UPI Delay Plan For New Payees Raises Fresh Worries Over Speed And User Friction

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- A proposal seeks a 1-hour delay on select digital transfers above ₹10,000, with banks and fintech players warning this could slow real-time payments.

- This follows tighter digital-payment safeguards this year, including mandatory 2-factor authentication from April 1, 2026.

A proposed 1-hour pause on some first-time high-value digital transfers has reopened a sharp debate between fraud control, user convenience, and the speed promise of India’s payments stack.

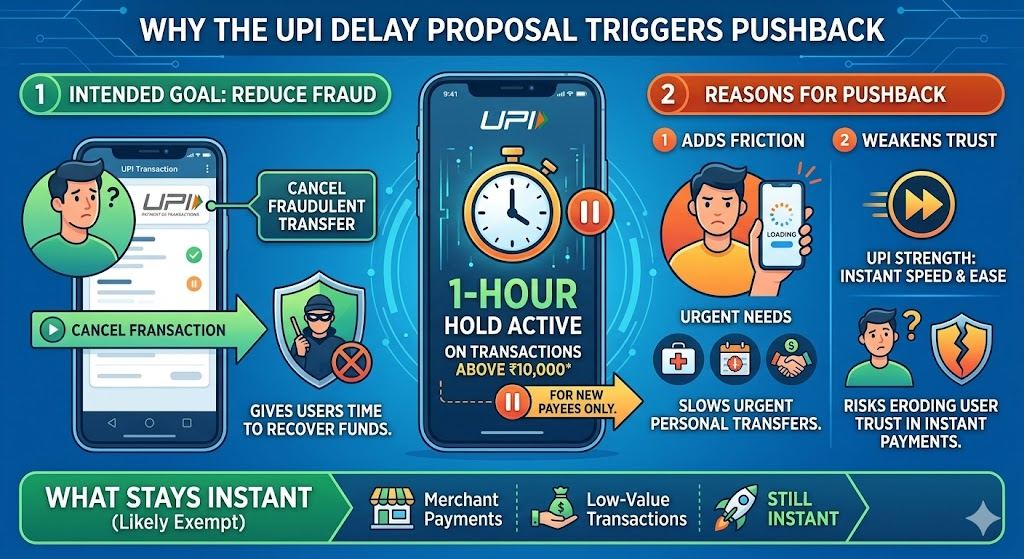

Why The Proposal Has Triggered Pushback?

India’s fast-payment ecosystem may be heading for a visible change if the proposed delay on some new-payee transfers moves ahead. The idea is to hold certain account-to-account payments above ₹10,000 for 1 hour, giving users time to cancel a fraudulent transfer. News reports say merchant payments and low-value transactions are likely to stay outside this hold.

In the short term, this could add friction for people who use UPI for urgent personal transfers. Over the longer run, supporters say the pause could reduce fraud losses, but bankers argue that any broad slowdown may weaken user trust in instant payments, especially when UPI has grown around speed and ease.

The proposal and the objections look like this:

The core concern is simple: a fraud-control tool may also change how ordinary users experience digital payments.

What It Could Mean For Users Across India

For the public, the biggest downside is delay in urgent first-time transfers above the threshold. A user sending rent support, medical money or family assistance to a new account may face a wait where they earlier expected instant credit. That could hit small households and informal payment behaviour more than card-based or merchant-led transactions.

There is another side. Reported digital payment frauds rose to 2.8 million between 2021 and 2025, with losses touching ₹230 billion, according to Reuters’ reporting on the proposal. So a cooling window may help users stop panic-driven transfers pushed by scam calls, fake apps or impersonation fraud.

Tthe earlier developments show why this proposal did not come out of nowhere:

The sequence is visible: tighter controls are building step by step, and this delay proposal is part of that broader anti-fraud shift.

What Stakeholders Are Saying And What Could Work Better

Bankers quoted in recent coverage say the proposal has merit, but they want the threshold reviewed and the operational burden examined. Some reports say industry players may prefer a more targeted model rather than a broad hold that affects normal transactions too.

A more workable fix may be a risk-based filter: stricter checks only for suspicious patterns, optional whitelisting for trusted payees, and faster alerts before money leaves the account. That would keep fraud control in focus without slowing the wider digital flow more than necessary.

Conclusion

The proposal has opened a real policy clash between safety and speed. The final call will likely depend on whether regulators choose a broad cooling period or a narrower, risk-based model.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article