By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

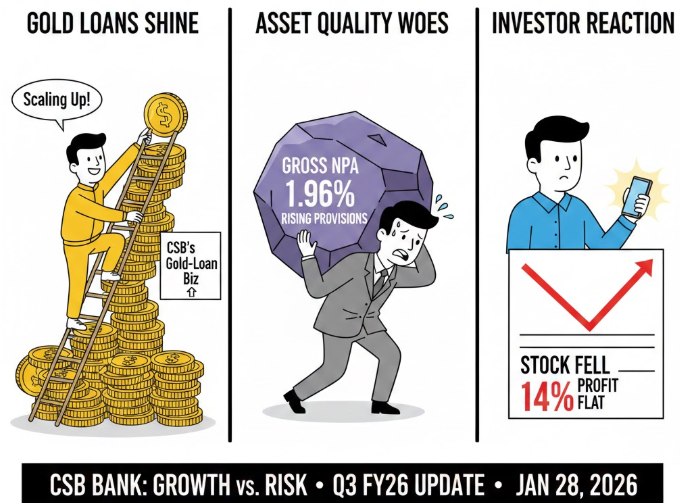

CSB Bank is under the trader’s lens after a weak Q3 FY26 reaction. Gold loans are growing fast, but NPAs and provisions raised concerns.

CSB Bank’s stock has turned volatile after its Q3 FY26 update, with investors weighing a strong core income trend against rising stress indicators. On January 28, 2026, an Economic Times report said the stock fell 14% as profit stayed almost flat and asset quality worsened.

The same day, MarketsMojo flagged that the gross NPA ratio rose to 1.96% and provisions jumped. In parallel, CSB’s gold-loan franchise continued to scale, positioning it as a near-term earnings cushion if credit costs were cool.

The trigger is the Q3 FY26 outcome and what it signals for the next few quarters. MarketsMojo’s January 28, 2026 (03:16 PM IST) result analysis reported net profit at ₹152.67 crore (up 0.69% YoY) and net interest income at ₹453.19 crore (up 20.71% YoY), but noted margin pressure and deterioration in overall asset quality with gross NPAs at 1.96%.

This combination has kept the stock in a “wait and watch” zone, especially for near-term tactical traders.

An Economic Times report dated January 28, 2026 also highlighted the sharp reaction, saying the decline came as investors focused on flat profit and worsening asset quality.

