Startup Business Loans in India: First-Time Founders Get More Formal Funding Routes

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- What has happened? First-time entrepreneurs now have clearer loan routes through MUDRA, Stand-Up India, CGTMSE and CGSS, with ticket sizes running from ₹50,000 to ₹20 crore.

- \What was the previous update on this news? Recent policy changes raised the MUDRA cap to ₹20 lakh and expanded startup guarantee cover from ₹10 crore to ₹20 crore.

India’s startup loan architecture is widening for first-time founders, but access still depends on scheme fit, repayment capacity, and clean documents at the time of application.

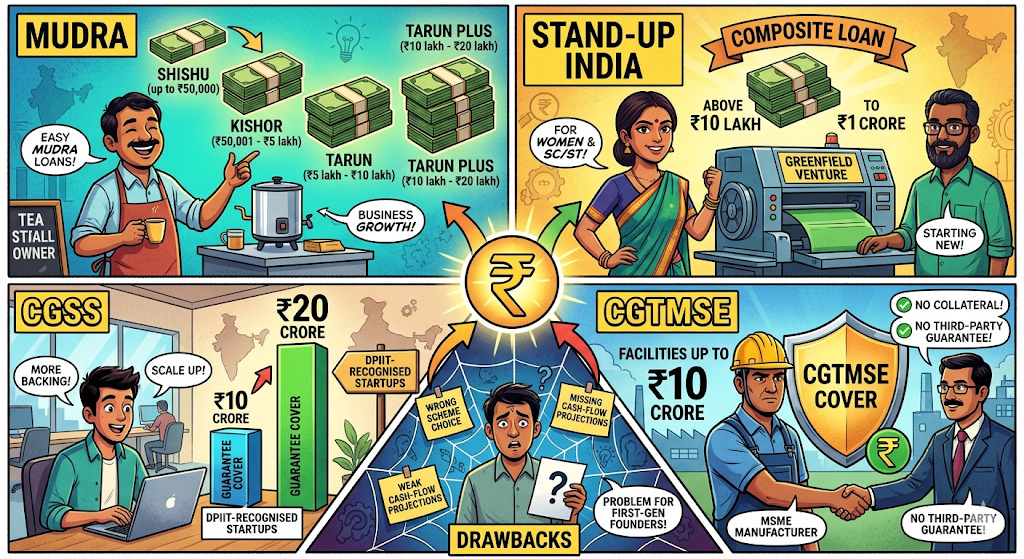

Why Startup Loan Access Is Expanding?

India’s first-time entrepreneurs now have more structured debt options than before. Small business founders can start with MUDRA, women and SC/ST borrowers can use Stand-Up India, MSMEs can seek collateral-light bank loans under CGTMSE, and DPIIT-recognised startups can tap CGSS-backed debt.

The drawback is straightforward. A wrong scheme choice, weak cash-flow projections, or missing registrations can still delay sanction or reduce eligibility. That becomes a problem for first-generation founders who do not have collateral or past borrowing history.

How This Could Change Borrowing For Small Businesses?

For small borrowers, this expands formal entry points. A micro entrepreneur can begin with MUDRA, while a larger first-time founder from an eligible category can move through Stand-Up India with repayment of up to 7 years and a moratorium of up to 18 months.

Collateral remains the biggest hurdle. CGTMSE helps here because banks can structure eligible loans on project viability without asking for full security. For many first-time founders, that improves loan conversations at branch level. Platforms such as LoansJagat are also positioning business loans for self-employed borrowers through digital comparison journeys.

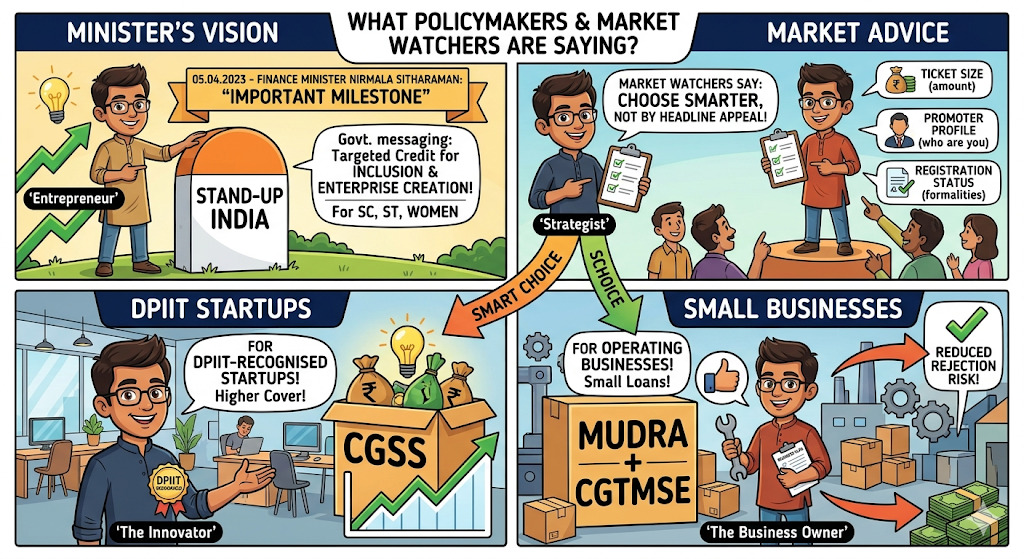

What Policymakers And Market Watchers Are Saying?

On 05.04.2023, Finance Minister Nirmala Sitharaman said Stand-Up India had become “an important milestone” in promoting entrepreneurship among SC, ST and women borrowers. The government’s own messaging is that targeted credit is now tied to inclusion and enterprise creation.

Market watchers are pushing a practical solution: founders should choose by ticket size, promoter profile and registration status, not by headline appeal. CGSS suits DPIIT-recognised startups. MUDRA and CGTMSE suit smaller operating businesses. That reduces rejection risk at the first screening stage.

Conclusion

India’s startup loan pipeline is getting broader, but approval still rests on numbers, paperwork and scheme fit. For first-time founders, better preparation will count as much as policy support.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article