By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

India’s financial shocks spread fast because lenders, NBFCs and markets are tightly linked. New research shows contagion through linkages often dominates standalone bank weakness.

India’s financial system has grown deeper, but also more intertwined. That has shifted the risk profile. A new India-focused analysis published on 20 February 2026 argues that systemic risk is driven less by a few weak institutions and more by the “wiring” connecting banks,

NBFCs and markets, which transmit liquidity and valuation shocks. Global and domestic stress events show that once funding tightens, correlations rise, spillovers intensify, and containment becomes harder.

The key issue is systemic risk created by interconnected balance sheets. In India, banks and NBFCs share funding lines, common borrowers and market channels. When one part faces a liquidity hit, the stress can migrate quickly across the network.

A 2025 study on India’s financial network finds crisis-period interconnectedness rises, with banks often acting as shock emitters and NBFCs as receivers. This raises the cost of treating risks as isolated.

The latest research on India’s “financial wiring” tracks connectedness since the mid-2000s and finds it stays structurally high. In normal phases, total connectedness “rarely” drops below about 75% of its peak. In stress phases, it often climbs above 90% of its peak. That signals a system where balance sheets start moving together, so problems spread.

The same work uses a measure called NetVIX and reports its highest recorded level during COVID-19. More importantly, the decomposition shows systemic risk is dominated by the contagion component, while the conventional volatility component stays close to 0 even in major stress windows.

This helps explain why headline comfort on individual institutions can coexist with fragile system behaviour. The IMF’s India stability assessment also flags that nonbank and market financing have grown, making the system more diverse and interconnected.

The time profile of shocks is also sharp, which affects how quickly policy and treasury teams must respond.

Once a funding shock hits, the window for “wait and watch” is short, and spillovers can outlast the first headline.

Past episodes underline the same pattern. During the IL&FS phase, the research notes that stress channels can flip, with some NBFCs temporarily turning into net spreaders of risk instead of receivers. That is why “who transmits risk” can change based on liquidity conditions.

Policy signals can reshape the network too. The study highlights that after the October 2017 announcement of a ₹2.11 lakh crore recapitalisation programme for public sector banks, connectedness saw one of its sharpest jumps outside the pandemic.

Meanwhile, retail stress can surface through everyday repayment behaviour. On 9 December 2025, LoansJagat reported renewed pressure in recoveries, especially in retail and unsecured borrowers, even as asset-quality optics looked improved.

A Times of India report also flagged rising smartphone EMI delinquencies after enforcement practices changed, pointing to underlying borrower strain in parts of consumer credit.

Paragraph before table: international regulators have been signalling similar risks, especially around nonbanks and leverage.

Paragraph after table: for India, the implication is not to treat NBFC stress as “separate”. The linkages are the channel.

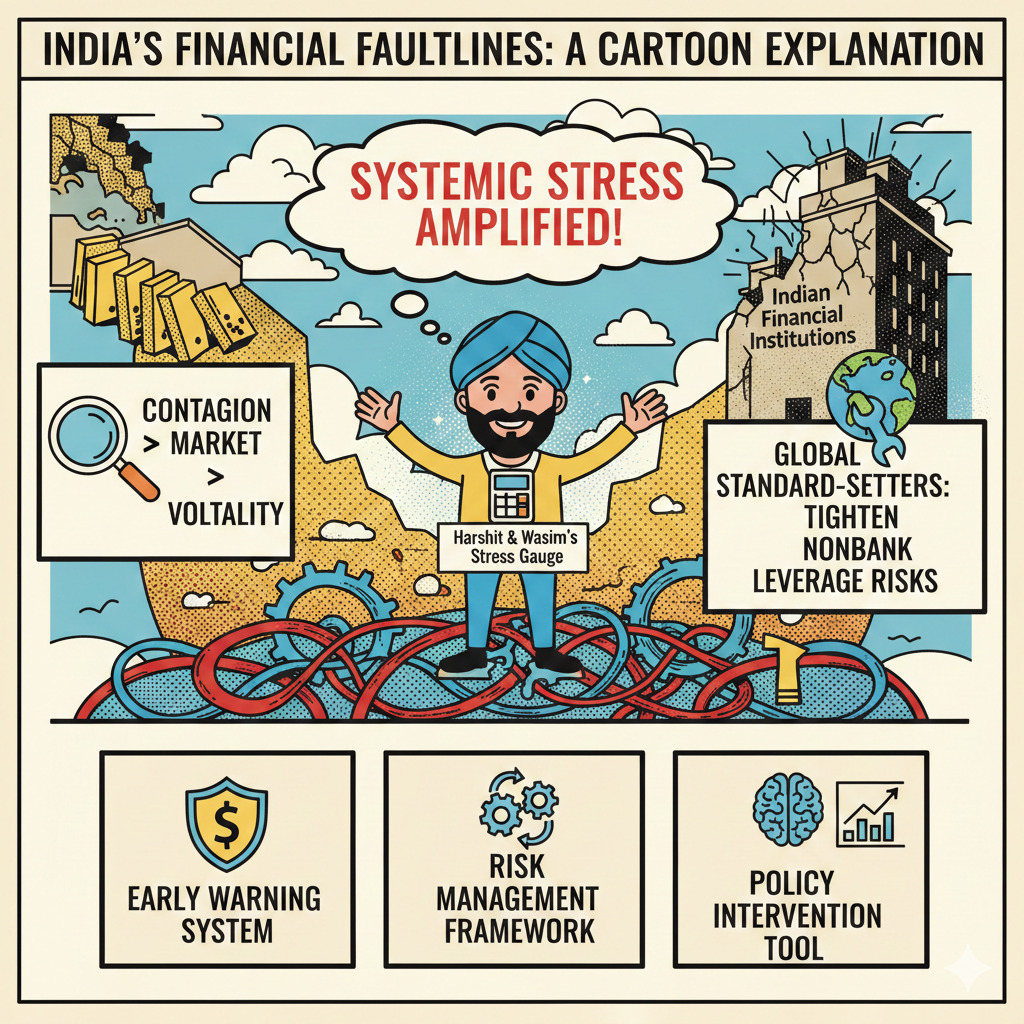

Researchers Harshit Kumar Sharma and Wasim Ahmad argue that the wiring of institutions amplifies systemic stress, with contagion outweighing pure market volatility in India’s network. Global standard-setters have urged governments to tighten frameworks for detecting and managing nonbank leverage risks.

India’s risk hotspots can shift quickly from banks to NBFCs to retail credit, mainly through shared funding and correlated behaviour. Stronger monitoring of linkages, not only standalone balance sheets, is where the next risk edge sits.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors |