the credit report for 36 months.

Read More - Credit Card Late Fee Shock

So, for Indians moving to the UAE, Canada, the UK or Australia, the damage may continue back home even after departure.

What Happens After The Move Abroad?

The first hit is credit history in India. The second is cost. Mint reported on 23 September 2024 that credit cards usually offer an interest-free period of 45-55 days, but interest starts on unpaid dues after that window. ET Wealth also noted on 23 February 2026 that paying only the minimum due can mean 3%-4% per month on the unpaid amount, making balances snowball fast. Some banks also reserve the right to adjust dues against balances held with them. HDFC Bank’s Most Important Terms & Conditions says the bank can exercise lien and set-off on monies held with it in case of default.

Previous Developments On This

India’s wider debt recovery picture shows lenders do not easily walk away from unpaid dues. A LoansJagat report dated 23 July 2025, citing a Finance Ministry reply in Parliament, said 1,629 wilful defaulters owed PSU banks ₹1.62 lakh crore as of 31 March 2025. The report also noted that overseas defaulters were excluded from that domestic count.

Separately, ET reported on 2 July 2025 that SBI denied a job candidate after a poor CIBIL record linked to earlier defaults, showing how credit history can spill into future opportunities in India. Cross-border relocation may complicate collection, but it does not erase the borrower’s record.

Statements By Stakeholders

Also Read - Repayment Strategy That Works Smart Debt Plan

CIBIL’s position is direct: missed and late payments can damage the borrower’s score. HDFC’s card terms say the bank may use lien and set-off rights on balances it holds. Mint and ET have both highlighted how unpaid dues attract steep interest and can keep rising if only minimum dues are paid.

Conclusion

For Indian credit card users, moving abroad changes the location, not the liability. The dues can grow, the credit report can suffer, and the fallout can return when the borrower needs money in India.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article