By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

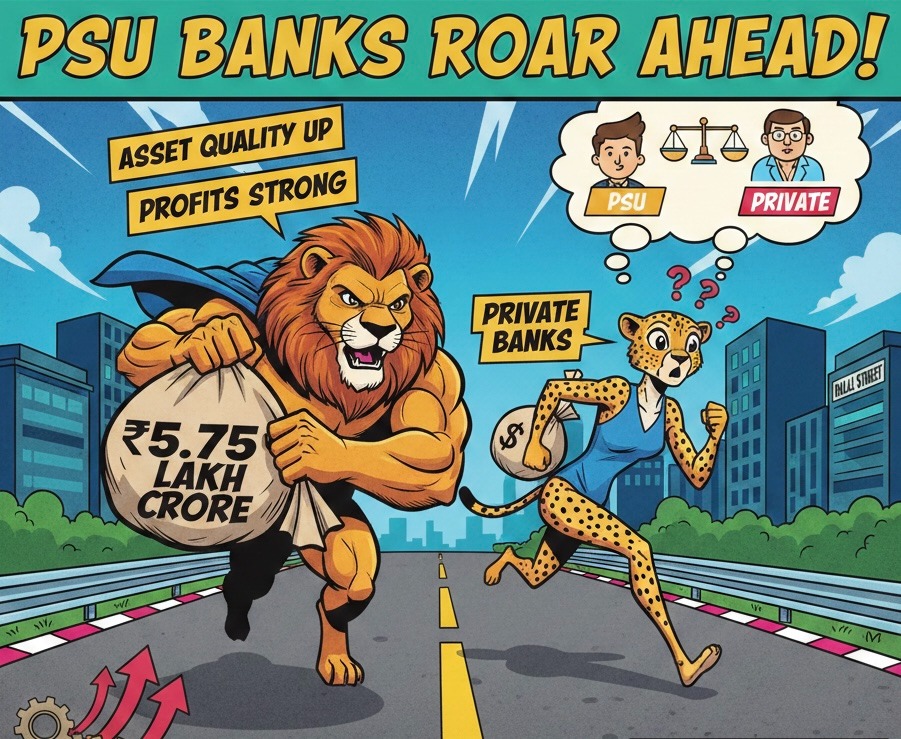

PSU bank stocks have surged as asset quality improves and profits stay strong. In 6 months, their combined market cap rose ₹5.75 lakh crore.

PSU banks are back in the spotlight after adding ₹5.75 lakh crore in market capitalisation in the last 6 months, taking the combined value of 12 PSU banks to around ₹21.35 lakh crore. This sharp jump has revived the “PSU vs private” debate on Dalal Street, with investors tracking whether public lenders can keep outperforming private peers.

The rally is being linked to cleaner balance sheets, steady loan growth and strong earnings delivery. At the same time, traders are watching funding costs, deposit trends and any early signs of a credit-cost uptick.

The headline move is simple: PSU banks have outpaced private lenders in recent months. An Economic Times Markets report published on Feb 20, 2026 (09:04 AM IST) said the 12 PSU banks added about ₹5.75 lakh crore in market cap in 6 months, reaching roughly ₹21.35 lakh crore.

A related Hindi report by Navbharat Times (published Feb 20, 2026, 01:14 PM IST) echoed the scale of the move and highlighted how investors are questioning how long the “party” can last.

Before getting into fundamentals, the market performance gap is what pulled attention first.

These numbers, quoted across market reports, are driving the “PSU banks are taking share” storyline. The Motilal Oswal page that circulated similar comparisons is linked here as a market reference (page accessed on Feb 21, 2026).

The strongest support has come from hard fundamentals, especially asset quality. A PIB release dated Feb 09, 2026 cited data showing the gross NPA ratio of Scheduled Commercial Banks at 2.15% as on Sep 30, 2025 (provisional). The same release said PSBs were at 2.50%, private sector banks at 1.73%, and foreign banks at 0.80%.

Profitability has also stayed firm. A PIB release dated Nov 12, 2025 said PSBs posted ₹93,675 crore net profit in H1 FY2025-26, with aggregate business at ₹261 lakh crore (as of Sep 2025). It also reported advances up 12.3% YoY, deposits up 9.6% YoY, and PSB GNPA at 2.30% and NNPA at 0.45%.

A LoansJagat report published Feb 04, 2026 said banking-sector discussions around liquidity support measures and restructuring of select NBFC exposures could further ease funding pressures for lenders, indirectly supporting credit growth outlook.

On the market tape, Reuters reported PSU banks were among the key drivers for weekly gains and said PSU banks rose 5.5% for the week ending Feb 20, 2026, while private banks gained 0.8% in the same week.

The re-rating has been building over time, not overnight. One visible trigger was the market gaining comfort that low slippages and credit costs are not a one-quarter story. Reuters, in a report dated Feb 18, 2026, noted that financials helped benchmarks end higher, with the Nifty 50 at 25,819.35 (+0.37%) and the Sensex at 83,734.25 (+0.34%) that day.

Another angle has been valuations. In an Economic Times interaction published on Feb 18, 2026, market expert Sudip Bandyopadhyay argued PSU banks could still offer value as the gap versus private peers narrows further, even if PSU multiples do not fully match top private lenders.

The policy and operating backdrop is best captured in the official performance snapshot.

These figures explain why investors have been willing to pay up for PSU earnings quality again.

Reuters market coverage on Feb 20, 2026 described PSU banks as the top sectoral gainers for the week, reflecting trader interest and risk-on positioning.

Sudip Bandyopadhyay’s view, published Feb 18, 2026, was that the valuation gap still leaves room for further narrowing.

The Finance Ministry note dated Nov 12, 2025 highlighted improved profitability and lower GNPA/NNPA for PSBs, backing the fundamental narrative.

PSU banks have support from cleaner books, strong profits and improving system asset quality. The next phase hinges on deposits, margins and whether credit costs stay contained.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors |