By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

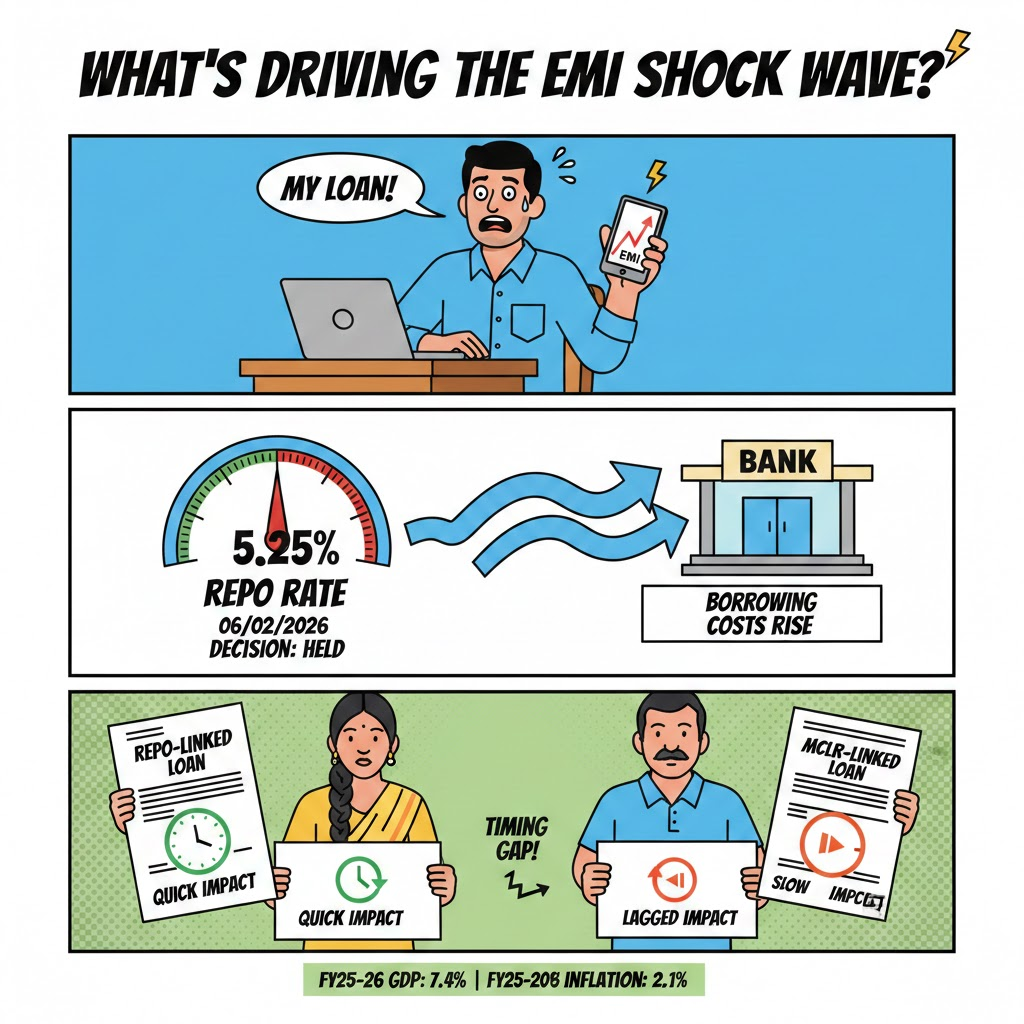

Repo rate moves are travelling faster to home loan EMIs. Borrowers on repo-linked loans see quicker resets, while MCLR-linked borrowers feel the impact later.

A repo rate change decides the direction of borrowing costs across the system. When policy rates rise, banks usually reprice floating-rate home loans, either quickly for repo-linked loans or with a lag for MCLR-linked loans. That gap is why 2 borrowers with similar loan amounts can see different timing on EMI impact.

In the current cycle, the focus has returned because the repo rate was held at 5.25% in the 06/02/2026 decision, keeping borrowers alert about what happens next. Coverage of the decision also pegged FY25-26 GDP growth at 7.4% and FY25-26 inflation at 2.1%.

Home loan transmission is no longer uniform. Repo-linked and external benchmark loans are built to reset more frequently, so changes in policy rates can show up sooner in borrowers’ interest rates and EMIs.

MCLR-linked loans typically wait for the borrower’s reset date, which can delay the impact even when policy rates move sharply.

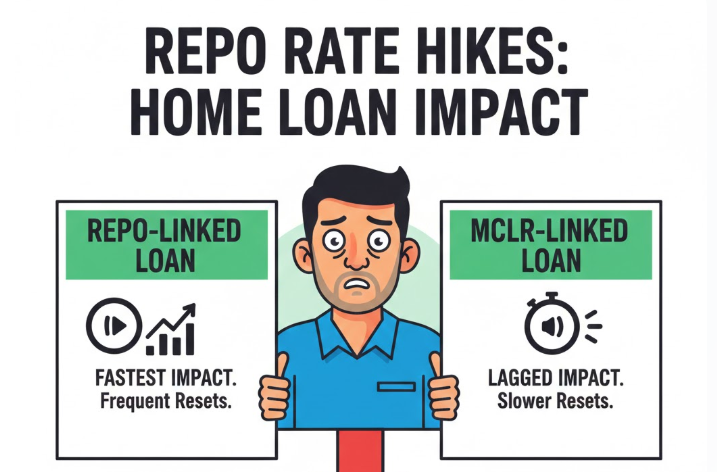

Before getting into the latest policy signals, here is the difference borrowers keep missing.

This split explains the “immediate pinch” borrowers talk about. It is less about the headline decision and more about the benchmark and reset rules.

For borrowers tracking the latest stance, LoansJagat explainer on the 06/02/2026 policy decision flagged that the repo rate stayed at 5.25%, which typically means no automatic EMI reset unless a lender changes the spread or the borrower hits a reset date.

The current “quick transmission” backdrop also sits on a sharp easing phase in 2025. On 05/12/2025, the repo rate was cut by 25 bps to 5.25%, taking total cuts in 2025 to 125 bps, as reported by Reuters.

That same day, Reuters also reported liquidity measures aimed at supporting transmission, including open market bond purchases worth ₹1 trillion and a $5 billion dollar-rupee FX swap, together framed as a liquidity boost of up to $16 billion.

Then came the February 2026 hold. Policy-day coverage in Times of India stated the repo rate remained 5.25%, with the Standing Deposit Facility (SDF) at 5.00% and the Marginal Standing Facility (MSF) and bank rate at 5.50%.

This is where borrowers look for direction, because the corridor levels often shape banks’ short-term funding pricing and the tone for retail lending.

Here is a clean snapshot borrowers can track after the latest hold.

For longer context, Reuters also published a historical tracker of repo rate changes since June 2000, which borrowers use to compare how fast rate cycles can turn.

Minutes released on 20/02/2026 showed a majority view that the current policy rate was appropriate, with the central bank watching incoming GDP and inflation data.

The same minutes quoted Governor Sanjay Malhotra backing the status quo given growth and inflation readings, and Deputy Governor Poonam Gupta signalling limited room for further cuts after cumulative easing.

Business Standard, Deccan Herald separately reported Malhotra’s view that the current rate looked appropriate in the backdrop of growth and inflation.

Repo rate hikes hurt fastest when the home loan is repo-linked and resets frequently. Borrowers should check the benchmark type and reset date before expecting relief or bracing for higher EMIs.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors |