Why Indian Women Still Can’t Manage Their Own Money

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

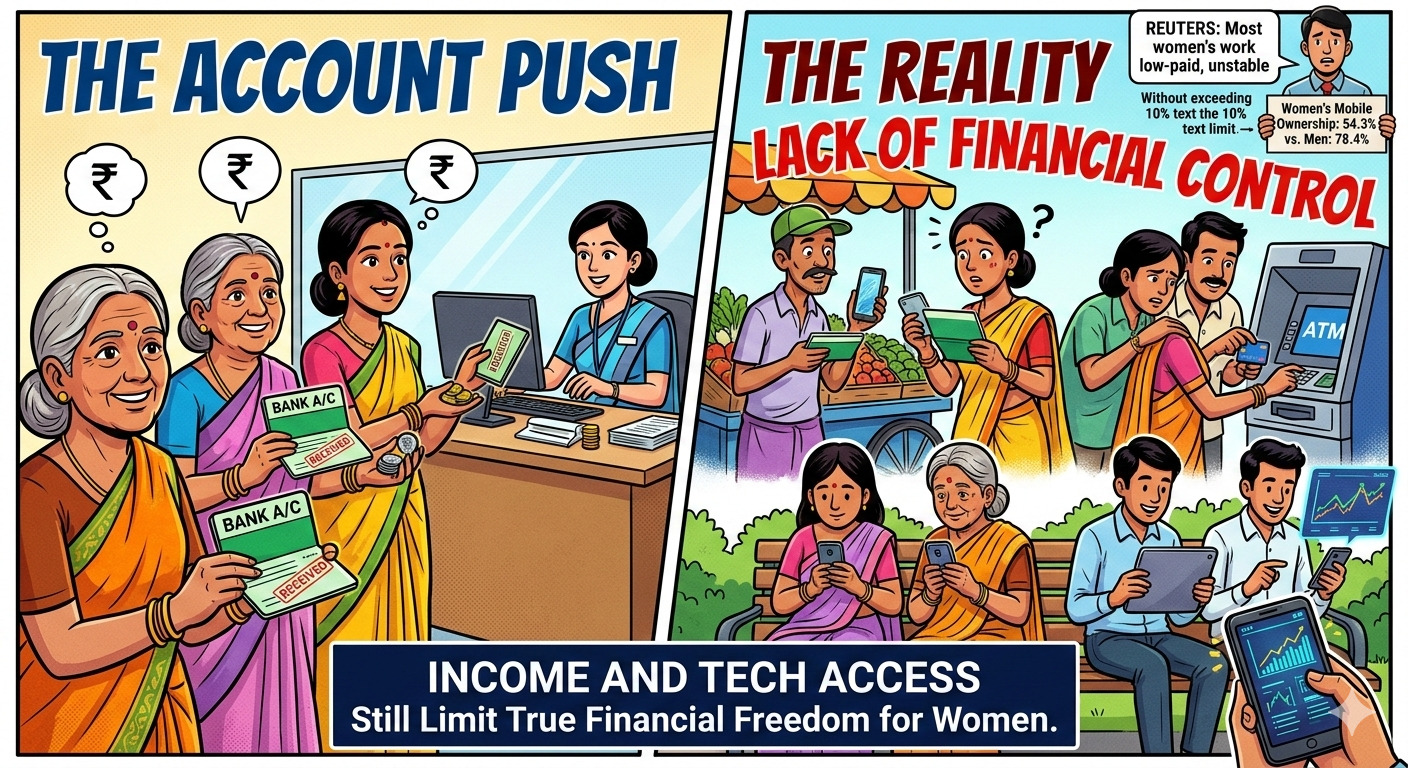

India has brought millions of women into banking, but control over savings, digital payments, credit and investing still slips away inside homes, workplaces and markets.

India’s headline financial inclusion story looks impressive, but the gap shifts sharply when usage is checked. The World Bank’s India Financial and Digital Inclusion, Fall 2025, released in 2025 with updated India indicators, shows 89.2% of women aged 15+ have an account, against 88.8% of men. Yet only 22.8% of women save formally, compared with 31.1% of men. That gap explains the core issue. Indian women are entering the system, but many still do not control how money is earned, saved, moved or invested in their own name.

India’s Bank Account Push Has Not Become Financial Control

The story gets tougher once money use moves beyond opening an account. The same World Bank note shows 94% of women in the labour force have an account, but women outside the labour force trail at 86%. This suggests income still drives financial control. The digital barrier is equally sharp. Women’s mobile phone ownership stands at 54.3% against 78.4% for men.

Smartphone ownership is 31.8% for women against 52.0% for men. Internet use in the last 30 days is 36.3% for women and 55.0% for men. Online learning or training stands at 11.9% for women against 19.0% for men. In plain terms, many women can receive money, but not always transact independently. Reuters, in a poll report published on 22 July 2025, also noted that much of the recent rise in women’s work is concentrated in low-paid, unstable or self-employment segments rather than secure salaried jobs.

This is why the problem is no longer just access. It is private control, regular use and confidence with formal tools.

Read More : Women Investors Rising In India, But Confidence Still The First Barrier

What Changed Earlier And Why The Gap Still Remains?

The progress is real. The NFHS-5 national report, released in 2021 for 2019-21, showed women who had a bank or savings account that they themselves use rose to 78.6%, up from 53.0% in NFHS-4 for 2015-16. The PLFS annual press note, released on 23 September 2024, showed female labour force participation rose to 41.7% in 2023-24 from 37.0% in 2022-23. On 28 August 2025, a PIB release on PM Jan Dhan Yojana said 56% of Jan Dhan accounts are held by women and 67% are in rural or semi-urban areas.

But the next layer looks weak. An Economic Times report, published on 6 March 2026, said women hold only 25% of mutual fund folios and start investing 5 years later than men. A Mint report, published on 8 March 2026, said the share of equity mutual funds in women’s portfolios rose from 10% to 32% in 5 years.

That signals movement, but from a low base. In entrepreneurship, the funding gap is harsher. An Economic Times report, published on 5 March 2026, said women-led startups receive just Rs 4 out of every Rs 100 raised by founders. A Times of India report, published on 6 March 2026, put the share at 4.4% of capital raised for companies with at least 1 woman co-founder.

This is the unfinished journey. Women are inside the banking network, but not fully inside wealth creation.

Also Read : Only Women Are Eligible For This SBI Loan

What Stakeholders Are Saying?

On 28 August 2025, Finance Minister Nirmala Sitharaman, in the PIB PMJDY release, said financial inclusion drives economic growth. On 27 November 2025, SEBI issued a circular to incentivise onboarding of women investors. LoansJagat, in a report published on 9 February 2026, said confidence remains the first barrier for women investors.

Conclusion

Indian women now have more accounts, but not enough command over savings, credit and investment. The next test is not access. It is whether women can use money without depending on anyone else.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article