By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Miss a loan for long enough, and recovery does not stay limited to the borrower. A new J&K ruling shows even a guarantor’s pension account can come under pressure.

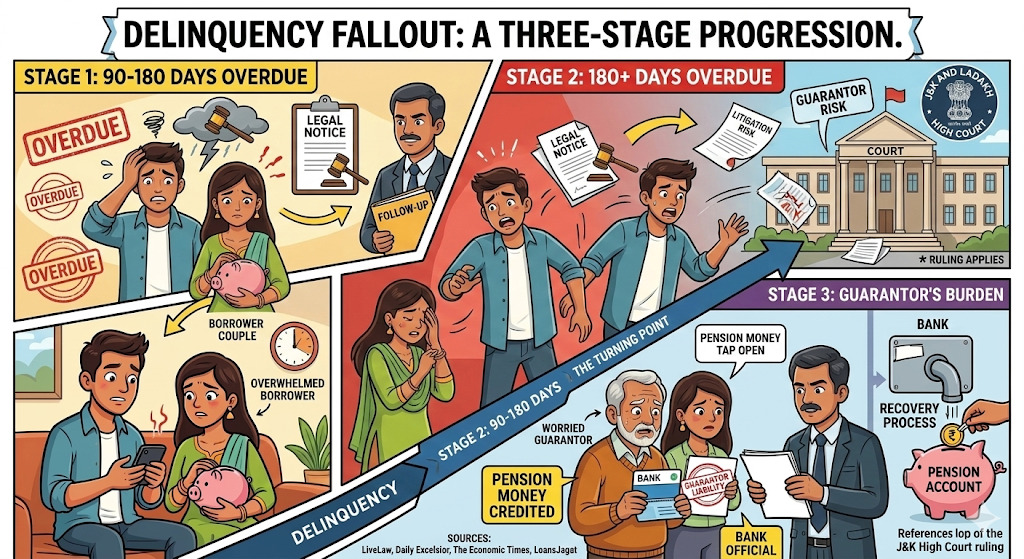

A missed EMI usually begins with penalty charges, follow-up calls and credit damage. But when the delay stretches, the fallout can move from inconvenience to legal recovery. That is the real warning from the latest Jammu and Kashmir and Ladakh High Court ruling, reported by LiveLaw, Daily Excelsior and The Economic Times.

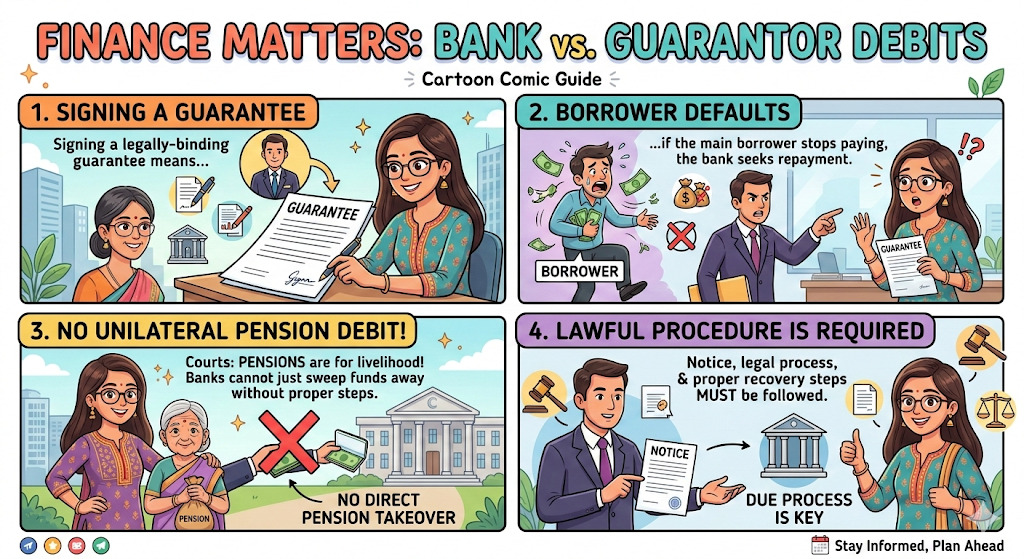

The court said that once pension money is credited into a bank account, it is treated as received and can be tapped to recover dues linked to a guarantor’s contractual liability. If a borrower does not clear a loan on time, the guarantor can also feel the blow.

Before the legal position tightened in this ruling, lenders had already been following a familiar recovery path. A LoansJagat explainer dated 17 June 2025 said that after 90 to 180 days of non-payment, lenders may issue legal notices or begin recovery proceedings, and after 180+ days, stronger action can follow.

Read More : Loan EMI Repayment Problems in India

That is why this is not just a pension headline. It is a clear example of what can happen when loan repayment keeps slipping and a guarantor has signed on the dotted line.

Missed a few EMIs already? Compare personal loans on LoansJagat to find a more manageable repayment option before the default deepens.

The fresh ruling has put one point in sharp focus. Standing as guarantor is not a formality. It is a binding promise. According to the reports published on 26 and 27 February 2026, the borrower had taken a cash credit facility of ₹15 lakh, and the pensioner had stood as guarantor on 9 March 2018.

Daily Excelsior reported that the pensioner was receiving around ₹36,000 a month and that ₹50,000 was deducted from his pension account on 25 August 2025 after the borrower failed to clear the dues.

The court accepted the bank’s position that pension protection under the Pensions Act applies till disbursal, and not indefinitely after the amount reaches the bank account. That became the turning point. The ruling effectively says that once default deepens, recovery may move beyond the original borrower if there is a valid guarantee backing the loan.

The Economic Times report published on 9 March 2026 highlighted the same reason while explaining why the bank was allowed to proceed against the credited pension amount.

This gives a harder edge to the usual advice around delayed repayments. A loan default can widen into a guarantor dispute, especially when the bank argues that contractual recovery rights have already kicked in.

The latest ruling does not end the legal debate. In an earlier J&K case reported by Daily Excelsior on 3 August 2025, the High Court had restrained the bank from dipping into a pension account for recovery.

Indian Kanoon’s record of that dispute shows the challenge was built around unilateral freezing and deduction from the pension account despite the account holder’s claim that pension money remained protected.

Then came the Orissa High Court ruling that pulled the debate in the opposite direction. SCC Times, on 27 October 2025, and LiveLaw, on 23 October 2025, reported that the court held that a bank cannot unilaterally deduct money from a retired employee’s pension account. The facts were striking.

The pensioner was drawing about ₹35,000 a month. His wife had taken loans of ₹5.90 lakh on 12 June 2015, ₹8 lakh on 7 December 2015 and a car loan of ₹7.45 lakh on 31 October 2017. The transport loans were classified as NPAs on 7 November 2018.

Later, ₹2.30 lakh and ₹2.70 lakh were debited on 17 and 19 February 2024, taking the total disputed recovery to ₹5 lakh. The court ordered the amount to be returned within 4 weeks.

Also Read : What to Do When Monthly Payments Become Unmanageable

That means courts have not spoken in one voice. One line has allowed recovery after pension credit. Another has pushed back against unilateral debit and lack of due process.

The bank’s position in these disputes has been simple. If a guarantor signs a legally enforceable guarantee and the borrower defaults, recovery can move against the guarantor too. Courts opposing unilateral debit have said pension is tied to livelihood and cannot be swept away without lawful procedure, notice and proper recovery steps.

A delayed loan does not stay a delayed loan forever. If the default deepens, the borrower’s guarantor can be dragged in too, and this latest J&K ruling shows how costly that can become.

Related Financial News | |||