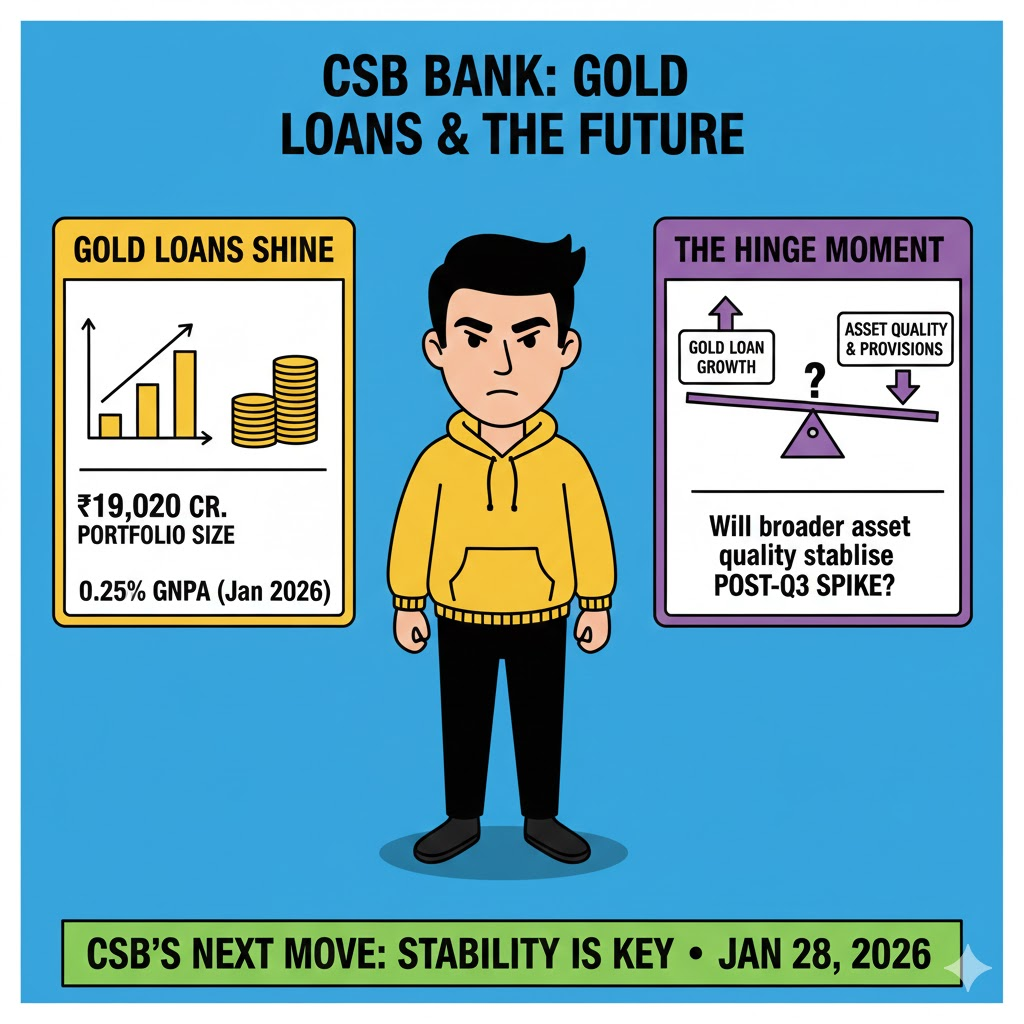

The strongest support for the “gold loans can steady the ship” view comes from CSB Bank’s own disclosure. In its Investor Presentation Q3 FY26, dated January 28, 2026, CSB reported that its gold-loan portfolio rose to ₹19,020 crore in Q3 FY26 from ₹13,018 crore in Q3 FY25. It also disclosed key operating metrics for the gold book: portfolio yield 11.83%, LTV 63%, and gold-loan GNPA 0.25%.

Below is a quick data snapshot from the official presentation, useful for readers who want the exact operating picture first.

This scaling is the key tactical hook. Gold loans are secured, disbursal cycles are short, and pricing generally supports NII. Yet the market wants proof that stress in other segments does not keep pushing provisions higher.

The stock had run up earlier in January, before the Q3 reaction pulled it down sharply. MarketsMojo’s stock coverage noted CSB hit a 52-week high of ₹519.95 on January 5, 2026, signalling strong sentiment before results.

The reversal was driven by the risk-cost narrative. MarketsMojo’s Q3 analysis reported provisions at ₹86.77 crore in Q3 FY26 versus ₹16.53 crore YoY, keeping focus on credit costs rather than just growth.

Macro commentary on gold loans also adds context to why CSB’s gold push is getting attention. LoansJagat’s report dated January 30, 2026 said nationalised banks hold 60% of India’s gold loans outstanding and noted higher gold prices have enabled larger ticket loans, supporting portfolio expansion.

A Deccan Chronicle report dated January 28, 2026 added another sector datapoint: as of November 2025, gold loans were about 14% of total consumption loans and 9.7% of total retail loans in portfolio outstanding terms

Management commentary relayed by The Economic Times on January 28, 2026 indicated business momentum remained strong, with improvements expected in the current quarter, even as the market reacted to NPAs and provisions.

Traders are tracking whether gold-loan growth stays firm. Analysts continue to watch margins and credit costs closely.

For readers tracking the current tape, Economic Times’ company page showed CSB Bank at ₹384.85 on February 20, 2026.

Traders also use pivot zones as a quick weekly reference. Choice’s technical page lists supports near ₹393, ₹388, ₹381 and resistances near ₹405, ₹412, ₹416.

If CSB holds above ₹381 to ₹388, the bounce thesis stays open for a tactical trade. A clear break below ₹381 can shift sentiment back to risk-off quickly, especially with NPAs already elevated.

Gold loans are clearly scaling at CSB, with ₹19,020 crore portfolio size and 0.25% GNPA disclosed on January 28, 2026.

The stock’s next move hinges on whether broader asset quality and provisions stabilise after Q3’s spike.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors |