By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Public sector banks are lining up a pitch to the regulator to soften climate-finance rules, as green deposits stay niche and compliance costs keep rising.

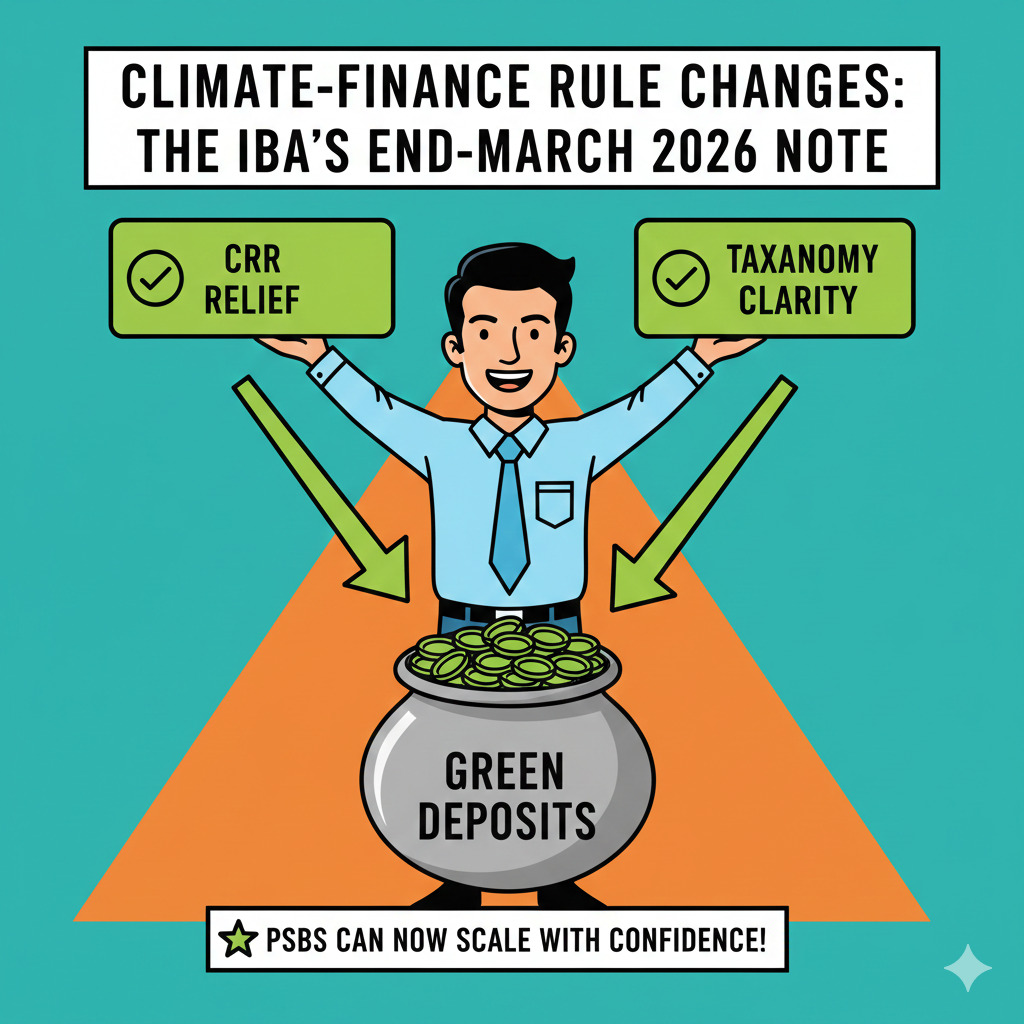

India’s public sector banks (PSBs) may soon approach the Reserve Bank of India through the Indian Banks’ Association (IBA) to seek targeted changes in climate finance guidelines, after early green-deposit traction stayed muted.

The key demand is incentive-linked: a carve-out on reserve requirements to make green deposits cheaper for banks to mobilise and deploy.

Another ask is definitional clarity, since lenders say the “green” label still leaves room for interpretation and later disputes. The IBA’s note is expected by end-March 2026, according to reports.

Banks are saying the current rulebook does not reward them for raising green deposits. They still have to park part of deposits as cash reserves, which reduces deployable funds and pushes up cost. Reports peg the cash reserve ratio at 3%, and lenders want relief specifically for green deposits.

They are also uneasy about the “what qualifies as green” layer. In internal credit committees, this slows approvals, and raises reputational risk if an activity later gets tagged as greenwashing.

The IBA is expected to move a formal representation by end-March 2026, seeking two practical changes. First, lenders want CRR easing for green deposits so that a larger share of these liabilities becomes usable for lending and investment.

Second, they want sharper taxonomy guidance so bankers and auditors are aligned on eligibility from day 1.

Below is what banks are trying to change, and why it is central to product uptake.

This push also ties into the bigger funding gap. India needs around $2.5 trillion (at 2014-15 prices) to meet its NDC targets till 2030, as stated in the government’s climate finance taxonomy document hosted on PIB.

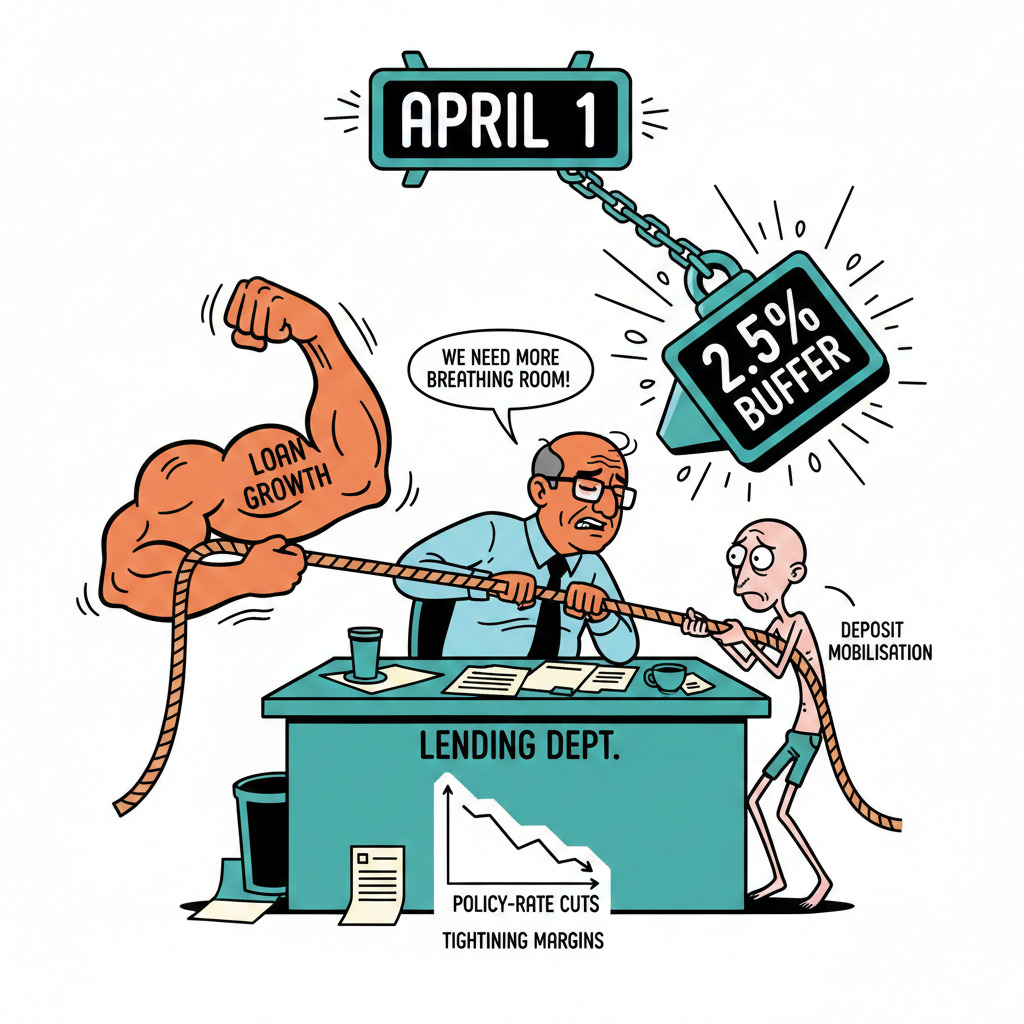

The climate-finance debate is landing at a time when lenders are already strained on liquidity and compliance bandwidth. Reuters reported that banks have asked for regulatory leeway as loan growth outpaces deposit mobilisation. It also noted the policy-rate cycle, with the RBI having cut repo rates by 125 bps since February 2025, tightening margins for lenders hunting stable deposits.

The same Reuters report said revised liquidity coverage ratio norms kicking in from April 1 require a 2.5% buffer on digitally linked deposits, which treasury officials have suggested delaying. Bloomberg also reported lenders seeking relaxation of liquidity rules to unlock more funds.

Here is the recent sequence that is shaping bank strategy.

Separately, the Reuters Jan 29 report underlined India’s climate exposure, citing Germanwatch data: 430 extreme weather events during 1995-2024, over 80,000 deaths and about $170 bn in losses.

Banks see this as the macro risk case for climate finance, but want workable economics and clearer definitions to scale it.

Banking officials quoted in The Economic Times and DebtCircle point to two pain points: no meaningful incentive for green deposits, and taxonomy ambiguity that can backfire later.

On the disclosure side, Reuters sources cited cost burdens and misalignment with corporate disclosures as reasons for the pause, which lenders read as space to recalibrate.

The IBA’s end-March 2026 note is now the key trigger point for climate-finance rule changes. If CRR relief and taxonomy clarity come through, PSBs could finally scale green deposits with confidence.

Related Financial News | |||

Reduces interpretation risk and speeds up approvals, also limits greenwashing disputes.

How RBI’s Repo Rate Decision Affects Borrowers and Depositors |